预计到 2024 年,电信和基础设施行业将超过移动和消费行业,成为领先的细分市场,这得益于对人工智能基础设施的大量投资。与此同时,汽车行业正在成为一个主要的增长领域,这得益于该行业向人工智能和先进处理技术的转变。相比之下,预计未来五年智能手机和个人电脑的需求将保持疲软,导致移动和消费行业增长温和,预计复合年增长率约为 5%。

预计到 2024 年,电信和基础设施行业将超过移动和消费行业,成为领先的细分市场,这得益于对人工智能基础设施的大量投资。与此同时,汽车行业正在成为一个主要的增长领域,这得益于该行业向人工智能和先进处理技术的转变。相比之下,预计未来五年智能手机和个人电脑的需求将保持疲软,导致移动和消费行业增长温和,预计复合年增长率约为 5%。Source: Semiconductor Industry Watch. At yesterday's Conputex conference, Dr. Lisa Su released the latest roadmap. Afterwards, foreign media morethanmoore released the content of Lisa Su's post-conference interview, which we have translated and summarized as follows: Q: How does AI help you personally in your work? A: AI affects everyone's life. Personally, I am a loyal user of GPT and Co-Pilot. I am very interested in the AI used internally by AMD. We often talk about customer AI, but we also prioritize AI because it can make our company better. For example, making better and faster chips, we hope to integrate AI into the development process, as well as marketing, sales, human resources and all other fields. AI will be ubiquitous. Q: NVIDIA has explicitly stated to investors that it plans to shorten the development cycle to once a year, and now AMD also plans to do so. How and why do you do this? A: This is what we see in the market. AI is our company's top priority. We fully utilize the development capabilities of the entire company and increase investment. There are new changes every year, as the market needs updated products and more features. The product portfolio can solve various workloads. Not all customers will use all products, but there will be a new trend every year, and it will be the most competitive. This involves investment, ensuring that hardware/software systems are part of it, and we are committed to making it (AI) our biggest strategic opportunity. Q: The number of TOPs in PC World - Strix Point (Ryzen AI 300) has increased significantly. TOPs cost money. How do you compare TOPs to CPU/GPU? A: Nothing is free! Especially in designs where power and cost are limited. What we see is that AI will be ubiquitous. Currently, CoPilot+ PC and Strix have more than 50 TOPs and will start at the top of the stack. But it (AI) will run through our entire product stack. At the high-end, we will expand TOPs because we believe that the more local TOPs, the stronger the AIPC function, and putting it on the chip will increase its value and help unload part of the computing from the cloud. Q: Last week, you said that AMD will produce 3nm chips using GAA. Samsung foundry is the only one that produces 3nm GAA. Will AMD choose Samsung foundry for this? A: Refer to last week's keynote address at imec. What we talked about is that AMD will always use the most advanced technology. We will use 3nm. We will use 2nm. We did not mention the supplier of 3nm or GAA. Our cooperation with TSMC is currently very strong-we talked about the 3nm products we are currently developing. Q: Regarding sustainability issues. AI means more power consumption. As a chip supplier, is it possible to optimize the power consumption of devices that use AI? A: For everything we do, especially for AI, energy efficiency is as important as performance. We are studying how to improve energy efficiency in every generation of products in the future-we have said that we will improve energy efficiency by 30 times between 2020 and 2025, and we are expected to exceed this goal. Our current goal is to increase energy efficiency by 100 times in the next 4-5 years. So yes, we can focus on energy efficiency, and we must focus on energy efficiency because it will become a limiting factor for future computing. Q: We had CPUs before, then GPUs, now we have NPUs. First, how do you see the scalability of NPUs? Second, what is the next big chip? Neuromorphic chip? A: You need the right engine for each workload. CPUs are very suitable for traditional workloads. GPUs are very suitable for gaming and graphics tasks. NPUs help achieve AI-specific acceleration. As we move forward and research specific new acceleration technologies, we will see some of these technologies evolve-but ultimately it is driven by applications. Q: You initially broke Intel's status quo by increasing the number of cores. But the number of cores of your generations of products (in the consumer aspect) has reached its peak. Is this enough for consumers and the gaming market? Or should we expect an increase in the number of cores in the future? A: I think our strategy is to continuously improve performance. Especially for games, game software developers do not always use all cores. We have no reason not to adopt more than 16 cores. The key is that our development speed allows software developers to and can actually utilize these cores. Q: Regarding desktops, do you think more efficient NPU accelerators are needed? A: We see that NPUs have an impact on desktops. We have been evaluating product segments that can use this function. You will see desktop products with NPUs in the future to expand our product portfolio.

Yole predicts in its latest report that, driven by generative ai, the GPU market size is expected to reach $190 billion by 2029, twice as large as the CPU market size!

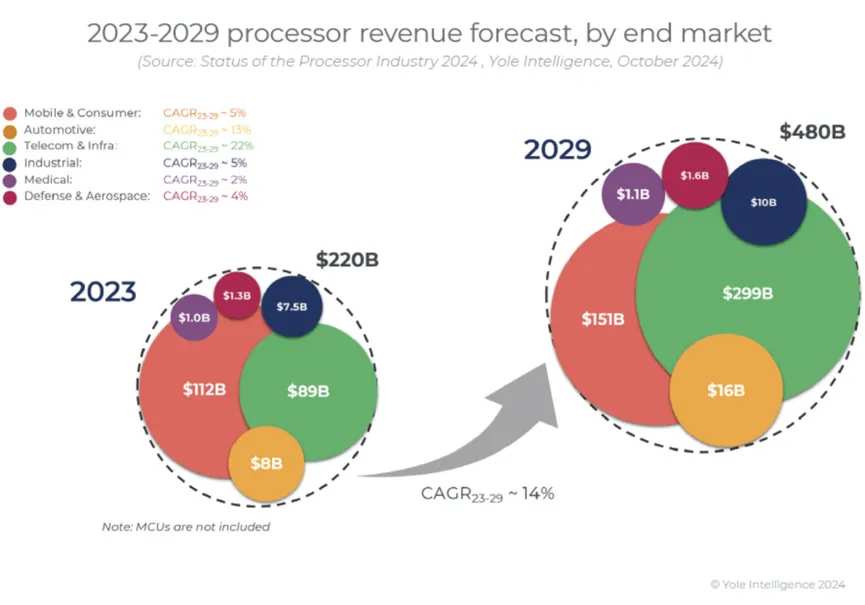

They stated that the processor market will experience significant growth, mainly driven by the increasing demand for generative AI applications. By 2029, the market size is estimated to reach $480 billion, with GPUs and AI ASICs leading this expansion. Although APUs, CPUs, and GPUs are currently leading the market in that order, GPUs are expected to surpass other segmented markets as they play a crucial role in AI-driven workloads. Data center AI ASICs are also expected to grow rapidly as specialized chips for AI tasks gain attention, especially with the development of custom processors by cloud hyperscalers.

It is expected that by 2024, the telecommunications and infrastructure industry will surpass the mobile and consumer industries to become the leading segmented market, thanks to significant investments in artificial intelligence infrastructure. Meanwhile, the automotive industry is emerging as a major growth area, benefiting from its shift towards artificial intelligence and advanced processing technologies. In contrast, demand for smartphones and personal computers is expected to remain soft over the next five years, leading to moderate growth in the mobile and consumer industries, with a projected compound annual growth rate of around 5%.

It is expected that by 2024, the telecommunications and infrastructure industry will surpass the mobile and consumer industries to become the leading segmented market, thanks to significant investments in artificial intelligence infrastructure. Meanwhile, the automotive industry is emerging as a major growth area, benefiting from its shift towards artificial intelligence and advanced processing technologies. In contrast, demand for smartphones and personal computers is expected to remain soft over the next five years, leading to moderate growth in the mobile and consumer industries, with a projected compound annual growth rate of around 5%.

Nvidia dominates the GPU market, while Intel faces competition in the CPU market.

With the continuous growth in demand for AI accelerators, $NVIDIA (NVDA.US)$ they will lead the generative AI revolution with their high-performance GPUs.

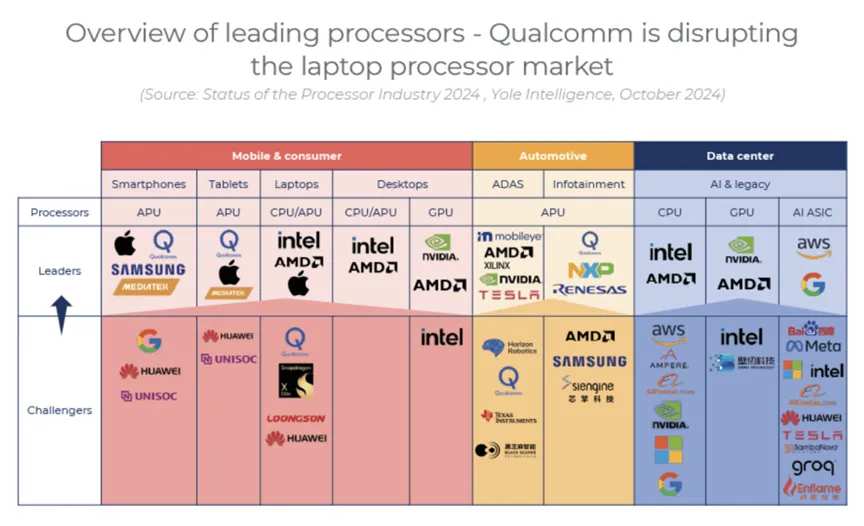

报告显示,处理器市场主要由CPU和GPU组成,其中英特尔和 AMD 在 CPU 领域领先,Nvidia 则近乎独霸 GPU ,他们合计占据各自市场的 97%,并占据整个处理器市场的 47%。

$Intel (INTC.US)$ 仍然是 CPU 领域的领导者,但由于来自 Ampere Computing 等初创公司以及$Amazon (AMZN.US)$和谷歌等科技巨头的竞争日益激烈,其市场份额正在下降。与此同时,$Qualcomm (QCOM.US)$和联发科在 APU 领域占据主导地位,而苹果在内部设计方面处于领先地位。在笔记本电脑市场,他们与曾经的双头垄断企业英特尔/AMD 的竞争越来越激烈。汽车市场的竞争也日益激烈,众多公司都在争夺不断扩大的机会。

$Advanced Micro Devices (AMD.US)$ Intel is leading in the FPGA field, especially in the SoC FPGA field, while AI ASIC is mainly driven by Google, Amazon, and other datacenter OEMs as well as Intel's Gaudi product line.$Alibaba (BABA.US)$The DPU market is also dominated by leading datacenter processors and hyperscale cloud providers.

In China, the government's prioritization of artificial intelligence and RISC-V has created a competitive environment for processors. Overall, the artificial intelligence processor market is rapidly growing, indicating that the industry is in a transformative stage.

Generative AI is driving processor innovation.

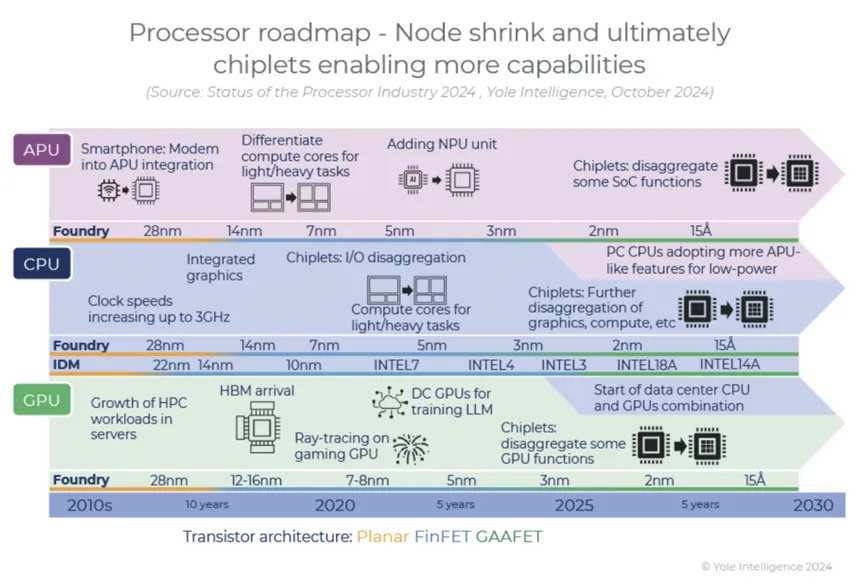

Since 2023, generative artificial intelligence has driven innovation in processors, optimizing artificial intelligence in data centers and consumer devices. AI personal computers are reshaping the laptop and desktop market, with Apple M and Qualcomm's Snapdragon X-Elite/Plus leading the trend. AMD and Intel have also entered the artificial intelligence personal computer field with 4nm and 3nm processors, respectively.

In smart phones, integrated artificial intelligence has improved performance, particularly with MediaTek's Dimensity 9300+. Nvidia's Blackwell GPU chip architecture will enhance data center capabilities, while Arm-based CPUs (such as Nvidia Grace) and custom processors from major tech companies are gaining attention in the server space. The automotive industry is also evolving due to the demand for ADAS technology.

Startups and hyperscale enterprises are focusing on AI ASIC inference to compete with Nvidia, leveraging small chips and HBM memory for increased efficiency. The 4nm process is becoming a standard, while 3nm is limited to specific applications. Today,$Taiwan Semiconductor (TSM.US)$Leading in advanced lithography, while Samsung faces challenges in terms of production capacity. The small chip architecture is widely adopted throughout the industry, allowing for optimizations for various applications.

After a decline in revenue, Intel is adjusting its global strategy to enhance the competitiveness of its foundry business, planning to utilize TSMC's 3nm process to produce its Lunar Lake processors. By 2026, Intel's focus will shift to internally manufacturing the Panther Lake processors.

Advanced packaging, rapid development.

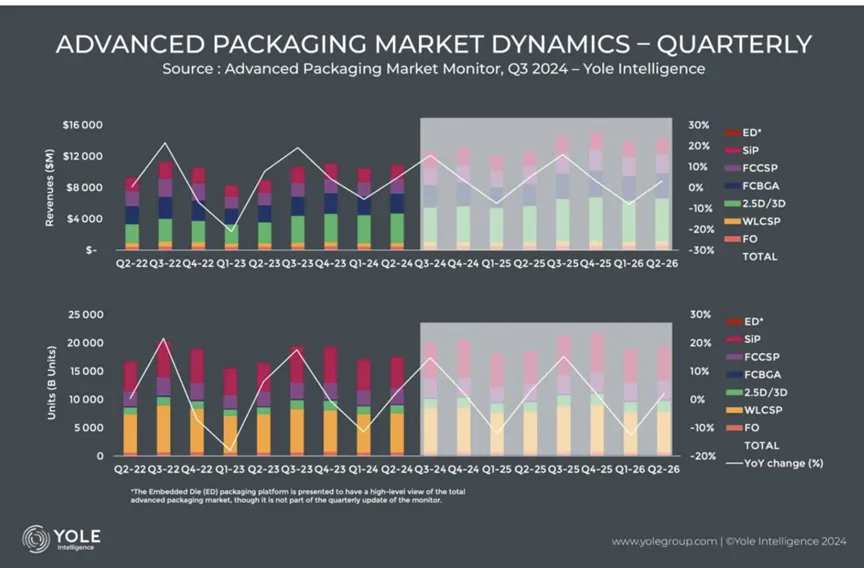

Yole reported that under the drive of artificial intelligence, the revenue for advanced packaging in the second quarter of 2024 reached $10.9 billion, a 5% increase from the previous quarter.

The report indicates that due to normal seasonal factors typically affecting backend operations, the first half of the year will likely be the weaker period. As signs of slow demand recovery emerge, revenue is expected to grow by another 15.5% to $12.6 billion in the third quarter of 2024. Despite ongoing soft demand and further customer inventory digestion, 2024 is expected to be a year of recovery, with stronger performance in the second half.

In terms of capital expenditure, the second quarter of 2024 slightly exceeded the previous quarter. Top players had advanced packaging capital expenditures of about $10.3 billion in 2023, a 19% decrease from the previous year, but an estimated 7% increase is projected in 2024. Monitoring included new analyses of two different scenarios for FOPLP adoption. The most optimistic scenario reflects a higher shift towards UHD FO to PLP conversion, considering that TSMC will significantly transfer a large part of its CoWoS and InFO production to panels starting from 2027.

Yole also predicts that in the coming years, advanced packaging revenue is expected to grow at a compound annual rate of 12.7%, meaning the overall market size will increase from $39 billion in 2023 to $80 billion in 2029. Overall, 2023 was a relatively weak year for the entire semiconductor industry and the advanced packaging market was also affected. Nevertheless, with increasing demand and the continuous growth of advanced packaging adoption, the market will rebound in 2024.

According to Yole, the advanced packaging market is mainly driven by the mobile and consumer, telecommunications and infrastructure, as well as automotive markets, propelled by trends such as HPC and generative AI. Among all packaging platforms, 2.5D/3D packaging will experience the fastest growth in the next five years. Industry giants such as Taiwan Semiconductor, Intel, Samsung, as well as top OSATs like ASE, Amkor, and JCET are heavily investing in advanced packaging technology and capacity, with an expected investment of approximately $10.7 billion in their advanced packaging business by 2024.

AI chips, the influence is spreading.

As the primary driving force in the chip industry, the impact of AI chips is spreading. For example, ASML CEO Christophe Fouquet, the helmsman of the lithography giant, stated last week during the financial report release, "Without AI, the semiconductor industry would be in dire straits."

From the financial reports of ASML and Taiwan Semiconductor and the resulting impact, we can see AI is deeply influencing the semiconductor industry.

As Bloomberg recently reported, the semiconductor industry is often seen as a barometer of the global economy because chips are crucial for a wide range of products from data center servers to dishwashers. Companies providing the equipment to manufacture these chips are at the forefront of this industry.

Before semiconductor companies begin production, it takes several months to build, install, and test the machines used to manufacture chips. Therefore, companies like ASML have an unusually long-term view of customer sentiments. Currently, they are sending warning signals across all areas except artificial intelligence. For instance, due to increased customer inventory, demand from automotive and industrial suppliers is declining.

In addition, Intel is cutting costs and delaying construction of new factories to address declining sales and increasing losses. Samsung Electronics apologized to investors this month, citing disappointing financial performance due to delays in high-bandwidth memory chips. Investors will be watching closely this week.$Texas Instruments (TXN.US)$The company, which will announce its performance on Tuesday, is widely used by customers for its simulation chips.

Overall, the outlook for equipment manufacturers seems challenging, with many companies' stock prices hitting historic highs earlier this year. Some traders have not waited to see and have started selling stocks.

ASML just went through its worst week since early September, with its U.S.-listed stock price dropping by 14%. The largest chip equipment manufacturer in the usa$Applied Materials (AMAT.US)$Applied Materials Inc. fell by 9.1%, while KLAn and $Lam Research (LRCX.US)$ fell by more than 12%.

At the same time, stocks of Israeli chip companies fell on the Tel Aviv Stock Exchange, mirroring their decline on the U.S. Stock Exchange. Leading the decline is NOVA, dropping by about 14.8%, with a market cap of approximately 0.96 billion dollars evaporating, currently valued at around 5.4 billion dollars. Tower dropped 3.6%, reducing its market cap to 5.15 billion dollars.$Camtek (CAMT.US)$ Fell by 3.5%, with a market cap of approximately 3.82 billion US dollars.

Cantor Fitzgerald analyst CJ Muse wrote in a research report: "We have always been cautious about other semiconductor equipment companies. But we originally thought that companies like ASML with longer delivery times would perform well. Obviously, our assumption was wrong."

AI chips are expensive, not many players will be involved.

Recently, Marvell's Executive Vice President and Chief Technology Officer Noam Mizrahi said in an interview with Nikkei that due to the substantial funds required to remain competitive, only a few top chip developers can continue to invest in semiconductors for AI computing.

"However, even with 'not many' participants able to stay in this game, the market for custom AI chips will grow rapidly." Noam Mizrahi emphasized.

Mizrahi pointed out: "From an investment perspective, this is indeed a vast market. It is a race for those with scale and ability to make long-term investments." "You need to invest in packaging technology, you need to invest in 5-nanometer, 3-nanometer, 2-nanometer chip process technology. You need to invest in everything, including intellectual property, interface technology, and memory technology. ... That's why I believe this field won't be too crowded."

According to the International Business Strategies (IBS) estimation, the cost of manufacturing a single wafer of 7-nanometer chips is close to $10,000, the cost of manufacturing a single wafer of 5-nanometer chips exceeds $14,000, and the cost of manufacturing a single wafer of 2-nanometer chips is close to $20,000. To maintain competitiveness, chip developers spend hundreds of millions of dollars developing and designing each generation of chips to stay relevant.

At the same time, the demand for custom chips is growing, especially for chips used for ai computing.

While Nvidia and AMD's ready-made products remain very popular, leading cloud service providers such as Google, amazon, and Meta are investing heavily in developing their own datacenter semiconductors.$Microsoft (MSFT.US)$The goals of these tech giants are to optimize performance fully and achieve product differentiation. This not only requires establishing their own chip design teams, but also finding partners to support chip development and production.

Marvell forecasts that the compound annual growth rate of the total market volume for custom computing chips will reach 45% from 2023 to 2028, increasing from $6.6 billion to $42.9 billion. The company's goal is to increase its market share in this growing field.

Mizrahi stated that another major driver of the ai boom is the 'interconnection' function in data centers. For example, supercomputers designed for ai computing require fast connections between multiple graphics processing units or ai accelerators to run as a computing unit, optimizing their performance.

"We're not talking about a single [component]," Mizrahi said. "We're talking about hundreds, thousands, tens of thousands of components. They are all interconnected... They all need to appear as a virtual machine. The way they are connected has a huge impact on [computing] results."

According to Marvell, the interconnect market is expected to grow at a compound annual rate of 27% from 2023 to 2028, reaching a value of nearly $14 billion.

In conclusion,

Actually, not long ago, the big brother in the chip industry was Intel, while Nvidia has been developing well, it still cannot be compared with the big brother. Especially after experiencing the collapse of the mining frenzy, everyone had expressed concerns about Nvidia's future. But with the arrival of ChatGPT, everything has changed.

From the market perspective, currently Nvidia is the most stable winner in the AI market. Although Taiwan Semiconductor, AMD, and SK Hynix are also benefiting significantly, considering the relevant monopolistic situation, they will also face uncertainties.

How AI will impact the semiconductor industry in the future remains to be seen.

Editor/Rocky