Source: Shenyuan Hongyuan Macro

Authors: Zhao Wei, Chen Dafei, etc.

Summary

The 2024 US election is about to come to a conclusion, how to determine the market impact and possible outcomes of the 'Trump Trading' for reference.

(1) How has historical 'election trading' played out? Trading elections in the fourth quarter 'unexpectedly', followed by trading policy advancement

(1) How has historical 'election trading' played out? Trading elections in the fourth quarter 'unexpectedly', followed by trading policy advancement

Historically, 'election trading' usually goes through three stages: the first stage, when one side's advantage in winning rapidly expands/narrows, 'election trading' will start early. The US presidential election is divided into party primaries and the general election. Primaries usually end around the end of August, when the candidates of both parties and their policies gradually become clear, the market also gradually starts trading 'policy differences'.

The second stage, after the election results, the market prices in the 'unexpected' election. Elections since 1936 can be divided into four scenarios: 1) a reversal of the outcome, the market performance significantly reverses from the previous three months, such as 2016; 2) winning in high suspense, the market continues the previous trading direction for about a month, as in 2004; 3) winning in low suspense, the market continues for about 10 trading days after the election, like in 2020; 4) winning without suspense, the market reaction after the election is weak, as in 1996.

The third stage, the implementation/failure of core policies, will also bring about a restart/reversal of previous trading. Taking Trump's first term as an example, in March 2017, Trump's first policy, the new healthcare bill, failed, leading to a 'reversal' in Trump Trading. It was not until early November 2017, with the successful advancement of the tax reform bill, that market confidence in Trump's policies was restored, and the Trump Trading resumed thereafter.

(2) How does the market conduct 'Trump trading’? The US dollar is relatively strong, with bullish tendencies in US stocks and copper, while US bonds and gold lean bearish.

Starting from the perspective of market trading itself, 'Trump trading' can be observed from three angles. 1) Focus on the performance of major asset classes during the two debate periods. Trump had a clear advantage in the June 27 debate, but failed in the September 10 debate. 2) The correlation between Trump's election advantage in the past 90 trading days and the performance of various assets. 3) The performance of major asset classes during the Trump trading period between November and December 2016.

Taking everything into consideration, the 'Trump trade' leads to rising US bond yields, a stronger US dollar, and a higher certainty of bitcoin increasing, which trades more on the upside against US stocks and copper prices, while leaning bearish on gold, with uncertain impacts on oil prices. Based on the trading results from the previous market, the 'Trump trade' is not 'bearish for copper and oil, bullish for gold', indicating a certain divergence from the judgment based on policies.

Beyond consensus: 1) Regarding copper, Trump does not completely restrict the new energy sector. Stimuli to the economy such as tax cuts and re-industrialization will also boost the demand for copper. 2) Concerning gold, Trump's policies pushing up US bond rates bearish for gold prices, while his geopolitical policies may ease geopolitical risks. 3) As for oil, stimuli to demand such as re-industrialization may to some extent weaken the potential bearish impact on supply.

(3) 'Trump trading' in the equity market? Large cap growth is relatively bullish, with a focus on finance, energy, and manufacturing.

For the US stock market, structurally 'Trump trading' may favor large cap growth. Since early June to mid-July and from mid-September onwards, Trump's election probability has significantly increased during these two stages, favoring large cap stocks and growth. Logically, Trump's favorable policies like tax cuts and technology benefit growth sectors, while his policies exacerbate the upward risk of US bond yields, potentially putting pressure on small cap stocks.

Considering excess returns on debate days, excess returns at various stages of the election, and the correlation between the past 90 trading days and Trump's winning rate, the potential impact of 'Trump trading' on industries can be assessed: 1) Relaxation of financial regulations, bullish for banks; 2) Development in traditional energy sectors, bullish for energy equipment; 3) Corporate tax reductions, bullish for electronic devices; 4) Weak support for clean energy, bearish for electrical utilities.

Apart from the aforementioned industries, the following consensus-unrelated categories are worth monitoring: 1) Trump's policies such as re-industrialization support air transportation logistics, building materials, autos, and other industries; 2) Relative to Harris' tax cuts and subsidies for the middle and lower income groups, Trump's tax reduction policies benefit the wealthy, leading to bearish sentiment for essential consumption, healthcare, and the likes; 3) Trump's geopolitically contraction policy, bearish for military industry.

(4) Possible deduction of 'election trading'? Short-term looks at unexpected results, medium-term looks at policy impulses, long-term looks at fundamentals.

Currently, the trading balance has shifted towards Trump; if Trump is elected, the continuity of trading may be limited. If Harris wins, trading may significantly reverse. The continuation of mail-in voting, post-epidemic urban-rural population migration, etc., still bring certain variables to the election. If Trump is elected, the market may resemble 2020, with trading continuing slightly; but once Harris wins, the market may resemble 2016, with trading significantly reversing.

Looking at the medium term, whether policy propositions are smoothly implemented may directly affect the reversal or continuation of the third phase of election trading. 1) Timely delivery, in the first term, Trump swiftly issued policies in immigration, trade, regulation, etc., through executive orders, but tax policies were implemented slowly. 2) Possible implementation, Trump's policy implementation rate in the first term is only 23%, but it is higher in the trade field.

In the long term, the impact of elections on the market may mainly be achieved through influencing the fundamentals. This year's election results can be divided into four scenarios: ① Republican Party comprehensive victory (49%), ② Trump + divided Congress (14%), ③ Democratic Party comprehensive victory (12%), ④ Harris + divided Congress (21%). In terms of the positive impact on the economy: ③>①>④>②.

Risk warning

Risk warnings: escalation of geopolitical conflicts; US economic slowdown beyond expectations; Japanese yen continuing to appreciate beyond expectations.

Report Text

The dust of the 2024 US election is about to settle, but there is still controversy over the impact of the 'Trump trade' on certain assets. The rightful place of the 'Trump trade' in asset price performance, potential market deductions after the election? For reference.

First, how is "election trading" interpreted in history? Unexpected election trading in the fourth quarter, followed by the advancement of trading policies.

Looking back at history, "election trading" usually goes through three stages: the rapid changes in the advantages of the winning party before the election, the "unexpected" election results after the election, and the determination of the continuity/reversal of trading based on policy implementation.

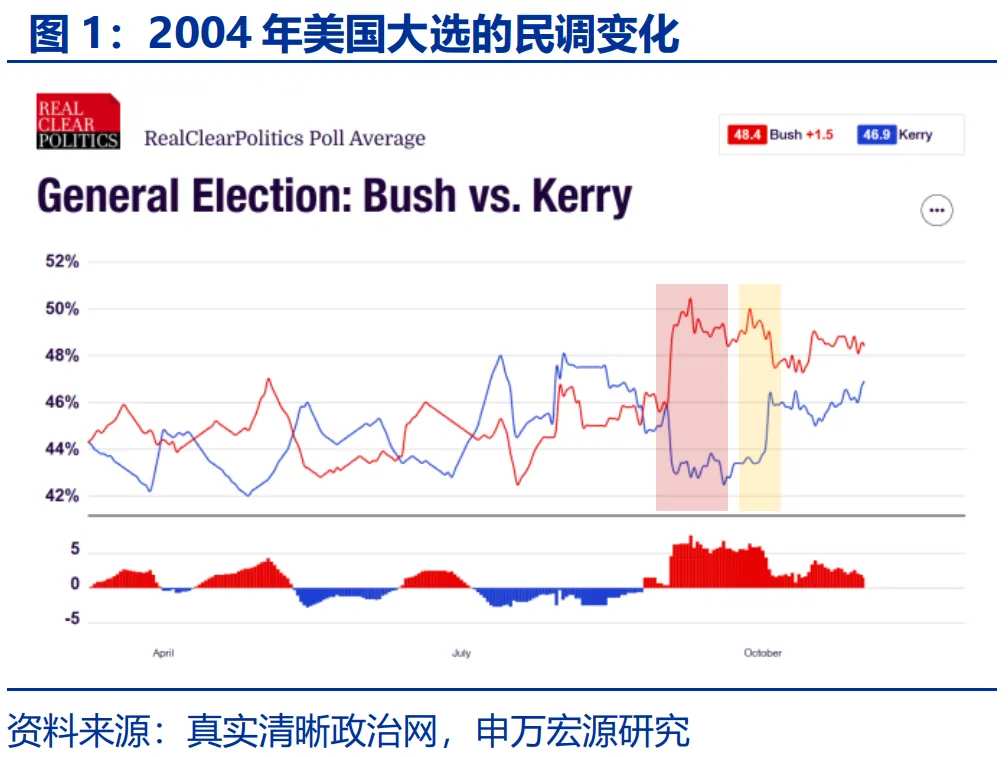

In the first stage, when the advantage of the winning party rapidly expands/contracts, "election trading" will start early. The US presidential election is divided into party primaries and the presidential election. Primaries usually end around the end of August, when the candidates and their policies become clearer, and the market gradually begins trading based on the "policy differences". For example, in the 2004 election between Bush and Kerry, their main policy differences were on traditional energy attitudes and when the Iraq war would end. The shooting incident on September 2 significantly boosted Bush's chances of winning, leading to a rise in energy equipment and defense military stocks. However, after the debate loss on September 30, the excess returns of these two sectors quickly reversed. In 2008, Obama's probability of winning continuously expanded after his formal nomination, and trading around Obama's healthcare reform started in mid-September.

In the second stage, after the election results are known, the market will price in the "unexpected" outcomes of the election. The differences between predictions in the betting markets and the polls have categorized elections since 1936 into four scenarios: "reversal of outcome", "win under high suspense", "win under low suspense", and "win without suspense". Under the reversal scenario, the market shows a significant reversal compared to the previous three months, with the 2016 election being a typical example. In scenarios where the winner is unclear until the last moment, the market continues in the same direction for over a month. If the winner is clear early on, the market's reaction after the election is weak, lasting only around 10 trading days. In cases where the victory is certain early on, the market's initial pricing is relatively adequate, leading to a weaker and shorter reaction after the election, as seen in the 2020 election.

In the third stage, the implementation/failure of core policies will restart/reverse previous trades. For example, in 2017, under promises of tax cuts and trade conflicts during the election, the market responded to the "Trump trade" with "strong US stocks" and "strong US dollar". However, on March 25, 2017, the failure of the new healthcare reform bill led to a rapid decline in US stocks and a significant weakening of the US dollar on that day. The bill was the first key legislation Trump attempted to enact, but internal disagreements led to its withdrawal before the House vote, significantly impacting market confidence and causing a notable reversal in the Trump trade. It wasn't until early November that the successful advancement of a tax reform bill restored market confidence in Trump's policies, and the Trump trade resumed during the progress of the tariff bill in 2018.

Taking the 2016-2019 Trump trade as an example, both the second and third stages of the "Trump trade" were played out. During the first stage from early September 2016 to November 7, until the election day, polls and betting leaned towards Hillary, causing the S&P 500 index to decline and the US dollar index to fluctuate, with the Trump trade yet to begin. In the second stage from November 8 to December 31, 2016, the election "surprise" was quickly priced in, leading to a surge in the US dollar index and a big rise in the S&P 500 index. After the cancellation of the new healthcare reform bill on March 15, 2017, the US dollar index continued to weaken, temporarily reversing the Trump trade. It wasn't until February 2018 that the implementation of the 201 and 232 tariffs boosted market confidence in trade policy, strengthening the US dollar index and restarting the Trump trade.

Second, how does the market conduct "Trump trading"? A strong US dollar has higher certainty, tilting towards US stocks and copper, while US bonds and gold lean towards negative.

The current interpretation of the "Trump trade" in the market mainly focuses on viewing the market from a policy standpoint, but the impact of a series of campaign proposals by either candidate on assets may vary. By examining market transactions themselves, some of this divergence can be mitigated. On one hand, the effect of different policies proposed by Trump or Harris may be opposite on certain types of assets; for example, Trump's policies such as lowering corporate taxes, increasing tariffs, and supporting industrial production tend to strengthen the US dollar, yet he also attempted a "weak dollar plan". The actual trend of the US dollar in the Trump trade cannot be ascertained solely from the policies. On the other hand, both candidates share similarities in some policies, such as promoting US industrial production, but the impact of their "policy differences" on copper, cyclical stocks, and more is hard to measure. The market's response during the first stage of the "Trump win" trading provides answers to these questions.

Perspective 1: Focus on the performance of major asset classes during the two debates. On the evening of June 27th, 9:00 p.m. Eastern Time, Trump and Biden had their first presidential debate, where Trump clearly had the upper hand, establishing a significant advantage over Biden. During the debate, the S&P 500 index and the Nasdaq index soared, the US Dollar Index strengthened, US bond yields rose, LME copper quickly rose, Bitcoin went up, Brent crude oil prices slightly rose, and COMEX gold was under pressure. From this performance, the 'Trump trade' may have the characteristics of boosting the US Dollar, raising US bond rates, positive for US stocks, copper, Bitcoin, etc., bearish for gold, and has a weaker impact on crude oil prices.

During the debate with Harris on September 10th, Trump was at a disadvantage, and the market trend during this period may be opposite to the 'Trump trade'. During the debate under 'Harris trade,' the S&P 500 index and Nasdaq index quickly weakened after opening, the US Dollar Index weakened, US bond yields declined, copper and oil prices resonated and rose, Bitcoin fell, and gold slightly rose. From the market performance, Trump and Harris' policies, still characterized by a strong US Dollar, raising US bond rates, positive for US stocks and Bitcoin, bearish for gold, while indications regarding copper and oil prices that were more contradictory may have been disrupted by OPEC's lowering of global oil demand growth expectations for the next two years on the evening of September 10th.

Perspective 2: The correlation between Trump's election advantage and excess returns. In the past 90 trading days, as the presidential debates began, asset pricing began to consider the impact of 'election trade'. From June 17th to date, looking at the correlation between various assets and the betting market's Trump win rate, 1) the 10-year US bond yield and the US Dollar Index have a correlation with Trump's win rate as high as 0.77 and 0.70, where Trump's trade has the most certainty in pushing up US bond yields and supporting a strong US Dollar; 2) Bitcoin, Nasdaq have a correlation with Trump's win rate of 0.46 and 0.44, also benefiting significantly from Trump's trade; 3) Brent crude oil, LME copper, and S&P 500 have a weak positive correlation with Trump's win rate, positive for copper and oil, seeming to have some policy interpretation differences; 4) Gold shows a weak negative correlation with Trump's win rate.

Perspective 3: Performance of major asset classes during the 'Trump trade' in 2016. After Trump's unexpected victory on November 8, 2016, there was an evident reversal in many major asset markets, displaying typical characteristics of the 'Trump trade'. As of December 31, 2016, US bond yields rose rapidly by 59 basis points, the US Dollar Index increased by 4.4%; in the equity markets, the S&P 500 and Nasdaq rose by 4.6% and 3.7% respectively; in the commodity markets, Brent crude oil surged by 23.4%, LME copper rose by 5.7%, and COMEX gold plummeted by 10.0%; in other assets, Bitcoin surged by 33.8%.

Overall, in the 'Trump trade', the rise in US bond yields, a stronger US Dollar, and an increase in Bitcoin have a higher certainty, trading towards being bullish for US stocks and copper, bearish for gold, with uncertainty regarding oil price impacts. Looking at the direction of the impact of the 'Trump trade', categories that have certain differences from a policy perspective are mainly copper, gold, and oil. While commodity prices will also be disturbed by multiple other factors, based on previous trading results, the 'Trump trade' may not necessarily be 'bearish on copper and oil, bullish on gold'.

1) Regarding copper, Trump does not completely restrict the new energy sector. During his tenure, the production of natural gas and renewable energy in the USA hit record highs. The subsidy for clean energy increased from 7.1 billion USD in 2017 to 17.3 billion USD in 2020. Additionally, tax reductions, reindustrialization, and other economic stimuli will boost the demand for copper. 2) Concerning gold, Trump's reelection will to some extent interrupt policy continuity, increase market uncertainty, but the high certainty of Trump's policies in pushing up US bond yields is still bearish for gold. Moreover, Trump's contraction in geopolitics is favorable for reducing geopolitical risks. In addition, an expanded deficit does not necessarily lead to a surge in central bank gold purchases, as central bank gold purchases are mostly driven by security factors, rather than directly related to US bond credit.

2) Regarding gold, Trump's reelection will to some extent interrupt policy continuity, increase market uncertainty, but the high certainty of Trump's policies in pushing up US bond yields is still bearish for gold. Moreover, Trump's contraction in geopolitics is favorable for reducing geopolitical risks. In addition, an expanded deficit does not necessarily lead to a surge in central bank gold purchases, as central bank gold purchases are mostly driven by security factors, rather than directly related to US bond credit.

For further analysis, please refer to the report 'Under the New Highs, Is It 'Gold'?'

On the oil front, Trump holds an energy expansion policy. However, on one hand, the U.S. shale oil production capacity is already near a high point, and there is still a long delay from the issuance of licenses to supply increases. On the other hand, policies like industrialization may weaken Trump's energy policy's bearish impact on oil prices to some extent.

For more analysis, refer to the report 'Oil Price Watershed?'

In the equity market, is the 'Trump Trade' noteworthy? CNI large cap.growth index is relatively bullish, focusing on finance, energy and manufacturing.

Regarding the U.S. stock market, structurally, the 'Trump Trade' is relatively bullish for large cap.growth index. According to the odds changes on PredictIt, the 'election trade' since June can be roughly divided into three stages: the first stage, early June to mid-July, Trump's odds of winning significantly increased; the second stage, mid-July to early August, Harris's emergence led to a sharp decline in Trump's chances of winning; the third stage, since mid-September, Trump trade has revived due to Harris's poor interview performance. From a market relative performance perspective, in the first and third stages, large cap and growth clearly have the advantage; in the second stage, large cap and growth significantly weakened. Logically, Trump's tax cuts, technology, and other policies are bullish for growth sectors, while the upward risk to U.S. bond yields from his policies may pressure small cap stocks relatively.

By industry, you can also evaluate the potential bullish and bearish effects from the excess returns during the 'Trump Trade' period.1) Looking at the intraday returns on debate days, industries that were bullish after Trump's dominance on the night of June 27 should perform well the next day in favor of Trump trade, while those industries should reverse the next day when Trump performed poorly on the night of September 10.2) Looking at the various stages of the Trump candidacy, from June 27 to July 16, and from September 18 till now, both are stages of Trump's increased odds of winning, which should favor 'Trump Trade' targets; while from July 17 to August 11, the phase of Harris's significantly increased odds, weak industries may be more characteristic of 'Trump Trading'.

Furthermore, one can examine the correlation of industry index market performance with Trump's winning chances. Since June 17, sectors like air transportation and logistics, building materials, energy equipment and services, semiconductors, and banks have a high positive correlation with Trump's winning odds, at 0.61, 0.55, 0.49, 0.47, 0.47 respectively; whereas industries like life sciences, food, personal care products, medical care suppliers and services, and biotechnology have a higher negative correlation with Trump's winning odds, at -0.63, -0.62, -0.57, -0.56, -0.54 respectively.

Taking into account the excess returns on debate days, various stages of the candidacy's excess returns, and the correlation with Trump's winning odds over the past 90 trading days, industries potentially bullish under Trump can be roughly categorized into four types: 1) banks and consumer finance benefiting from relaxed financial regulations; 2) traditional energy development supportive sectors like energy equipment and services, metals and mining, and oil and natural gas; 3) electric appliances favored by corporate tax deductions; 4) air transportation and logistics, building materials, autos, auto parts, etc.

Industries with potential bearish outlook can also be divided into four types: 1) consumer goods categories like personal care products, beverages, home consumer goods, food, durable consumer goods, etc.; 2) clean energy categories such as electrical utilities; 3) medical care categories like life sciences, pharmaceuticals, medical equipment and services; 4) defense and military industry categories.

The market's consensus is positive towards finance, traditional energy, and tax cuts, while negative towards clean energy. It is worth paying attention to the following categories:

1) Supported by Trump's policy of reindustrialization, industries such as air transportation logistics, building materials, and autos.

2) Relative to Harris' tax cuts and subsidies for low- and middle-income groups, Trump's tax cuts benefit the wealthy more, leading to a negative bias towards essential consumer goods, medical care, and other industries.

3) Trump's contractionary policies on geopolitics lead to a negative bias towards defense and military industries.

Four, the possible interpretation of the 'election trade'? Short-term focuses on unexpected results, mid-term on policy signals, and long-term on fundamentals.

Recently, the probability of Trump's re-election has significantly increased, and the market has once again priced in the possibility. As of October 24th, RCP's aggregation polls show Trump's support at 48.5% and Harris at 48.6%; in September, Trump was once behind by 2 percentage points but has caught up with Harris. Trump leads in all seven swing states; as of October 26th, his lead has widened in Georgia, Arizona, Pennsylvania, Nevada, and Wisconsin compared to the previous week. In the betting markets, the likelihood of Trump's victory is as high as 61%. Since September 23rd, the Trump Group has surged by 268%, reigniting Trump trading.

However, the election outcome is far from certain. In the short term, if Trump wins, the continuation of previous trades may be relatively limited. But if Harris wins, there could be a significant reversal in the previous trades. Looking back at history, the betting markets have not been reliable in predicting election results; out of 22 elections since 1936, 5 have been incorrectly predicted. Polls also have their flaws. This year, uncertainties such as continued mail-in voting, rural-urban population shifts after the pandemic, and new biases in Trump after polling model adjustments could bring about uncertain results. Yet, the market trades are clearly leaning towards Trump. This means that if Trump wins smoothly, the market trend may resemble 2020 and 2012 with a small continuation of earlier trades; but if Harris wins, the market may resemble 2016 with a significant reversal.

In the mid-term, the focus of the market's interpretation lies in the pace and feasibility of the election propositions. 1) Looking at the pace of advancement, the U.S. president can implement policy propositions through executive orders, legislation, etc.; legislation implementation is slower, while executive orders are easier to implement. Historically, Trump's first term swiftly enacted policies in areas like immigration, trade, and regulation through executive orders, but tax policies took longer to materialize. 2) Considering the feasibility, if lacking cooperation from Congress, Harris' tax policies, Trump's tax and energy policies may face obstacles; at the same time, both sides have poor records of fulfilling election promises, with Trump only achieving a 23% policy fulfillment rate in his first term, but a higher rate in the trade sector. The smooth progress or hindrance of policy propositions directly affects the reversal or continuation of the third phase of election trading.

In the long run, the most decisive factor for the pricing of most assets is still the fundamentals themselves, and the impact of elections on the market may be mainly realized through the influence on the fundamentals. From the market trends during the period from 2017 to 2019, when the trade policy implementation drove the restart of the 'Trump trade', US bond yields continued to fall, copper and oil resonated falling, and gold prices surged significantly, seemingly conflicting with the 'Trump trade'; the reason behind this is that the downward economic cycle caused by trade frictions led to a significant weakening of the US economy, dominating the market trends during this period. Looking ahead, the 'election trade' should still return to the fundamentals themselves. At present, this year's election can be divided into four scenarios: Republican full victory (probability: 49%), Trump + divided Congress (probability: 14%), Democratic full victory (probability: 12%), Harris + divided Congress (probability: 21%). According to the magnitude of positive impact on the economy, in order, they are: Democratic full victory > Republican full victory > Harris + divided Congress > Trump + divided Congress.

For more analysis, please refer to the report 'Comprehensive Analysis of the US Presidential Election: Policy Comparison, Macroeconomics, and Asset Implications'.

Risk warning

1. Escalation of geopolitical conflicts. The Russia-Ukraine conflict has not ended, and tensions in the Israeli-Palestinian conflict have risen again. Geopolitical conflicts may intensify fluctuations in oil prices, disrupt the global 'de-inflation' process, and the 'soft landing' expectations.

2. US economic slowdown exceeds expectations. Since May, US economic data has consistently fallen short of expectations, the labor market has slowed down rapidly, the trend of upward pressure on residents' debt repayment and interest payment burden continues, and the slowdown in consumption trends continues.

3. Yen continues to appreciate beyond expectations. Against the background of recession trading and Fed rate cuts, the yen has appreciated significantly. If the yen continues to appreciate significantly, it will hinder the recovery of domestic demand in Japan and the Bank of Japan's normalization process.

Editor / jayden