日前,华尔街知名投行高盛的策略师表示,标准普尔500指数未来十年的年化名义回报率预计仅为3%。相比之下,过去10年的年化名义回报率高达13%,而长期平均水平为11%。标准普尔500指数回报率将有大约72%的概率落后于美国国债。

日前,华尔街知名投行高盛的策略师表示,标准普尔500指数未来十年的年化名义回报率预计仅为3%。相比之下,过去10年的年化名义回报率高达13%,而长期平均水平为11%。标准普尔500指数回报率将有大约72%的概率落后于美国国债。Source: Brokerage China Author: Qu Hongyan Recently, China Yangtze Power hit a historical high and once again showed the slow bull stock trend of "tripling in ten years". The slow bull market has left behind many passers-by and brought good returns to the steadfast investors. It is "rare for those who triple in one year to be like carp jumping over the dragon gate, while those who double in three years are few and far between." On the other end of the investment world, however, violent collapses are also deafening, with many financial products suspected of "Ponzi schemes" ceasing payments, leaving investors with no hope of recovering their investments. Both positive and negative cases illustrate the importance of forming a suitable mentality towards money in one's lifetime; otherwise, sooner or later, you will divorce yourself from your money. "I call this the money mind, a person's IQ can reach 120, 140, or even higher levels, and perhaps some people's minds are good at doing one thing, while others are good at doing another. They can do things that most ordinary people can't do. But I know some very smart people who make very foolish decisions because they lack the money mind." Buffett once said so. The so-called money mind refers to believing in common sense, believing in compound interest, being cautious and rational, thinking independently, prioritizing security over return, not dealing with people with questionable character, not easily guaranteeing for others, not believing in windfall profits, and not trying to cross legal norms for extra benefits. In today's world of ubiquitous information, everyone's wealth may become the "prey" of those with ulterior motives. Only with the money mind, can one form good behavior habits and shield oneself from separating from one's wealth. Do not entrust your wealth easily. Wealth is easy to lose but hard to accumulate, and trust is a vital reason leading to the rapid loss of wealth. "Do not allow anyone else to manage your business unless you can watch their every move closely and understand their behavior; or you have strong reasons to believe in their character and ability. For investors, this criterion determines when you can let someone else make investment decisions for you." Graham's criterion written eighty years ago is so clear. Almost all the investors who lost their wealth in the financial products have violated the above two criteria. They did not have the ability to closely supervise the whereabouts of their funds, nor did they have sufficient reasons to believe in the character of the product issuers. They easily invested their own wealth solely based on others' glib tongue and a piece of commitment paper. They did not act as gatekeepers of their own wealth and ended up with nothing left even if the government punished the wrongdoers. "An ounce of prevention is worth a pound of cure." This is a phrase Munger often says. Destiny must be in one's own hands, and investors with a suitable money mind will try their best to find suspicious points in their investments to protect the safety of their principal. For example, whether the manager is trustworthy, whether the underlying assets are profitable, whether oneself can timely monitor the risks in the investment process, and whether the sales staff is obtaining large commissions. As long as any unreliable signs are found, these investors firmly will not invest their money. Do not desire to get rich quick. As in the capital market and anywhere else, making money is not easy, and desiring to get rich quick will lead to quick loss of wealth. In the capital market, the desire to get rich quickly often leads to investors over-allocating specific stocks, industries, or assets at the worst time. For example, buying high-risk stocks that can gain huge returns once an adventure succeeds, but the chance of success is very small, also known as "whispering stocks" by legendary fund manager Peter Lynch. "They often tell investors a story with explosive effects. These 'whispering stocks' have a hypnotic effect on people, and it is easy for you to believe that the story the company tells has an emotional appeal that can easily confuse you." This is like hearing a very tempting "sizzling" sound, making you salivate, but you did not notice that there is no steak on the grill. In the eyes of investors who lack the money mind, stable yield provided by blue chips such as China Yangtze Power cannot meet their demands. However, historical experience clearly shows that buying stocks lacking in safety solely based on imagined high yields is unwise. The long-term average investment return of general stocks is 9%-10%, which is also the average investment return of stock indexes in history, a benchmark to measure one's investment performance and the benchmark to measure fund investment performance.

Author: Chen Ming.

Is the era of the sharp rise in the US stock market over?

Recently, Goldman Sachs, a well-known investment bank on Wall Street, stated that the S&P 500 index is expected to have a nominal annualized return of only 3% in the next ten years. In comparison, the nominal annualized return over the past 10 years was as high as 13%, while the long-term average level is 11%. There is about a 72% probability that the S&P 500 index return will lag behind US Treasury bonds.

At the same time, David Rosenberg, the president of Rosenberg Research, a top American economist, also issued a warning that the US stock market may collapse. He said, "These days observing the market is like watching a clown blowing up a balloon, knowing full well that a crash is inevitable. When this super bubble bursts, it will be spectacular."

At the same time, David Rosenberg, the president of Rosenberg Research, a top American economist, also issued a warning that the US stock market may collapse. He said, "These days observing the market is like watching a clown blowing up a balloon, knowing full well that a crash is inevitable. When this super bubble bursts, it will be spectacular."

JPMorgan strategists cited the bank's own indicators, stating that due to investors betting on a rise in the U.S. dollar on the eve of the U.S. election, there was a significant surge in dollar demand last week, and this buying interest may continue.

Is the era of the sharp rise in the US stock market over?

Since the beginning of this year, the U.S. stock market has continued to strengthen, with the Nasdaq rising by over 23% and the S&P 500 index also approaching a 23% increase. However, this rebound is mainly concentrated on a few large technology stocks.

Goldman Sachs strategists say that as investors turn to other assets, including bonds, seeking better returns, it is unlikely for US stocks to maintain their performance above average levels of the past decade. David Kostin and other Goldman Sachs strategists analyze and predict.$S&P 500 Index (.SPX.US)$The annualized nominal return rate for the next ten years is expected to be only 3%, a significant decrease compared to recent performance. Over the past decade, the annualized nominal return rate of the S&P 500 index has been 13%, with a long-term average of 11%.

Goldman Sachs strategists also believe that the benchmark index return rate will have about a 72% chance of lagging behind US Treasury bonds, with a 33% chance of lagging behind inflation by the end of 2034. In their latest report, Goldman Sachs strategists write: "Investors should be prepared as stock returns over the next 10 years will be close to the lower end of their typical performance range."

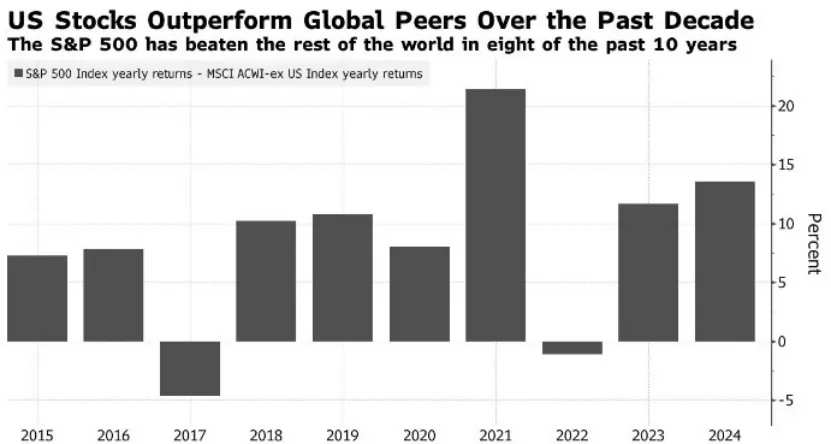

After the global financial crisis, the US stock market rebounded, first driven by near-zero interest rates, and later by bets on economic growth resilience. According to compiled data, in 8 out of the past 10 years, the performance of the S&P 500 index is expected to outperform other regions globally. However, this year's 23% increase in the index is mainly concentrated in a few of the largest technology stocks. Goldman Sachs strategists state that over the next ten years, equally weighted indices like the S&P 500 are likely to outperform market cap-weighted benchmarks, indicating a potential shift in market dynamics.

For investors accustomed to strong returns in recent years, this forecast from Goldman Sachs may serve as a reminder of the cyclical nature of financial markets. It suggests the need for diversification and a reassessment of investment strategies to achieve long-term financial goals.

Surveys show that investors anticipate the continuation of the US stock market rebound until the final stage of 2024. People believe that the strength of US corporate performance is more critical to stock market performance compared to who wins the US presidential election or the policies of the Federal Reserve.

With the continuous surge in the US stock market, many Wall Street elites have been warning about the possibility of a bubble in the stock market. Some experts suggest that investors concerned about this situation should focus on "key sectors" and add some stocks with "insurance-like" qualities to their portfolios.

American economist and President of Rosenburg Research, David Rosenberg, recently stated, "Observing the market these days is like watching a clown blow up a balloon, knowing that the inevitable result (a massive crash) is unavoidable. When this super bubble bursts, it will be spectacular."

David Rosenberg pointed out that investors need to act cautiously, avoiding herd mentality, especially when it comes to the frenzy around large technology stocks. In his view, investors should focus on stocks with strong business models, robust growth, reasonable prices, and should add some 'insurance' to their investment portfolios. David Rosenberg suggested that investors should allocate their investments towards products that people will always need in the future. He specifically recommended paying attention to medical care and essential consumer goods stocks.

David Rosenberg also mentioned that utility stocks appear promising. Other forecasters have warned that due to the increasing demand for electrical utilities and datacenters fueled by the AI boom, utility companies could face significant upside potential. David Rosenberg stated, "As we have long said, utility stocks are close to being 'no-brainers' because of their income properties, and the strong and long-term prospects of the US electricity demand enhance profit visibility, thus leading the reevaluation of utility stocks as 'defensive growth.'" Additionally, David Rosenberg pointed out that considering the escalating global geopolitical tensions, aerospace & defense stocks might also be worth buying.

David Rosenberg also specifically recommended that investors should consider adding 'insurance' to their investment portfolios, referring to gold and government bonds. He wrote, "The beauty of gold is that it is not a debt that a central bank can easily dismiss, nor a currency that can be easily printed by a government. I am also bullish on the US Treasury market because its yields are among the highest in all major industrialized nations, and it has strong liquidity."

JPMorgan: Recent Surge in US Dollar Demand

Recently, JPMorgan strategists cited their own indicators, stating that due to investors betting on a rise in the US dollar ahead of the US elections, demand for the US dollar surged last week, and this buying pressure may continue.

JPMorgan pointed out that the most popular trades were buying the US dollar in the options market while simultaneously selling the Singapore dollar and Australian dollar. Patrick Locke and other JPMorgan strategists mentioned strong demand for buying the US dollar against the Mexican peso and the US dollar against the euro.

After experiencing the worst quarter performance of the US dollar trade-weighted index since the end of last year, a significant amount of buying pressure has shifted US dollar positions from short to neutral. Strategists stated that this provides ample room for traders to increase long positions before the election. 'Election trading activity is picking up,' strategists wrote, 'Despite investors buying the US dollar in October so far, overall, the US dollar positioning remains predominantly neutral. There is still more room for additional election hedging trades in the next two weeks.'

According to the data from the U.S. Commodity Futures Trading Commission, speculators have almost completely offset the net short positions in the U.S. dollar established in July. France's Industrial Bank Chief Forex Strategist Kit Juckes said on Monday, "Before the U.S. election, old positions are being liquidated."

JPMorgan also pointed out that the selling of the euro has intensified, with some put options targeting the euro falling to par with the U.S. dollar. As U.S. presidential candidate Trump threatens to expand tariffs to Europe, the risk of the euro falling to parity with the U.S. dollar is increasing. JPMorgan strategists said, "We believe that the euro/dollar short positions will continue to increase."

A recent research report released by JPMorgan also stated that hedge fund capital is showing a strong preference for Republican themes, with Republican winners being bought into over the past few weeks, holding positions close to a 2-year high, while Democratic winners are being sold, with positions at multi-year lows.

According to observations on the average betting rates for the 2024 U.S. presidential election by RCP (Real Clear Politics), Trump has been surpassing Harris recently and widening the gap. As of October 21, 2024, the average betting feedback on Trump's victory probability is approximately 58.3%, significantly exceeding Harris' 40.8%. Risk-averse transactions in the export chain and outbound chain, along with a rebalancing feedback on global risk sentiment, are reflected in trading signals.

Guosen Securities pointed out that Trump's current policy direction primarily focuses on trade, immigration, and Fed independence. While Trump's policies aim to reduce dependence on foreign production, they may also weaken the ability of U.S. companies to export to world economic growth. In the long run, Trump's policies may lead Americans to bear the greatest economic costs rather than 'making foreigners pay.' Therefore, in the long term, there is no advantage for U.S.-based assets such as U.S. stocks and the U.S. dollar.

Editor/Rocky