债券交易商普遍预计债券拍卖规模将连续第三个季度维持在1250亿美元。

债券交易商普遍预计债券拍卖规模将连续第三个季度维持在1250亿美元。The US Department of the Treasury will announce the quarterly refinancing plan of US bonds on Wednesday, and any indications of imminent borrowing increases could further disrupt the US bond market.

After the resilience of the US economy shook investors' confidence in the Fed's future rate cut path, the US bond market also faces doubts about how long the US government can avoid massive borrowing.

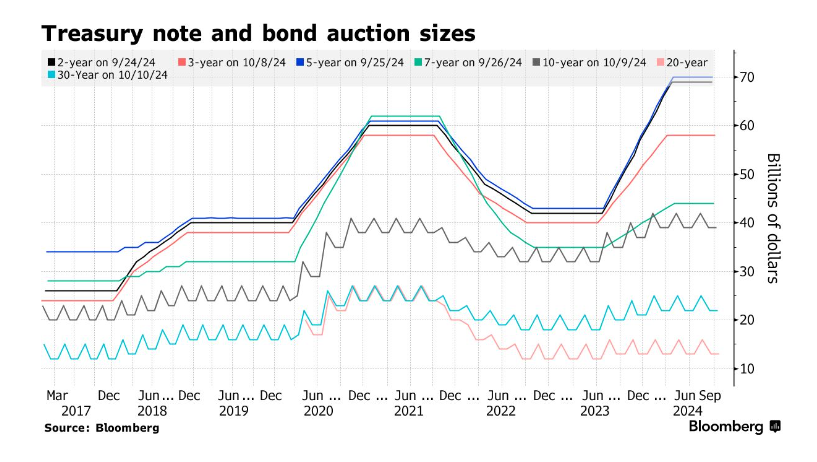

Although the US fiscal deficit remains at historic highs, the Treasury Department has issued guidance since May stating that it will maintain the size of note and bond auctions "at least over the next few quarters" unchanged. The Treasury Department will announce the latest quarterly refinancing plan for US bonds this Wednesday.

Bond traders generally expect the bond auction size to be maintained at 125 billion USD for the third consecutive quarter. The question is whether the guidance on "over the next few quarters" will remain unchanged. If so, it indicates that there will be no increase in issuance of US bonds before mid-2025.

Bond traders generally expect the bond auction size to be maintained at 125 billion USD for the third consecutive quarter. The question is whether the guidance on "over the next few quarters" will remain unchanged. If so, it indicates that there will be no increase in issuance of US bonds before mid-2025.

Due to neither former President Trump nor Vice President Harris making deficit reduction a core element of their election campaigns, the increase in the scale of long-term US debt sales has been seen as inevitable at some point.

Jefferies' senior economist Thomas Simons said, "The reiteration of the borrowing path over the 'next few quarters' seems to be a quite significant commitment repeated by the Treasury Department at this particular time," "They may go ahead with this."

Some US bond auction sizes, including the 10-year Treasury, have reached record levels. Any hints of imminent increases in borrowing could further disrupt the US bond market. In recent weeks, US bond yields have risen sharply. On Monday, as the quarterly refinancing estimate is released, traders will also learn about the Treasury's latest indications of broader borrowing needs.

Phoebe White, head of inflation strategy at JPMorgan USA, said: "Regarding the quarterly refinancing announcement by the Treasury Department, its forward guidance may be somewhat fresh. Therefore, if we see changes in the guidance, some wording being abandoned, then the market may be frightened."

Companies such as JPMorgan, Citigroup, and Royal Bank of Canada's capital markets believe that there will be no changes in the quarterly refinancing scale or forward guidance on Wednesday. Wells Fargo predicts that there may be slight changes in wording, but not enough to anger investors.

"We believe the Treasury Department may adjust their guidance on increasing coupon issuance, but will not imply its urgency," said Angelo Manolatos, strategist at Wells Fargo.

But there is one unknown this time, Wednesday will be the last time the Biden administration team releases the quarterly refinancing announcement.

The next quarter's refinancing plan will take place after the new president takes office. Some of Trump's Republican supporters publicly criticized Treasury Secretary Yellen and her deputies, exacerbating the reliance on short-term notes that will mature over the course of a year to control the issuance and yield of long-term bonds. This indicates that if the Republicans win the White House, the issuance of short-term notes may decrease, while the amount of long-term bonds issued may increase.

If the refinancing scale remains the same, the bond issuance plan for next week will be as follows:

Issuance of $58 billion 3-year Treasury bonds on November 4th

On November 5th, issued $42 billion of 10-year Treasury bonds.

On November 6th, issued $25 billion of 30-year bonds.

Even before any new team took office, debt managers, including Treasury officials, had already been fighting for the restoration of the federal debt limit in early January. Unless Congress quickly suspends or raises the limit, the Treasury will need to initiate a routine used to give itself the most space to continue making payments.

"If the Treasury is constrained by the debt limit after January 1 next year, they wouldn't want to increase coupon supply," said Blake Gwinn, Head of U.S. Interest Rate Strategy at the Royal Bank of Canada Capital Markets. "So, retaining the guidance on stable auctioning for the 'next few quarters' seems to be the best option."

Ira F. Jersey, the Chief U.S. Interest Rate Strategist at Bloomberg Industry Research, believes that the Treasury does not need to change its guidance, as they may even be able to maintain the stability of coupon issuance next year. Given that the Treasury has raised over $1.6 trillion in funds in the 2025 fiscal year, there is hardly any need for adjustments unless unexpected expenditures require funding.

Over the coming months, the Fed's Quantitative Tightening (QT) program may slow down further, even come to an end, which would be beneficial for the Treasury. QT involves allowing a certain amount of treasuries to expire from the Fed's balance sheet without renewal, forcing the Treasury to sell more bonds to the public.

Bond investors will also be watching for the latest news from the Fed regarding interest rate cuts at the policy meeting on November 6th and 7th. Since the Fed began the rate-cutting cycle last month with a 50 basis points rate cut, rising expectations of policymakers lowering the benchmark rate further in subsequent meetings have been subdued, leading to higher bond yields.

Traders predict that the Treasury will maintain the issuance of floating-rate bonds unchanged within the next three months on Wednesday. As for U.S. Treasury Inflation-Protected Securities (TIPS), the issuance in this sector is expected to continue to rise slightly. In a quarterly survey of traders, the Treasury asked whether another type of TIPS bond should be added on top of the existing three.

Editor/Rocky