Trump's preferred bullish assets include gold, with short positions in US stocks and the US dollar, and long positions in A shares.

Elevenfinance APP learned that Guosen Securities released a research report, stating that Harris' trading leans towards bullish assets such as gold, crude oil, copper, and the US dollar; bearish varieties include stocks (including A shares and US stocks), and the impact on US treasury bonds is more short than long; Trump's trading mechanism is more complex, with a preference for bullish assets like gold, short positions in US stocks and the US dollar, and long positions in A shares, while crude oil, US treasuries, copper, and other assets have varying degrees of bearishness.

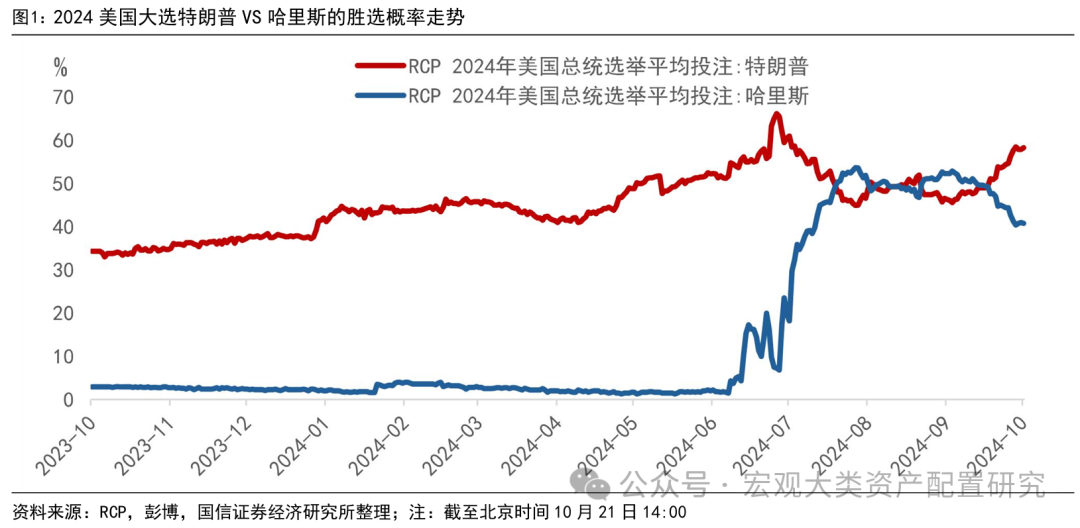

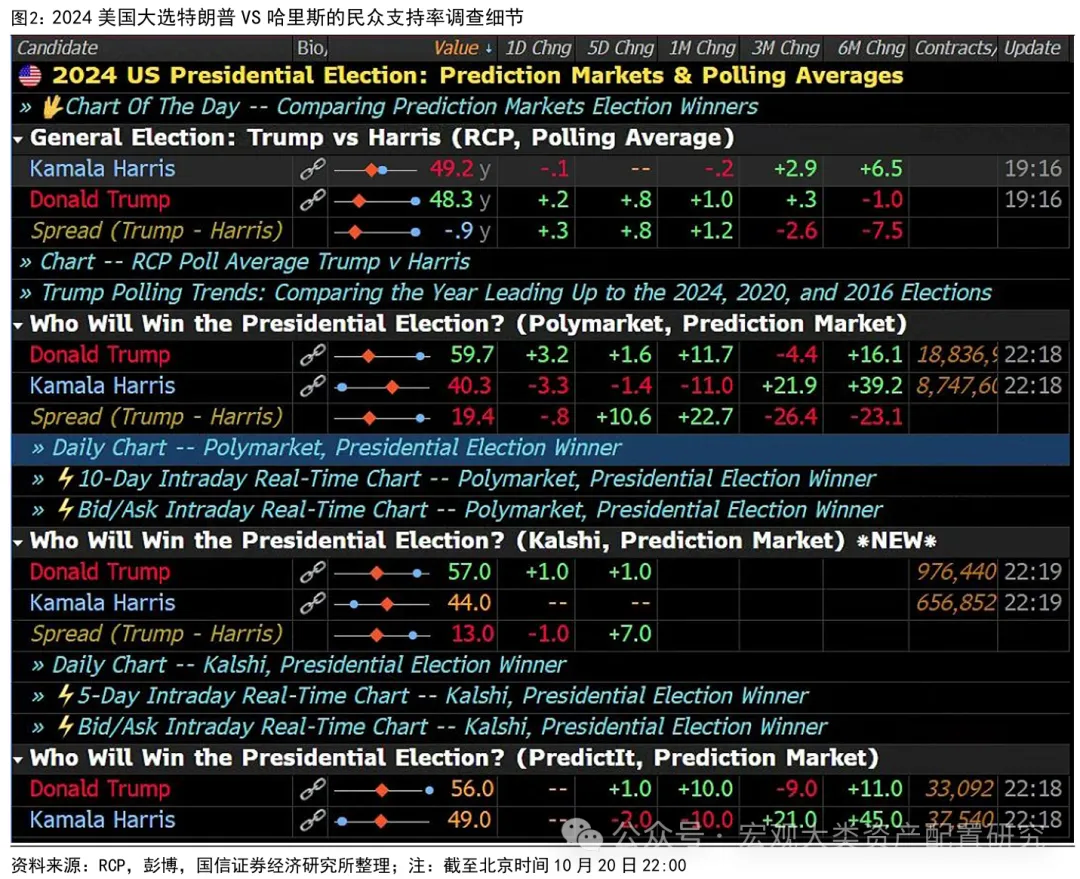

Regarding the 2024 US presidential election average betting odds observed by Real Clear Politics, recent feedback shows that Trump has surpassed Harris and continues to widen the gap. As of October 21, 2024, Trump's average betting feedback victory probability is approximately 58.3%, significantly exceeding Harris' 40.8%. The 'Trump Portfolio' represented by assets such as Trump Media & Technology has significantly outperformed US stocks recently, matching the timing of Trump's rising election odds.

Trump's odds of winning the election surpassing Harris: Global risk appetite rebalancing

Trump's odds of winning the election surpassing Harris: Global risk appetite rebalancing

Based on Real Clear Politics' observation of the average betting odds for the 2024 US presidential election, Trump has recently surpassed Harris and continues to widen the gap. As of October 21, 2024, Trump's average betting feedback victory probability is approximately 58.3%, significantly exceeding Harris' 40.8%. Risk aversion trades along the export chain and offshore chain, the global risk sentiment rebalancing feedback are seen within trading signals. This article explores different scenarios after the US election settles, especially if Trump starts his second term in the White House, predicting the trends of various assets and industries globally and initiating a new round of left-hand side layout and risk prevention.

The impact of Trump's potential second presidential term on the world if he is elected as the president again

According to the PIIE's calculations, if Trump is re-elected as the President of the United States for a second term, it will have long-lasting and far-reaching effects on the economic growth and inflation levels of different countries. The impact of Trump's current policy thinking mainly focuses on trade, immigration, and the independence of the Federal Reserve. Although Trump's policies aim to reduce dependence on foreign production, they may also weaken the ability of American companies to export to global economic growth. In the long run, Trump's policies may lead to Americans bearing the greatest economic costs, rather than 'making foreigners pay.' Therefore, for assets denominated in US dollars such as US stocks and the US dollar, there is no long-term advantage.

Looking at the asset allocation orientation from the perspective of Trump's policy context

There is a wide range of disagreements in the domestic US market regarding Trump's economic stimulus and fiscal policies, with consolidated views more focused on harder immigration policies, more extreme trade policies, and potentially affecting the independence of the Federal Reserve's monetary policy.

Immigration Policy: Trump plans to restrict legal and illegal immigration again and subject visa applicants to 'extreme vetting.' Trump's policy may result in a decrease in labor supply, impacting economic growth and competitiveness. Strict immigration policies reduce the potential labor supply in the US economy, which could lead to labor shortages, especially in the low-skilled labor market. Rising labor costs may drive inflation, affecting consumer purchasing power and corporate profitability, leading to GDP and employment being lower than under other circumstances by 2040. It also causes a decrease in investment returns across various sectors of the US economy, with financial capital flowing overseas, where returns on capital are higher than in the US. The durable manufacturing sector experiences the greatest impact on output and employment, while agriculture and mining suffer from decreased competitiveness due to rising labor costs.

Trade Policy: Trump's proposed trade policies include a universal increase of 10 percentage points in tariffs (and imposing a 60 percentage point tariff on Chinese imports). This extreme trade policy is expected to cause a short-term decrease in US GDP, with relatively minor long-term effects. Tariffs lead to an initial decline in employment, especially in agriculture, mining, and durable manufacturing. In the long term, some unemployed workers are absorbed into the service industry, but overall employment rates still decline. Intermediate product prices rise, triggering inflation. Imports decrease, but the appreciation of the US dollar also reduces export competitiveness, with no significant improvement in trade balance. In the long term, the trade deficit may worsen due to capital outflows. Agriculture, mining, and durable manufacturing are most affected, with significant decreases in output and employment.

Independence of the Federal Reserve: Trump may attempt to weaken the political independence of the Federal Reserve by granting the President more control over monetary policy to stimulate economic growth. Initially, the actual US GDP may temporarily increase due to loose monetary policy, leading to employment rate growth, but inflation will intensify, and the long-term trend of GDP will start declining. At the same time, capital will flow out of the US to other countries like China, Canada, Germany, Japan, and Mexico. Changes in the Federal Reserve's monetary policy may also have significant global financial market impacts, triggering capital flows and exchange rate fluctuations.

Recently, the market's impression of Trump's Trade 2.0 is mostly based on extrapolating and adjusting his 'playing strategy' during the previous election period, especially during the trade friction time. By looking at the election platforms and policy goals of the Democratic and Republican parties (fiscal, monetary, trade), one can have a clearer view of the impact on various types of assets in different time periods in the future. In summary, Trump's Maganomics emphasizes higher immigration restrictions, higher import tariffs, taking an approach of internal tax reductions and external tax increases, with a preference towards traditional energy that would expand corresponding production capacity and affect its price foundation. While Harris also tries to boost the economy, her approach focuses more on the transition between old and new energy, increasing taxes, and relying on deficits to concentrate efforts to stimulate the economy. Overall, Harris's trade leans towards assets with bullish sentiment such as gold, crude oil, copper, and the US dollar; bearish sentiments are seen in stocks (including A-shares and US stocks), with short positions dominating the US bonds' impact in the short term and long positions in the long term. The Trump trade mechanism is more complex, leaning towards bullish asset categories in gold. Short positions prevail in the US stocks and US dollar market, while short positions dominate in the A-share market. Different levels of bearish sentiment are observed in crude oil, US bonds, copper, and other assets.

It is worth noting that the impact of Trump's potential victory on global asset prices is not singular and linear, especially when it comes to the indirect effects on various industries and styles of A-shares. The transmission pathways in the table below only show the directional impact on various types of assets based on the public policy agendas that the two have committed to. It does not directly indicate the rise or fall of these assets, especially for assets priced outside the US jurisdiction, which rely more on local macroeconomic policy adjustments, corporate profit differentials, and other influences.

Based on the latest disclosed holding positions data of Trump, the eight representative stocks he holds are: Trump Media Technology Group, Apple, Microsoft, Nvidia, Amazon, Alphabet, Berkshire Hathaway, Broadcom. These are considered as Trump's portfolio, and its performance since 2024 has been closely aligned with Trump's reelection prospects. The recent surge of the 'Trump portfolio' is closely tied to the increase in Trump's reelection odds.