标普500指数不断超越策略师的预期

标普500指数不断超越策略师的预期Wall Street strategists believe that the valuation of the S&P 500 index is getting higher, which will further squeeze the upside potential.

The unexpected rise of US stocks this year has surprised Wall Street strategists.

The Zhixin Finance APP learned that the S&P 500 index hit a new high in the closing week last week, with a cumulative increase of 23% so far this year. In January, strategists predicted that the S&P 500 index would be flat this year. Despite repeated upward revisions in their expectations, the S&P 500 index's performance still exceeded expectations.

The S&P 500 index has continuously surpassed the expectations of strategists.

The S&P 500 index has continuously surpassed the expectations of strategists.

This is somewhat related to the US economy. The performance of the job market is much better than expected, while inflation seems to be under control. Interest rates are high but declining. The benefits of the artificial intelligence boom have not been fully priced in January. However, the uncertainties in US politics are well known, and reliable long-term indicators suggest extreme caution.

Wall Street strategists believe that the valuation of the S&P 500 index is becoming increasingly high, which will further squeeze the upside potential. Goldman Sachs' Chief US Equity Strategist, David Kostin, made a noteworthy dual prediction. On October 4, he raised the year-end forecast for the S&P 500 index from 5600 points to 6000 points, and set the 12-month target at 6300 points, implying an increase of about 11% in a year. Last week, he published a follow-up research report, suggesting that the S&P 500 index will only have a nominal annual increase of 3% (actual increase of 1%) over the next 10 years, making it one of the worst increases on record.

This is not completely contradictory. Bloomberg columnist John Authers stated that a market that is already strong is expected to perform well in the next 12 months, but poorly over the next 10 years, indeed indicating instability in the market, possibly leading to bubbles. Authers analyzed the driving factors of the market.

Emotions.

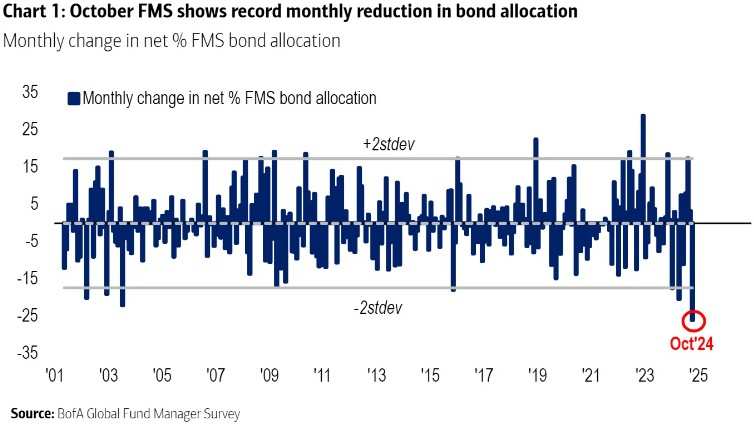

In the short term, the market is a product of what Keynes referred to as the 'animal spirits.' The situation is clearly developing in a bullish direction, which is difficult to stop in the short term. Last month, the largest global bond management companies surveyed by Bank of America cut their bond allocations by the largest amount in 23 years:

People's excitement about stocks is evident, with the largest increase in stock allocations since the first lockdown in 2020:

A strong stock market often generates positive feedback loops for the economy. With the rise of the S&P 500 index, optimism about the continued growth of the U.S. economy in the next 12 months has strengthened. All of this aligns with the market's growing belief that Donald Trump's return to the White House would be favorable for the stock market but unfavorable for bonds.

Another important short-term factor is earnings season, which also suggests that investors should not exit the stock market. Profit forecasts are relatively unchallenging, and Goldman Sachs' Kostin team estimates that profit margins can continue to expand. Goldman's expectations for the U.S. economy are slightly better than the market's general expectations, providing a reason for the strong performance of the stock market next year.

Valuation

In the long run, valuation is the most important factor. The higher the price when buying stocks, the less return one will get over ten years or longer. However, this relationship does not hold in the short term at all, and investors cannot use it to time the market. An irrationally expensive market will always become even more expensive. But over a period of ten years or longer, this relationship will hold. This is the core reason why Goldman Sachs and other institutions are quite pessimistic about long-term forecasts for the US stocks.

The most widely used long-term value measure indicator is CAPE (Cyclically Adjusted Price-to-Earnings ratio), which was first proposed by legendary value investor Benjamin Graham in the 1930s and popularized 25 years ago by Nobel Prize winner Robert Shiller in his book 'Irrational Exuberance'. The key to this indicator is that valuation will be adjusted based on the economic cycle, with multiples being higher when the economy is in a downturn but likely to improve, and vice versa.

US stock valuations seem to be at historical highs.

With the growth of profitability and productivity, CAPE will rise over time. However, it is concerning that the S&P index is more expensive than on the eve of the Great Crash of 1929, and not much cheaper than during the bursting of the dot-com bubble in the early 2000s. Perhaps more importantly, after reaching a peak in the past, CAPE will sharply decline within a few years. This time is different, as CAPE peaked during the prosperity period after the 2021 pandemic, but rebounded by the end of 2022. Whether coincidental or not, this rebound happens to coincide with the launch of ChatGPT. The AI frenzy seems to play a crucial role in maintaining market highs.

Stock valuations should not be disconnected from bonds. Lower bond yields prove that paying a higher price for stocks is reasonable. According to Shiller's 'Excess CAPE Yield,' the lower the excess yield of stocks, the worse their subsequent performance relative to bonds. The excess CAPE yield turning negative twice (meaning stocks are more expensive than bonds) lined up perfectly with the Great Crash and the dot-com bubble, which were the two best opportunities in history to exit the stock market.

The long-term outlook for the US stock market is not optimistic.

But strange things have happened. The actual return of stocks currently exceeds the expected level, the largest since the 19th century. The most reasonable explanation is the special monetary stimulus during the epidemic. However, the most important thing is that reliable indicators show that one should not expect stocks to outperform bonds, as the recent performance of stocks seems abnormally high. Artificial intelligence and stimulus plans have played a significant role in supporting the rise of the stock market, but there are reasons to expect their impact to gradually diminish.

Currently, the USA market seems much more expensive than other developed markets. However, this is not always the case: during the peak of the internet bubble, stock markets in several countries were more expensive than the USA, even though the epicenter of the trend (like artificial intelligence) is obviously the USA.

The US stock market is not always more expensive than other markets.

The above analysis is not suggesting that investors should sell US stocks now. However, over a 10-year period, the performance of US stocks will lag behind stocks of other countries and will not perform well compared to bonds. The significant influence of the 'Big Seven', including Apple (AAPL.US), Amazon (AMZN.US), Microsoft (MSFT.US), Nvidia (NVDA.US), Alphabet (GOOG.US, GOOGL.US), Meta (META.US), and Tesla (TSLA.US), may be a core reason.

Concentration

Undoubtedly, the US stock market (even the global stock market) is exceptionally concentrated. Kostin found that concentration is at the 99th percentile historically, which is crucial: when market concentration is high, the overall index performance largely depends on the outlook of a few stocks. In a highly concentrated market environment, index volatility may be greater.

This is the largest share of the top 10 stocks in the S&P 500 index since 1980:

Kostin pointed out that concentration affects valuation. Excluding the top 10 stocks, the S&P 500 index has a higher return than the 10-year U.S. Treasury bonds; and the returns of the top 10 stocks are also declining, which should be a strong sell signal:

Authers summarised that generally, the strategy of only buying the largest stocks is a failure because these stocks have no way to go but down, and their competitive position will gradually erode. Even excluding the impact of large-cap stocks, it is difficult to make a positive forecast for the U.S. stock market in the next 10 years. However, it seems that the stock market will continue to rise, so investors should act cautiously.

Editor/rice