David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Accenture plc (NYSE:ACN) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Accenture's Net Debt?

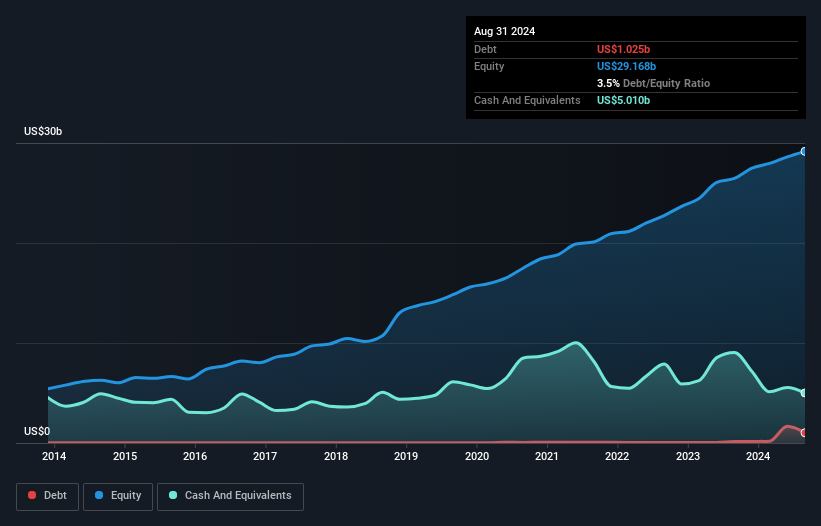

You can click the graphic below for the historical numbers, but it shows that as of August 2024 Accenture had US$1.02b of debt, an increase on US$147.9m, over one year. However, its balance sheet shows it holds US$5.01b in cash, so it actually has US$3.99b net cash.

A Look At Accenture's Liabilities

We can see from the most recent balance sheet that Accenture had liabilities of US$19.0b falling due within a year, and liabilities of US$7.79b due beyond that. Offsetting this, it had US$5.01b in cash and US$13.7b in receivables that were due within 12 months. So it has liabilities totalling US$8.09b more than its cash and near-term receivables, combined.

We can see from the most recent balance sheet that Accenture had liabilities of US$19.0b falling due within a year, and liabilities of US$7.79b due beyond that. Offsetting this, it had US$5.01b in cash and US$13.7b in receivables that were due within 12 months. So it has liabilities totalling US$8.09b more than its cash and near-term receivables, combined.

Since publicly traded Accenture shares are worth a very impressive total of US$235.5b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Accenture boasts net cash, so it's fair to say it does not have a heavy debt load!

While Accenture doesn't seem to have gained much on the EBIT line, at least earnings remain stable for now. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Accenture can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Accenture has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Accenture generated free cash flow amounting to a very robust 90% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Summing Up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Accenture has US$3.99b in net cash. The cherry on top was that in converted 90% of that EBIT to free cash flow, bringing in US$8.6b. So we don't think Accenture's use of debt is risky. Another factor that would give us confidence in Accenture would be if insiders have been buying shares: if you're conscious of that signal too, you can find out instantly by clicking this link.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.