据此,高盛将印度股市从超配下调至中性,NIFTY指数12个月目标为27000点,意味着9%的上涨空间。短期目标为24500点(-1%)和25500点(+3%)。

据此,高盛将印度股市从超配下调至中性,NIFTY指数12个月目标为27000点,意味着9%的上涨空间。短期目标为24500点(-1%)和25500点(+3%)。Goldman Sachs warns that the valuation of the Indian stock market is currently at historical peak levels, with overvaluation still being the most common concern for investors. As the economic cycle slows down and affects corporate profits, the Indian market may experience fluctuations in the next 3-6 months. Recently, signs of weakness have appeared in the Indian stock market, with the benchmark index NSE Nifty 50 falling by over 5% since October, potentially marking the worst single-month performance in four years.

Goldman Sachs has downgraded its stock rating for the Indian market from shareholding to neutral. Analysts warn that due to weak corporate profit outlook, market high valuation, and weak external support, the Indian stock market will experience volatility in the short term, and investors are advised to shift their focus to high-quality companies with high profit visibility.

In a research report released by Goldman Sachs analyst Sunil Koul on October 22nd, it was mentioned that the overall valuation of the Indian stock market has reached 24 times the expected earnings (24x Fwd earnings), which is at a historical peak. High frequency indicators indicate that the Indian economic growth is currently undergoing a cyclical slowdown, which will drag down corporate profit performance. Historical experience shows that when company valuations are high and profits are cut, the market may experience volatility in the next 3-6 months.

Based on this, Goldman Sachs has downgraded the Indian stock market from overweight to neutral, with a 12-month target of 27,000 points for the NIFTY index, indicating a 9% upside. The short-term targets are 24,500 points (-1%) and 25,500 points (+3%).

Based on this, Goldman Sachs has downgraded the Indian stock market from overweight to neutral, with a 12-month target of 27,000 points for the NIFTY index, indicating a 9% upside. The short-term targets are 24,500 points (-1%) and 25,500 points (+3%).

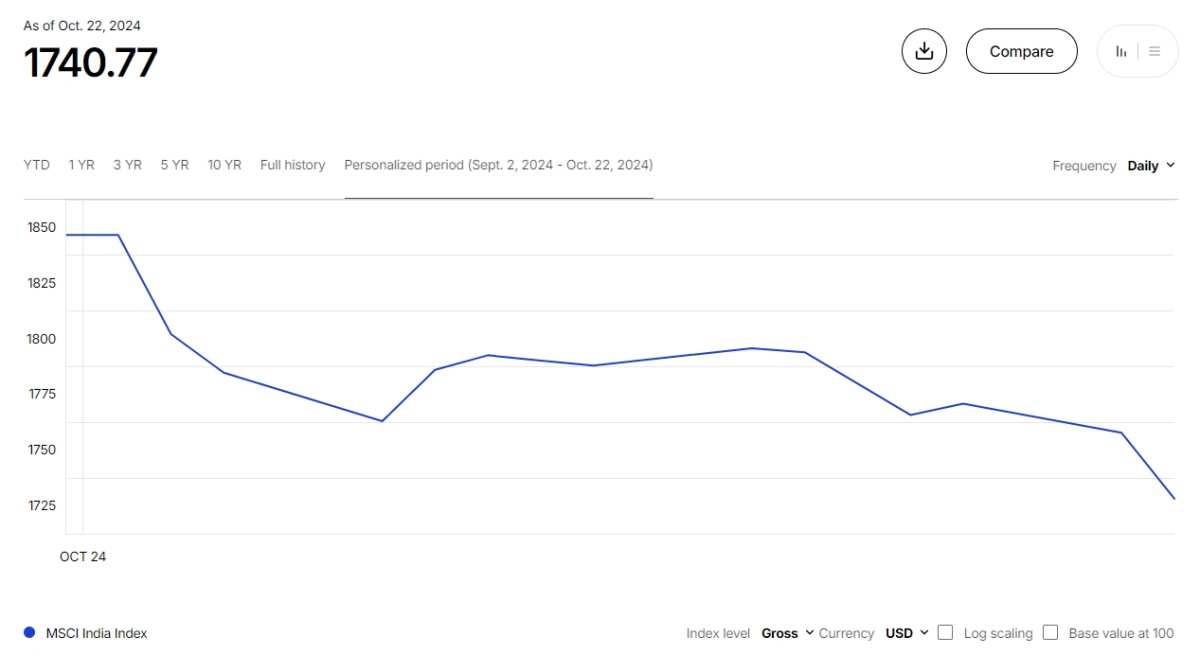

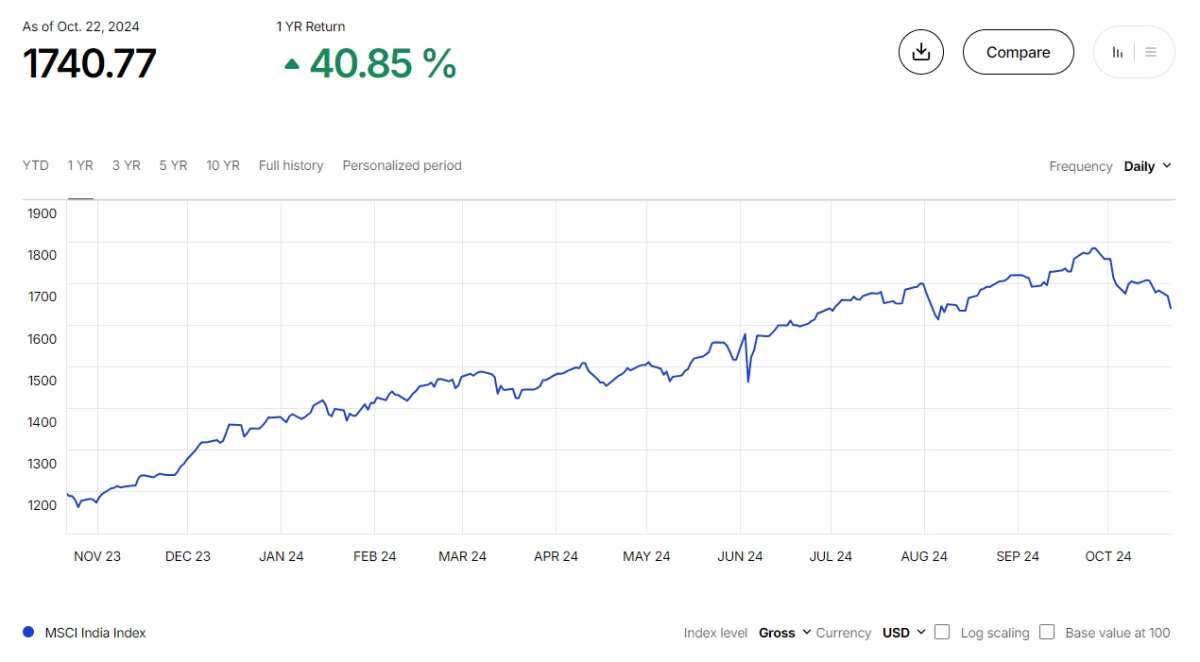

Public information shows that Goldman Sachs raised its stock rating for the Indian market to shareholding at the end of last year, and since then the MSCI India index has risen by over 35%. However, signs of weakness have recently appeared in the Indian stock market, with the benchmark index NSE Nifty 50 falling by over 5% since October, potentially marking the worst monthly performance in four years.

Economic slowdown damages corporate profits.

Goldman Sachs stated that the Indian stock market has performed strongly in the past two years, with the MSCI India index rising by 43% since the beginning of last year (21% growth in emerging markets during the same period). The performance of India's mid-small cap index has been even more remarkable, nearly doubling in the past two years.

However, in the past quarter, many countries globally have experienced a cyclical slowdown in growth. India is no exception, as high-frequency indicators show that economic activity in India is generally slowing down.

In terms of investment, influenced by the elections, capital expenditure of the Indian central government contracted significantly in the second quarter, although there was some recovery in the third quarter. However, comparing the capital expenditure year-to-date (FYTD), it has decreased by 20%. Contract award activity for the quarter ending in September 2024 remains weak (down by 30% year-on-year).

Apart from highlights such as electrical utilities, private capital expenditure in India has not fully recovered. The residential sector has been strong in recent years, but the growth's second derivative is gradually weakening.

In terms of consumer aspects, urban demand indicators such as car sales and gasoline consumption have slowed down, while rural indicators show mixed signals. Recent survey data is also indicating a slowdown, with the September service sector Purchasing Managers' Index (PMI) dropping to a 10-month low of 57.7.

Due to several factors, Goldman Sachs economists currently predict that India's real GDP growth for the fiscal year 2024 may decline to 6.7% year-on-year (30 basis points lower than the market consensus) and drop to 6.5% year-on-year for the fiscal year 2025 (40 basis points lower than the market consensus).

Goldman Sachs warns that lower-than-expected economic growth might impact corporate profit expectations. Sensitivity models show that a 50 basis point decrease in nominal Gross Domestic Product (GDP) growth could result in a 200 basis point decrease in annual earnings per share for MSCI India companies.

The economic slowdown is beginning to impact company profits.

Goldman Sachs warned that the slowdown in economic growth has begun to impact corporate profits.

Over the past month, the sentiment on profits in the BSE 200 Index of the Mumbai Stock Exchange (measured by the breadth of analyst revisions) has deteriorated sharply, approaching a low point in nearly a year. Profit revisions have been lagging, with earnings per share of the MSCI India Index down only 1% in the past month, but the pace of downgrade accelerated last week.

The ongoing earnings season continues this soft tone. Out of the 18 MSCI India companies that have reported performance so far, 11 have fallen short of expectations. While the overall consensus expectations for the 2Q reporting season seem decent, they are driven by a few industries.

Goldman Sachs' Indian stock analysts have lower expectations than consensus across most industries, with the biggest differences in cyclical investment industries (industrial, cement/chemical). This suggests that as the next 3-4 weeks of the earnings season progress, profits may be further downgraded.

Increased probability of short-term pullback due to high valuation.

Goldman Sachs emphasizes that high valuations remain the most common concern for investors.

The expected PE ratio of the MSCI India Index is close to 24 times, 2.1 standard deviations above its 20-year historical average, and at peak valuation levels seen in 2007 and 2021.

In terms of relative valuation, compared to the Morgan Stanley Asia Pacific ex Japan Index (MXAPJ), the current 70% PE premium is relatively high, compared to the 55% average of the past 5 years.

Although strong growth and domestic fund support may keep the valuation at high levels, since June, the current risk return measured by the Price-Earnings Growth Ratio (PEG) has worsened due to slowing growth and rising valuation. More importantly, historical data indicates that when the initial valuation is high (PE ratio greater than 20 times) and earnings expectations are lowered, the return rate for the next 3-6 months will be lower.

Goldman Sachs pointed out that the regional capital flow in the Asian market is also intensifying the pressure on the Indian market. With China's strong policy deployment, there are signs of regional capital shifting towards the Chinese market.

In the past two weeks, India has seen around $8 billion of foreign selling, marking the fourth largest foreign institutional investor (FII) selling in India's history in absolute US dollar terms, with emerging markets and Asian funds reducing their exposure in India over the past month while increasing their exposure in China and other North Asian markets.

Regulatory and external environment factors are also increasing uncertainties.

Goldman Sachs believes that high oil prices and domestic regulatory actions in India have also dampened the short-term uptrend in the Indian market.

The Middle East accounts for 16% of India's commodity exports, over half of India's remittances, in addition to service exports, providing cushion for India's external balance and strengthening its macroeconomic resilience. Any escalation in the Middle East tensions and its potential impact on trade, remittances, especially oil, could create pressure on India's macroeconomic indicators.

Meanwhile, compared to other markets, the Indian market often underperforms during periods of sharp oil price increases. Ongoing news coverage of the Middle East tensions may keep oil price volatility high, exerting pressure on the Indian market in the short term.

Regulatory crackdown in India will affect short-term speculative sentiment among retail investors.

In recent years, the trading activity of derivatives on the India index has surged, with the nominal total trading volume of options and futures ranging between $4-5 trillion per day. This growth is driven by an increase in retail participation, the introduction of short-term index options contracts, and an increase in speculative trading volume at maturity.

This has raised concerns among market regulatory agencies. Earlier this month, the Securities and Exchange Board of India (SEBI) announced six new measures to regulate activities in the index derivatives market. While the effective implementation of these measures has a positive impact on medium-term market stability and strengthens investor protection, it may affect retail trading activities and sentiments, leading to recent market volatility.

A massive number of IPOs are also diverting market funds.

So far this year, the total value of Indian stock issuances has surpassed previous highs, currently reaching a record $45 billion. According to various media reports, the number of companies applying for initial public offerings in September set a record, and the remaining issuance plans for the year also seem substantial ($6 billion). Although domestic fund inflows have been strong so far, helping absorb stock supply, a slowdown in corporate earnings and outflows of foreign capital may lead to supply-demand imbalances, putting pressure on the market in the short term.

Given the above discussions, Goldman Sachs recommends investors reduce their investments in cyclical stocks and focus on sectors with high earnings visibility. Overweight in internet, real estate, autos, telecommunications, and insurance industries, neutral in industrial (transportation, infrastructure), pharmaceuticals, and durable goods industries.