整体来看,上述五家银行今年前三季度资产规模均在持续扩张,业绩表现却略有分化。其中,除平安银行营收出现两位数降幅外,其余四家银行营收及净利润均有不同程度增长,但各家增幅也同样参差不齐。

整体来看,上述五家银行今年前三季度资产规模均在持续扩张,业绩表现却略有分化。其中,除平安银行营收出现两位数降幅外,其余四家银行营收及净利润均有不同程度增长,但各家增幅也同样参差不齐。The current disclosed financial reports of the five listed banks show that their assets have continued to expand in the first three quarters of this year, with most of them experiencing some growth in performance, but the specific performance varies slightly.

As October gradually comes to an end, the quarterly reports of listed banks are also being released one after another.

As of October 25, Ping An Bank, Bank of Hangzhou, Bank of Nanjing, Jiangsu Changshu Rural Commercial Bank, and Shanghai Rural Commercial Bank, five A-share listed banks, have successively disclosed their operational results for the first three quarters of this year.

Overall, the asset size of the aforementioned five banks has continued to expand in the first three quarters of this year, with performance showing slight differentiation. Among them, except for Ping An Bank which experienced a double-digit decline in revenue, the other four banks all saw varying degrees of growth in revenue and net income, but the growth rates are also uneven.

Overall, the asset size of the aforementioned five banks has continued to expand in the first three quarters of this year, with performance showing slight differentiation. Among them, except for Ping An Bank which experienced a double-digit decline in revenue, the other four banks all saw varying degrees of growth in revenue and net income, but the growth rates are also uneven.

According to the analysis of China International Capital Corporation, the performance of listed banks in the third quarter of this year was relatively flat, with net interest margin still being the main factor affecting revenue, but the decline in net interest margin is narrowing. However, factors such as policy catalyzing the improvement of bank asset quality expectations and increased dividend certainty will be key variables affecting bank stock prices.

Profits of the five listed banks have all grown, while the downward trend in net interest margin continues.

In terms of performance, among the five listed banks that have already disclosed their quarterly reports, all except for Ping An Bank have achieved positive growth in operating income.

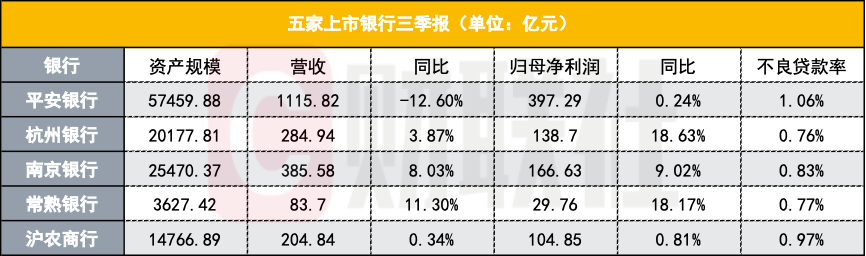

Among them, Ping An Bank's revenue for the first three quarters was 111.582 billion yuan, a year-on-year decrease of 12.60%; Shanghai Rural Commercial Bank's revenue was 20.484 billion yuan, a year-on-year increase of 0.34%; Bank of Hangzhou's revenue was 28.494 billion yuan, a year-on-year increase of 3.87%; Bank of Nanjing's revenue was 38.558 billion yuan, a year-on-year increase of 8.03%; Jiangsu Changshu Rural Commercial Bank's revenue was 8.37 billion yuan, a year-on-year increase of 11.30%.

From the perspective of net income, in the first three quarters of this year, the profitability of the five banks mentioned above has all achieved varying degrees of improvement, but the overall profit growth rate differences are more pronounced.

Among them, bank of hangzhou's attributable net income for the first three quarters was 13.87 billion yuan, jiangsu changshu rural commercial bank was 2.976 billion yuan, with year-on-year increases of 18.63% and 18.17%, respectively, leading among the five banks. Next, bank of nanjing's attributable net income was 16.663 billion yuan, with a year-on-year increase of 9.02%. Ping An Bank and Shanghai Rural Commercial Bank saw increases of less than 1%, achieving attributable net incomes of 39.729 billion yuan and 10.485 billion yuan, corresponding to growth rates of 0.24% and 0.81%.

In terms of interest spread, only Ping An Bank and jiangsu changshu rural commercial bank among the five banks disclosed their interest spread levels for the first three quarters. However, looking at the current data, the banking industry as a whole still faces significant downward pressure on interest spreads. Specifically, Ping An Bank's net interest margin for the first three quarters was 1.93%, down 54 basis points from the same period last year; jiangsu changshu rural commercial bank's net interest margin was 2.75%, down 20 basis points from the same period last year.

Regarding the significant year-on-year decline in interest spreads in the first three quarters, Ping An Bank explained that it was mainly due to the bank's commitment to benefiting the real economy, actively adjusting its asset structure, and being impacted by factors such as the downward trend in market interest rates, insufficient effective credit demand, and loan repricing, leading to an overall decrease in the average loan yield, resulting in a decline in net interest margins.

At the same time, Shanghai Rural Commercial Bank further stated that as interest spreads continue to narrow, the bank will closely follow policy guidance, actively respond to market changes, strengthen forward-looking analysis and refined management, optimize its asset-liability structure, and strive to achieve interest spread performance better than the industry average level.

Continuous expansion of asset size, significant decrease in provisioning level.

Overall, in terms of total assets, the aforementioned five banks that have disclosed financial reports have all achieved further expansion of asset size in the first three quarters of this year.

As of the end of September, the total assets of bank of nanjing were 2547.037 billion yuan, an increase of 11.31% from the end of the previous year, the largest among the five banks. Next, the total assets of bank of hangzhou were 2017.781 billion yuan, jiangsu changshu rural commercial bank's total assets were 362.742 billion yuan, and the total assets of Shanghai Rural Commercial Bank were 1476.689 billion yuan, with growth rates of 9.58%, 8.46%, and 6.07% respectively compared to the end of the previous year. Relatively speaking, the total assets of Ping An Bank were the highest among the five banks at 5745.988 billion yuan, but at the same time, its growth rate was relatively small, at 2.80%.

In addition, in terms of asset quality, the three largest commercial banks maintained a relatively stable non-performing loan ratio in the first three quarters, but the provisioning coverage ratio showed varying degrees of decline.

As of the end of September, the non-performing loan ratios of Ping An Bank, Bank of Hangzhou, and Shanghai Rural Commercial Bank remained unchanged from the end of last year, at 1.06%, 0.76%, and 0.97% respectively. At the same time, the non-performing loan ratio of bank of nanjing decreased by 0.07 percentage points to 0.83% compared to the end of the previous year, while jiangsu changshu rural commercial bank's non-performing ratio increased by 0.02 percentage points to 0.77%.

In terms of risk coverage ability, Ping An Bank's provisioning coverage ratio at the end of September was 251.19%, down 26.44 percentage points from the end of the previous year; Bank of Hangzhou's coverage ratio was 543.25%, down 18.17 percentage points; bank of nanjing's coverage ratio was 340.40%, down 20.18 percentage points; jiangsu changshu rural commercial bank's coverage ratio was 528.40%, down 9.48 percentage points; Shanghai Rural Commercial Bank's coverage ratio was 364.98%, down 40 percentage points.

Regarding asset quality, bank of nanjing stated that in the fourth quarter, it will continue to enhance the foresight of risk prevention and control, deepen credit risk investigation and early warning management, strengthen risk customer segmentation and classification disposal, to ensure the asset quality remains excellent. Meanwhile, Shanghai Rural Commercial Bank also mentioned that it will continuously improve the credit risk management system in accordance with external regulatory dynamics and internal business development needs, strengthen post-loaning management and non-performing asset management, to maintain the continuous stability of credit asset quality.