The noteworthy changes in global funding this week are: 1) According to the EPFR fund data we track, active foreign funds turned into outflows again after two weeks as of Wednesday (October 16); 2) Regarding the mutual market access, this week, the daily average trading volume of northbound funds narrowed, while southbound fund inflows accelerated; 3) In the global stock market, inflows narrowed but bond inflows expanded, with the opposite happening in the money market turning into outflows; 4) Inflow accelerated in the US and European markets, but outflows expanded in the Japanese market.

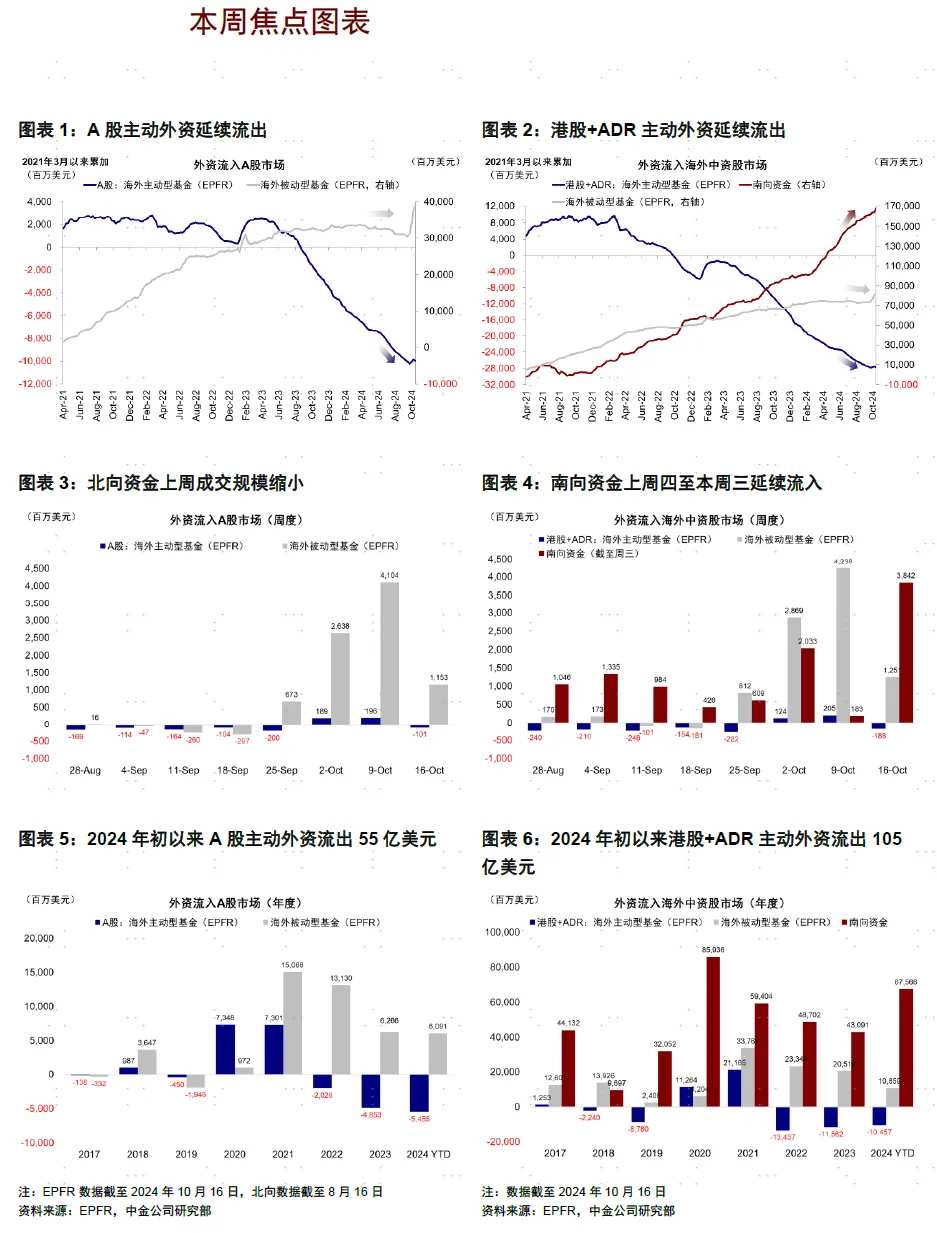

In the domestic market, active funds turned into outflows again after two weeks, and passive fund inflows also slowed significantly. After experiencing a significant rise in Hong Kong and Chinese concept stocks from the end of September to the National Day period, the market clearly cooled down in the past two weeks, with foreign investments following suit. Most of the inflows during the rebound were passive and transactional funds, while the inflow of active funds, which are the main foreign funds, was not significant, mainly due to the need to avoid falling too far behind and being forced to reduce underweight positions.

Recently, as the market started to consolidate, passive fund inflows slowed down significantly this week, only about 1/4 of the previous week, indicating the cooling of non-institutional investors' earlier excitement. At the same time, it is more notable that active funds (long-term institutional LO, accounting for 80% of the existing scale) experienced a minor inflow for two weeks followed by outflows again, confirming our judgment that the earlier LO inflow was mainly aimed at reducing underweight positions to prevent substantial underperformance, while systematic overweights or even significant overweights would require more conditions and stronger expectations. Looking at domestic funds, southbound fund inflows accelerated, focusing mainly on banks and telecommunication services, while selling off targets such as Meituan, Hong Kong Stock Exchange, and Kuaishou, which had leading gains in the previous rebound process, indicating a certain profit-taking.

On a global funding level, inflows accelerated in the US stock market, outflows expanded in the Japanese market, and outflows narrowed in the Indian market. As of Wednesday (October 10-16), active foreign fund outflows in the Indian market narrowed to $0.03 billion (vs. outflows of $0.15 billion the previous week), US stocks continued to have inflows after last week's $0.91 billion inflow, increasing this week to $1.24 billion, while Japanese stocks outflows expanded to $0.33 billion (vs. outflows of $0.23 billion the previous week).

On a global funding level, inflows accelerated in the US stock market, outflows expanded in the Japanese market, and outflows narrowed in the Indian market. As of Wednesday (October 10-16), active foreign fund outflows in the Indian market narrowed to $0.03 billion (vs. outflows of $0.15 billion the previous week), US stocks continued to have inflows after last week's $0.91 billion inflow, increasing this week to $1.24 billion, while Japanese stocks outflows expanded to $0.33 billion (vs. outflows of $0.23 billion the previous week).

In the Chinese market: active foreign funds turned into outflows again, while passive foreign fund inflows narrowed; southbound inflows accelerated.

Overseas funds: EPFR active foreign funds turned into outflows again after two weeks. As of Wednesday (October 10-16), A-share active foreign funds turned into outflows of $0.1 billion (vs. inflows of $0.2 billion the previous week), passive fund inflows were $1.15 billion (vs. $4.1 billion the previous week); at the same time, Hong Kong and ADR overseas funds overall inflowed $1.06 billion (vs. $4.44 billion the previous week), with active funds turning into outflows of $0.19 billion (vs. inflows of $0.2 billion the previous week), and passive fund inflows significantly narrowed to $1.25 billion (vs. $4.24 billion the previous week).

Mutual market access funding: Northbound funds stopped disclosing net purchase amount as of August 16, with daily average trading volume narrowing this week. This week (October 14-18), the daily average trading volume of northbound funds reached 240.8 billion yuan, down from last week's 401.6 billion yuan.

Southbound inflows accelerated, with the most inflows into mainland banks, telecommunication services, and other sectors. This week (October 14-18), southbound funds in total flowed in 24.42 billion Hong Kong dollars, with a daily average inflow of 4.89 billion Hong Kong dollars, an expansion compared to the previous week (average inflow of 4 billion Hong Kong dollars from October 8-10). In terms of industries, mainland banks and telecommunication services received the most southbound funds inflow last week, while diversified finance and software & services sectors mostly experienced outflows.

Global Market: Inflow narrowing in global stock markets, while inflow expanding in bond markets, and currency markets shifting to outflow; US stocks seeing accelerated inflow, with emerging markets turning into outflow.

Cross-Market and Asset: US stocks experience accelerated inflow, as emerging markets shift to outflow. Active foreign investment is on the rise, with US stocks' inflow accelerating to $1.24 billion this week (compared to $0.91 billion inflow last week), developed Europe's outflow increasing to $1.29 billion (compared to $0.87 billion outflow last week), Japan's stock market outflow expanding to $0.33 billion (compared to $0.23 billion outflow last week), and emerging markets turning into outflow of $0.77 billion (compared to $0.06 billion inflow last week). Overall, global stock markets see narrowing inflow, expanding inflow in bond markets, and currency markets shifting to outflow.

Allocation Proportion: As of August 31, active funds' allocation to China is approximately 0.1% below the benchmark. From 2022 to present, active funds globally have shifted from over-allocated to under-allocated in China and India, while still being over-allocated in South Korea, and Japan's under-allocation has decreased. From January 2022 to August 31, 2024, China's allocation proportion has decreased the most (-0.2%), with the UK (+1.8%), France (+0.5%), and Japan (+0.3%) receiving the largest increases in allocation. In terms of region, funds from Europe are the main outflow drivers; on a sector level, overseas funds are over-allocated in China's healthcare, consumer, semiconductor and hardware, and capital goods, while under-allocated in internet, finance, and real estate.

Editor/new