截至10月28日收盘,恒瑞市值达3100亿元,在国内医药行业当中市值排名第二,仅次于医疗器械龙头迈瑞医疗(3373亿元);如果只算药企的话,恒瑞医药是妥妥的国内“医药一哥”了。

截至10月28日收盘,恒瑞市值达3100亿元,在国内医药行业当中市值排名第二,仅次于医疗器械龙头迈瑞医疗(3373亿元);如果只算药企的话,恒瑞医药是妥妥的国内“医药一哥”了。According to Bloomberg on October 24th, Jiangsu Hengrui Pharmaceuticals is considering a secondary listing in Hong Kong next year and may raise at least $2 billion.

Hengrui Pharmaceuticals announced after the market closed on the same day that in recent years, the company has steadily promoted its internationalization process driven by technological innovation and global development strategies. In order to further deepen the company's strategic development goals, the company has recently conducted preliminary work such as research and consultations on financing in overseas capital markets. As of now, the company has not yet determined specific plans regarding these matters.

As a leading innovative international pharmaceutical company in China, Hengrui Pharmaceuticals focuses on new drug research and development in the fields of anti-tumor, metabolic diseases, autoimmune diseases, respiratory system diseases, and nervous system diseases.

As of the close of trading on October 28th, Hengrui's market cap reached 310 billion yuan, ranking second in the domestic pharmaceutical industry behind only medical equipment leader Mindray Medical (337.3 billion yuan). If only pharmaceutical companies are considered, Hengrui Pharmaceuticals is undoubtedly the top player in the domestic pharmaceutical industry.

As of the close of trading on October 28th, Hengrui's market cap reached 310 billion yuan, ranking second in the domestic pharmaceutical industry behind only medical equipment leader Mindray Medical (337.3 billion yuan). If only pharmaceutical companies are considered, Hengrui Pharmaceuticals is undoubtedly the top player in the domestic pharmaceutical industry.

Since the beginning of this year, A-share companies seeking secondary listings in Hong Kong have become a trend.

On September 17th, the household appliances giant Midea Group was listed on the Hong Kong Stock Exchange, becoming the second home appliance company to be listed on both A-shares and the Hong Kong stock market after Haier Smart Home.

In addition to Midea Group, other companies such as Chifeng Jilong Gold Mining, Hainan Drinda New Energy Technology, S.F. Holding, Jiangsu Lopal Tech, and Zhejiang Shibao are at different stages of listing in Hong Kong.

The fastest among them is Jiangsu Lopal Tech, which is expected to be listed on the Hong Kong Stock Exchange on October 30th. Jiangsu Lopal Tech stated that in order to accelerate the company's internationalization strategy and overseas business layout, enhance the company's overseas financing capabilities, further improve the company's capital strength and overall competitiveness, the company is progressing with this H-share issuance.

In addition, sources say that S.F. Holding is planning to conduct a second listing in Hong Kong by the end of November. S.F. stated in the listing application that the goal of the Hong Kong listing is to build an international platform and advance its global strategy, a goal that has remained unchanged. S.F. also hopes to leverage the Hong Kong stock market platform to further expand its overseas market presence. If this listing in Hong Kong is successful, S.F. will become the first 'A+H' dual-listed company in the express delivery industry.

Recently, the fourth largest global professional manufacturer of photovoltaic batteries, Hainan Drinda New Energy Technology, also submitted a listing application to the Hong Kong Stock Exchange, marking its second attempt after the failed submission in February this year.

01

Currently, there are 149 companies listed with 'A+H', with generally discounted prices in the Hong Kong stock market.

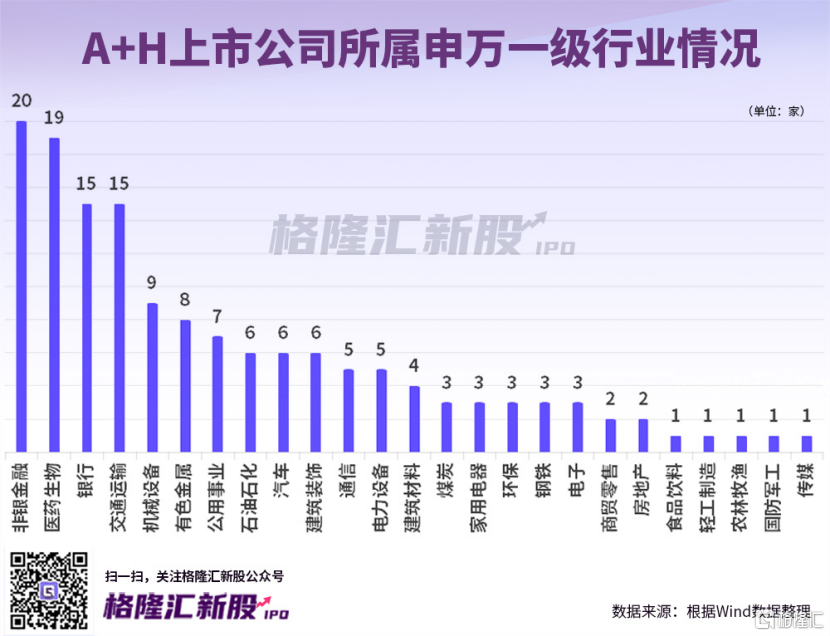

Wind data shows that as of October 28, there are a total of 149 companies listed in both mainland China and Hong Kong (detailed list at the end of the article). In terms of industry distribution, the 149 companies are mainly concentrated in non-financials, healthcare, banks, transportation, machinery, nonferrous metals, and other sectors, mostly comprising large companies within their respective industries.

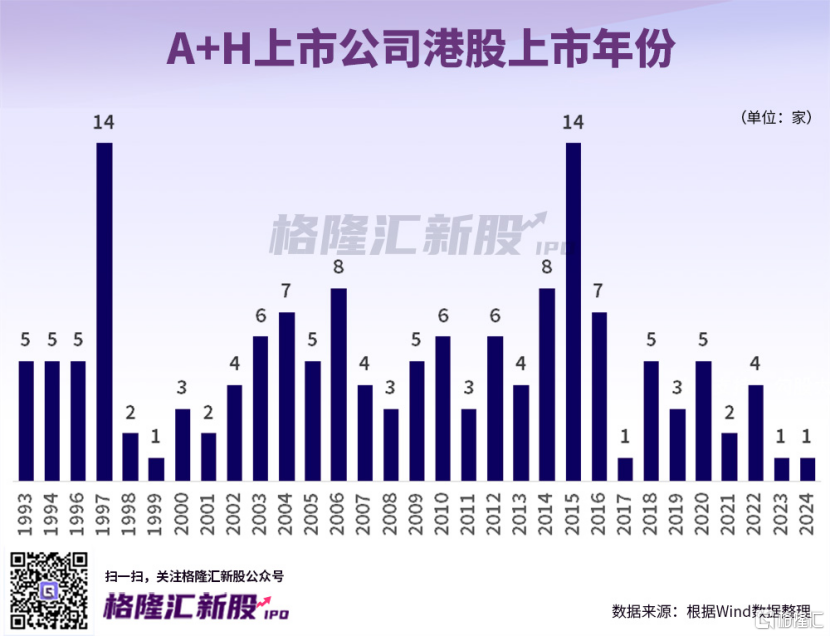

Looking at the years when companies listed in Hong Kong, prior to 2022, the number of A-share companies listed on the Hong Kong stock market was relatively higher, with 1997 and 2015 being two small peaks, seeing 14 companies each year. From 2023 to early 2024 as of October 28, only one company had listed in Hong Kong. However, with the upcoming listings of Jiangsu Lopal Tech. and S.F. Holding, the number in 2024 is expected to quickly rebound from this low point.

It is worth noting that the A/H premium rates of 149 A+H listed companies are all higher than 0%, with an average premium rate of 96%, indicating that all stock prices, after exchange rate conversion, are lower than A-shares in the Hong Kong stock market. The majority of companies' A-share prices are much higher than those in Hong Kong, with 134 companies having a premium rate exceeding 30%.

After news of Jiangsu Hengrui Pharmaceuticals' secondary listing emerged, its stock price fell by 5.58% on Thursday, continuing to decline on Friday, hitting the lowest level since September 27. Industry experts suggest that the probable reason for the stock price drop in Jiangsu Hengrui Pharmaceuticals is market concerns over the A/H premium rates.

Based on the closing price on October 25, the company with the highest premium rate is Zhejiang Shibao, reaching 298%, meaning that Zhejiang Shibao's A-share market cap is almost four times that of its Hong Kong shares; while the lowest is Midea Group Co., Ltd., with a 5% premium rate.

Looking at it by industry, the A/H premium rates for the agriculture, electronics, and light manufacturing industries rank in the top three, while the household appliances, food and beverage, and banking industries have relatively lower A/H premium rates.

In a research report by Sealand last year, it was pointed out that there is a significant difference in stock prices between A+H listed companies in both places, with fairly complex reasons behind it.

Firstly, the Hong Kong stock market is a relatively unique market. Investors in Hong Kong investing in A+H stocks have their liabilities denominated in US dollars, with interest rates affected by the US economic cycle. Their assets are denominated in RMB, influenced by China's macroeconomic environment. Hong Kong investors' cost of capital is linked to US dollar interest rates, while A-share investors' cost of capital is linked to RMB interest rates.

Currently, the interest rate differential between China and the USA remains at a high level, to some extent causing differences in the cost of capital for investors in the A/H markets, leading to pressure on Hong Kong stock prices and theoretically expanding the A/H premium.

In addition, the Hong Kong stock market is relatively mature, with the majority of investors being international institutional investors who have rich investment experience and more rational investment behavior. On the other hand, the A-share market has a higher proportion of individual investors, leading to stronger randomness in pricing.

At the same time, due to factors such as exchange rates and market mechanisms, arbitrage between A-shares and Hong Kong stocks is not possible, resulting in the inability to converge price differences and the continuous existence of premiums.

Although for investors, after listing in Hong Kong, the stock prices are mostly relatively discounted compared to A-shares, for the companies themselves, listing in Hong Kong can broaden the company's financing channels and serve as a bridgehead linking international capital markets, facilitating deeper overseas funding awareness of the company and promoting the company's business expansion overseas.

Regarding this point, Jiangsu Hengrui Pharmaceuticals stated in the third-quarter report that the company is actively exploring cooperation with various partners such as multinational pharmaceutical companies, innovative startups, innovation investment funds, and regional leading pharmaceutical companies with a global perspective, seeking cooperation opportunities with leading pharmaceutical companies worldwide to achieve rapid transformation of research and development results and cover overseas markets with the help of international partners, accelerate integration into the global pharmaceutical innovation network, and maximize product value.

02

Mainland companies' IPOs in Hong Kong are inseparable from policy support.

The acceleration of mainland companies' listing in Hong Kong is dependent on policy support.

On October 18, 2024, the China Securities Regulatory Commission and the Hong Kong Stock Exchange issued a joint statement announcing the optimization of the timetable for new listing application approval process to further enhance Hong Kong's attractiveness as a leading international IPO market in the region.

The joint statement listed three specific optimization measures, one of which is for companies listed on the A-share market to list in Hong Kong.

The joint statement stated that companies already listed on the A-share market in Hong Kong can apply for new listings if they meet the following conditions: (1) Expected market cap of at least 10 billion Hong Kong dollars; and (2) Based on legal opinions, confirming that the company has complied with all relevant laws and regulations related to A-share listings in the two full financial years before submitting the new listing application, their new listing application can be expedited for approval according to the fast approval timetable for eligible A-share companies.

Under the fast approval timeline for eligible A-share companies, if eligible A-share listed companies submit applications that fully comply with regulations, the SFC and HKEX will each issue only one round of regulatory comments. In this case, the regulatory assessments of the two regulatory bodies will be completed in no more than 30 business days respectively.

As early as April 19 this year, the China Securities Regulatory Commission issued 5 measures for cooperation with Hong Kong's capital markets, pointing out that the commission will further enhance communication and coordination with relevant departments, support leading mainland industry enterprises that meet the criteria to raise funds by listing in Hong Kong, and support leading mainland industry enterprises to list in Hong Kong.

This year, the Hong Kong Stock Exchange has also introduced many new measures, such as lowering the minimum listing threshold for special technology companies, increasing market inclusiveness, and attracting more innovative companies to IPO in Hong Kong.

According to Wind data, stimulated by a series of domestic policies, trading in the domestic stock market quickly picked up after "924", with the Hong Kong stock market reaching a historical high trading volume of 505.9 billion Hong Kong dollars on September 30, while the average daily turnover in August was only over 90 billion Hong Kong dollars.

Furthermore, the Hong Kong stock market is deeply influenced by global liquidity. Since the US Federal Reserve opened a rate-cutting channel in September, it has also helped improve the liquidity of the Hong Kong stock market.