他们还认为,标普500指数落后于国债的概率约为72%,并且到2034年落后于通胀的概率为33%。

他们还认为,标普500指数落后于国债的概率约为72%,并且到2034年落后于通胀的概率为33%。Goldman Sachs strategists expect the s&p 500 index to have an average annual nominal roi of only 3% over the next ten years, far below the 13% of the past decade.

Goldman Sachs strategists say that the US stock market is unlikely to sustain its above-average performance of the past decade, as investors are starting to shift towards other assets including bonds in search of better returns.

According to analysts including David Kostin, they expect the s&p 500 index to have an average nominal annual return of only 3% over the next ten years. In contrast, the average annual return of this index over the past decade has been 13%, with a long-term average return of 11%.

They also believe that the probability of the s&p 500 index underperforming bonds is about 72%, and the probability of underperforming inflation by 2034 is 33%.

They also believe that the probability of the s&p 500 index underperforming bonds is about 72%, and the probability of underperforming inflation by 2034 is 33%.

The team wrote in their report on October 18th, "Investors should be prepared for lower stock returns over the next ten years."

Since the global financial crisis, the US stock market has been on an upward trend. According to data compiled by Bloomberg, the s&p 500 index outperformed other regions in the world in eight out of the past ten years.

However, this year's 23% rebound is mainly concentrated in the largest technology stocks in the USA. Goldman Sachs strategists say they expect the rebound to be more widespread, and over the next ten years, the csi 500 equal weight index will outperform the market cap-weighted s&p 500 index.

Even if the rebound continues to be concentrated, the return rate of the s&p 500 index will be below average, at around 7%.

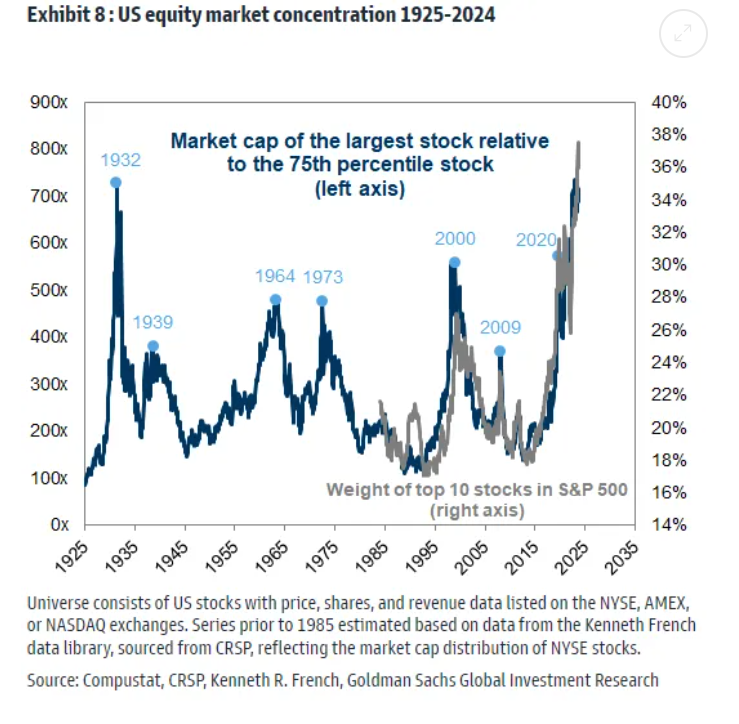

Undoubtedly, the concentration of the US stock market (and therefore the global stock market) is exceptionally high. However, investors should question whether this concentration is important or whether they should avoid stocks because of it. Kostin found that the concentration is at the 99th percentile in history.

Kostin said that compared to markets with lower concentration and higher diversification, the performance of indices in a highly concentrated environment will reflect a less diversified range of risks and may have a larger actual volatility.

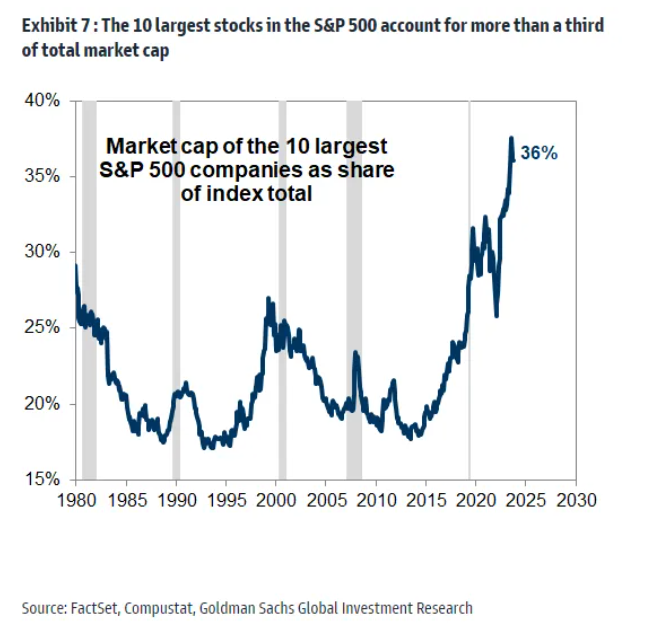

The following chart shows the proportion of the top 10 stocks in the S&P 500 index since 1980:

Another chart by Kostin reflects the proportion of the largest stock since 1925 to the companies in the index at the 75th percentile (larger than 74% of companies). The peaks in the chart coincide with important moments, whether it is buying (such as 1932 and 2009) or selling (such as 1973 and 2000). Extreme concentration occurs during economic downturns, which is not the case now, or when the market is extremely excited, such as the Nifty Fifty in 1973 and the internet bubble in 2000.

Kostin shows how concentration affects valuation. If the top 10 stocks are excluded, the return of the S&P 500 index exceeds that of the 10-year government bonds; while the returns of the top 10 stocks themselves are lower, which should be a strong sell signal.

Former chief market commentator of the Financial Times and Bloomberg columnist John Authers pointed out that viewing extreme concentration as a signal of increased fragility in the US stock market makes sense. Generally, a strategy of solely buying the largest stocks is a losing strategy because these stocks only have downside potential, and their competitive position will gradually be eroded.

Kostin points out that even without considering concentration, the return of US stocks in the next decade will only increase from the 7th percentile since 1930 to the 22nd percentile. This means that even if we ignore the impact of concentration, it is challenging to have a positive outlook on stocks in the next ten years.

However, it seems that the US stock market will continue to rise for now, so caution is advised.

Editor/rice