Key Insights

- Tai Sin Electric will host its Annual General Meeting on 29th of October

- Salary of S$493.7k is part of CEO Bernard Lim's total remuneration

- The overall pay is 885% above the industry average

- Tai Sin Electric's EPS declined by 5.5% over the past three years while total shareholder return over the past three years was 18%

Despite Tai Sin Electric Limited's (SGX:500) share price growing positively in the past few years, the per-share earnings growth has not grown to investors' expectations, suggesting that there could be other factors at play driving the share price. Some of these issues will occupy shareholders' minds as the AGM rolls around on 29th of October. One way that shareholders can influence managerial decisions is through voting on CEO and executive remuneration packages, which studies show could impact company performance. From the data that we gathered, we think that shareholders should hold off on a raise on CEO compensation until performance starts to show some improvement.

Comparing Tai Sin Electric Limited's CEO Compensation With The Industry

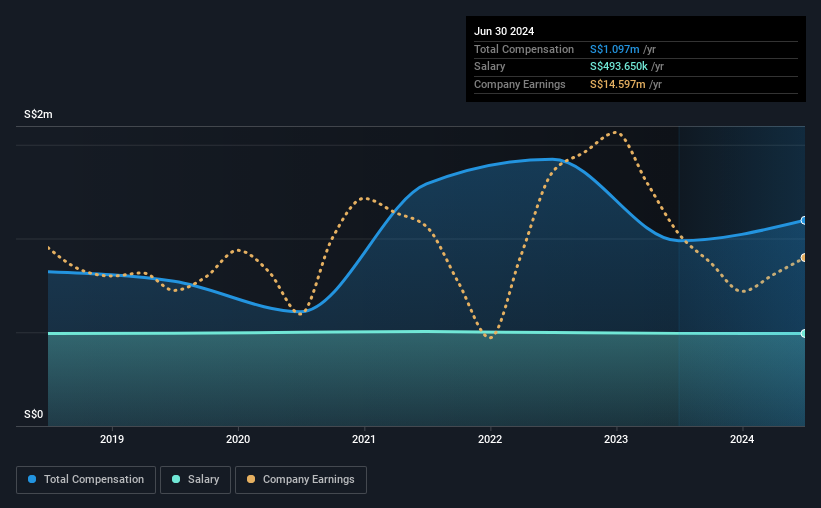

Our data indicates that Tai Sin Electric Limited has a market capitalization of S$184m, and total annual CEO compensation was reported as S$1.1m for the year to June 2024. We note that's an increase of 11% above last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at S$494k.

In comparison with other companies in the Singapore Electrical industry with market capitalizations under S$263m, the reported median total CEO compensation was S$111k. This suggests that Bernard Lim is paid more than the median for the industry. Moreover, Bernard Lim also holds S$62m worth of Tai Sin Electric stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | S$494k | S$494k | 45% |

| Other | S$603k | S$494k | 55% |

| Total Compensation | S$1.1m | S$988k | 100% |

On an industry level, around 72% of total compensation represents salary and 28% is other remuneration. In Tai Sin Electric's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

On an industry level, around 72% of total compensation represents salary and 28% is other remuneration. In Tai Sin Electric's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Tai Sin Electric Limited's Growth

Over the last three years, Tai Sin Electric Limited has shrunk its earnings per share by 5.5% per year. In the last year, its revenue is down 5.0%.

Overall this is not a very positive result for shareholders. And the fact that revenue is down year on year arguably paints an ugly picture. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Tai Sin Electric Limited Been A Good Investment?

Tai Sin Electric Limited has served shareholders reasonably well, with a total return of 18% over three years. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

Shareholder returns, while positive, should be looked at along with earnings, which have not grown at all recently. This makes us think the share price momentum may slow in the future. The upcoming AGM will provide shareholders the opportunity to revisit the company's remuneration policies and evaluate if the board's judgement and decision-making is aligned with that of the company's shareholders.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 1 warning sign for Tai Sin Electric that investors should think about before committing capital to this stock.

Important note: Tai Sin Electric is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.