非美货币方面,美元兑日元一度重回150,市场关注日本当局的干预风险,日本最高货币官三村淳警告说他正在观察市场。受降息预期影响,英镑兑美元一度下破1.30,为8月20日以来首次,本周将录得连续第三周下跌。在特朗普关税导致贸易不确定性的环境下,欧元兑美元也已连续四周下跌,

非美货币方面,美元兑日元一度重回150,市场关注日本当局的干预风险,日本最高货币官三村淳警告说他正在观察市场。受降息预期影响,英镑兑美元一度下破1.30,为8月20日以来首次,本周将录得连续第三周下跌。在特朗普关税导致贸易不确定性的环境下,欧元兑美元也已连续四周下跌,"Trump trade" restarts, gold, US dollar, and US stocks surge! Supply concerns are replaced by slowing demand, causing oil prices to plummet. Continuously heavyweight bullish news catalyze market enthusiasm, with "bullish on Chinese stocks" entering the hot trading list... What exciting market trends did you miss out on this week?

Market review

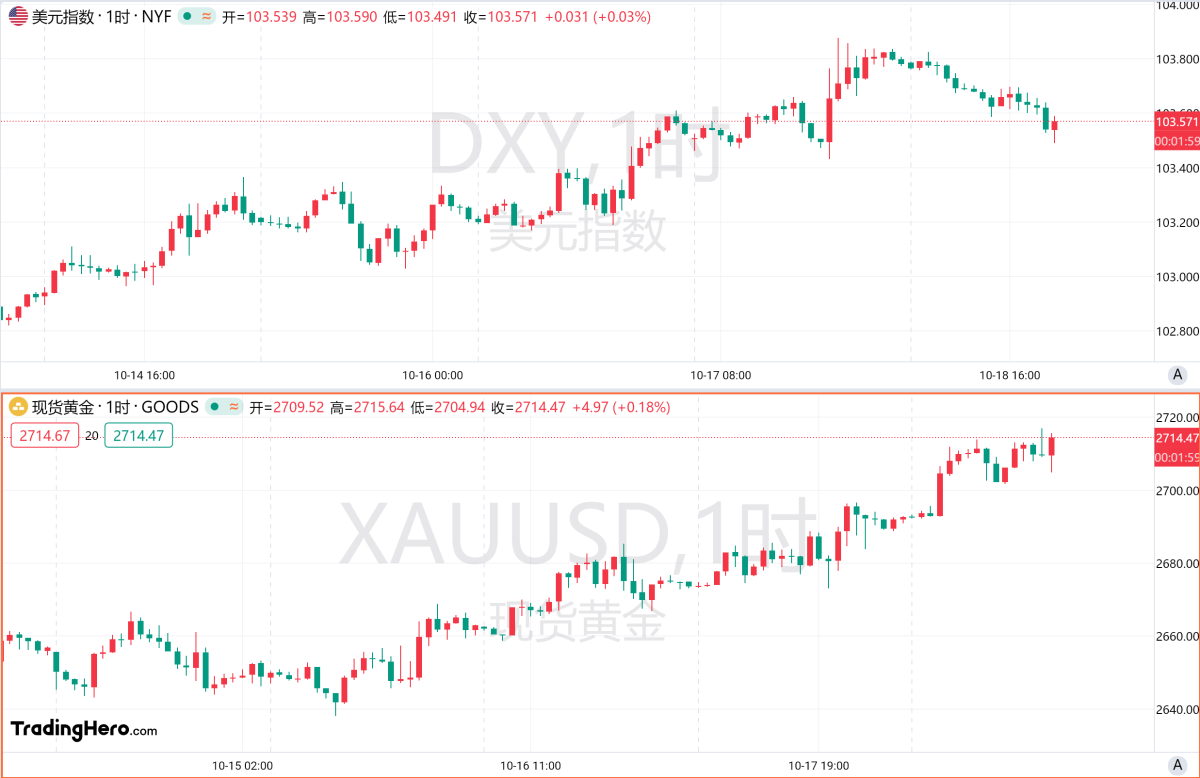

The US dollar index continued to rise this week, extending its three-week uptrend. Multiple data shows a strong performance in the US economy, with market expectations that the Federal Reserve will cut interest rates at a slower pace over the next year and a half. It is also believed that Trump will win the election, potentially boosting the US dollar, with the USD hitting an 11-week high.

Spot gold has not been affected by the rise in the US dollar, as both the USD and gold have risen in sync since October. Uncertainties surrounding the US election and the Middle East conflict have prompted investors to seek safe-haven assets, pushing the price of gold above $2700 per ounce, once again hitting a new historical high. Dow Jones market data shows that the most active gold futures contracts have hit a record high for 34 days this year, the highest since the 38 historical highs in 2011. As of the time of writing, spot gold is hovering near a historical high of $2715 per ounce.

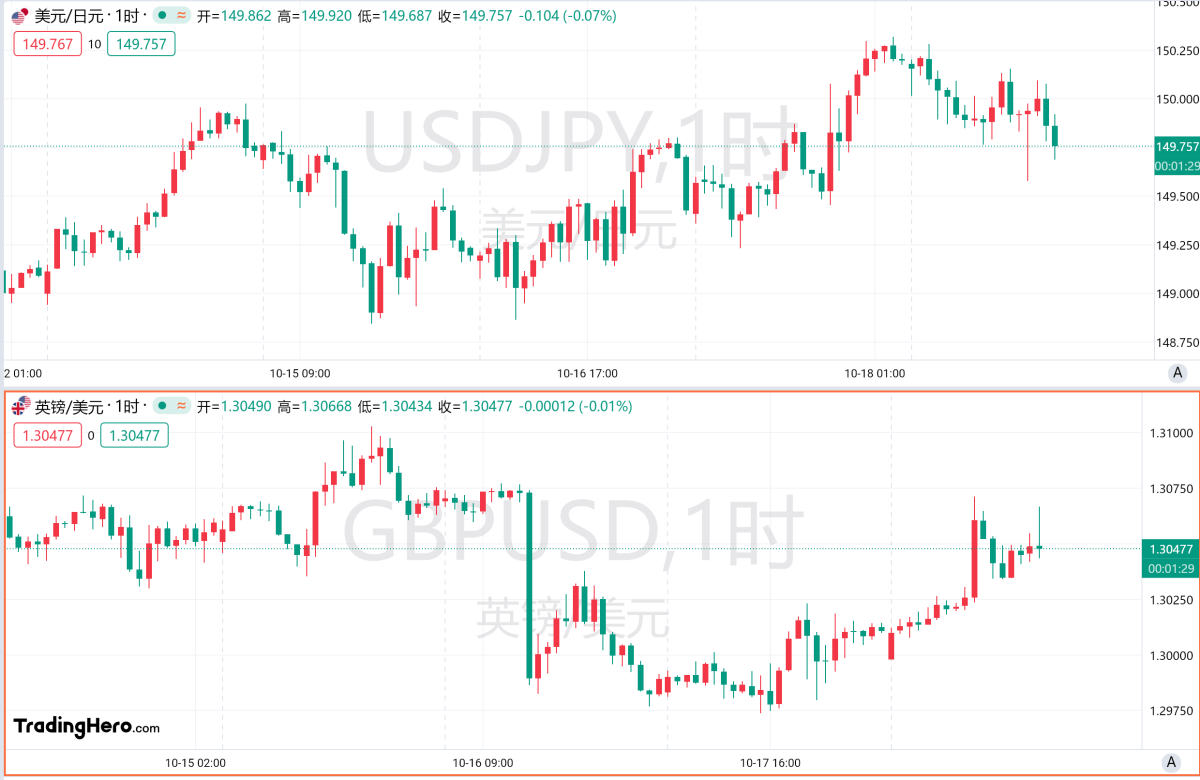

In terms of non-US currencies, the US dollar against the Japanese yen briefly returned to 150, with the market watching for intervention risks from the Japanese authorities. The highest monetary official in Japan, Jun Murai, warned that he is monitoring the market. Due to rate cut expectations, the pound sterling briefly fell below 1.30 against the US dollar, the first time since August 20. This week marks the third consecutive week of decline. In the environment of trade uncertainty caused by Trump's tariffs, the euro against the US dollar has also fallen for four consecutive weeks, raising concerns as it nears parity.

In terms of non-US currencies, the US dollar against the Japanese yen briefly returned to 150, with the market watching for intervention risks from the Japanese authorities. The highest monetary official in Japan, Jun Murai, warned that he is monitoring the market. Due to rate cut expectations, the pound sterling briefly fell below 1.30 against the US dollar, the first time since August 20. This week marks the third consecutive week of decline. In the environment of trade uncertainty caused by Trump's tariffs, the euro against the US dollar has also fallen for four consecutive weeks, raising concerns as it nears parity.

Stronger-than-expected UK retail sales data indicate a potentially strong performance in the country's economy, while signs of a stumbling Eurozone economy are becoming increasingly evident. The euro has fallen to the highest level against the British pound in two and a half years.

International oil prices continued to fall this week. Israel said it would strike military targets in Iran rather than nuclear facilities or oil targets, easing concerns about disrupted supply from Iran, also affected by forecasts of slower growth in oil demand, prices remained near two-week lows. WTI crude oil plummeted 4.5% on Monday, Brent crude oil fell 4.2%. Both oils are expected to fall over 7% this week.

In the stock market, the S&P 500 index hit another all-time high this week, with Goldman Sachs tactical expert Scott Rubner expecting it to rise to 6270 points by the end of the year; capital rotation is driving small-cap indices close to three-year highs; AI demand prospects are boosting Nvidia to refresh its intraday all-time high; Apple hit an intraday all-time high, with a market value reaching 3.61 trillion USD at one point.

A-shares and Hong Kong stocks have seen some adjustments, but surged on Friday under the catalysis of a series of favorable policies. Market and fund optimism remains high. A global survey conducted by Bank of America in October showed that 'long China stocks' ranked in the top three on the hottest trading list this month. Bank of America strategists who accurately predicted the rise in the Chinese stock market last month believe there is still room for further growth. Shen Xia, a well-known macro hedge fund in China, advises retail investors to buy stocks now, citing relatively low valuations and government support policies as bullish factors.

Major events of the week

Incremental funds have arrived! SFISF, share buybacks, increased lending launches

The People's Bank of China officially announced on the 18th that it had jointly issued a notice with the China Securities Regulatory Commission to launch the Securities, Funds, and Insurance Companies Self-financing Interbank Fund Transfer System (SFISF) starting today. Currently, 20 securities and fund companies have been approved to participate in the operation, with a total application amount exceeding 200 billion yuan.

Specifically, the term of the swap is 1 year, and extension can be applied for as needed; the initial operating amount is 500 billion yuan, and the rate for each operation is determined by auction; the range of collateral includes bonds, stock ETFs, CSI 300 component stocks, public REITs, etc., the conversion rate is set according to the risk characteristics of the collateral, and it is more favorable than the market level.

On the other hand, the central bank announced the official launch of share buyback and additional loan to boost holdings. Starting today, 21 national financial institutions can provide related loans to eligible listed companies and major shareholders. In the first month of the second quarter, additional loans can be applied for. For eligible cases, the People's Bank of China provides 100% support for additional loans based on the loan principal, with an initial quota of 300 billion yuan, an interest rate of 1.75%, a term of 1 year, extendable depending on the situation, and the cumulative term is expected to reach 3 years. Pan Gongsheng stated that the central bank's provision of share buybacks and additional loans has specific objectives, and it is the bottom line that credit funds must not illegally enter the stock market.

Pan Gongsheng also stated that it is expected to further reduce the deposit reserve ratio by 0.25-0.5 percentage points before the end of the year based on the market liquidity situation, and it is estimated that the loan prime rate (LPR) announced on the 21st will also decrease by 0.2-0.25 percentage points.

2. A combination of measures to stabilize the real estate market and prevent further decline, with five central departments making significant statements!

Implementing the renovation of 1 million sets of urban villages and old and dangerous houses: ① Priority support for cities above the prefectural level; ② Special loans from development-oriented and policy-based financial institutions; ③ Allowing local governments to issue special bonds; ④ Providing tax incentives; ⑤ Commercial banks issuing loans based on evaluations.

By the end of the year, the credit scale of 'whitelist' projects will be increased to 4 trillion yuan: ① All commercial residential projects loans will be included in the 'whitelist'; ② Optimize the allocation of loan funds to achieve 'the earlier the better'.

Special bonds to acquire existing commercial housing: ① Decided and implemented independently by local authorities; ② Support local areas to increase the area of affordable housing, with 4.5 million people expected to move into affordable housing by the end of the year.

Special bonds to purchase and store land: ① Will study the establishment of special loans for purchasing existing land with relevant departments; ② Study allowing policy banks, commercial banks to provide loans to eligible enterprises for land acquisition, with necessary additional loan support from the central bank; ③ In cities with excessively long inventory turnover periods, guide local areas to temporarily suspend the supply of residential land, and in cities with long inventory turnover periods, implement supply matching demand strategies; ④ Reasonably determine the acquisition price with existing landowners and enterprises.

Existing Home Loan Interest Rates: The average existing home loan interest rates are expected to decrease by around 0.5 percentage points, with the majority of existing home loan interest rates completed batch reduction by October 25.

Real Estate Value-added Tax: Efforts are being made to clarify the cancellation of the connection between ordinary and non-ordinary residential properties in terms of tax policies, mainly involving value-added tax and land value-added tax related policies.

3. Several heavyweight economic data will be announced in our country this week!

According to the preliminary estimates from the National Bureau of Statistics, the GDP for the first three quarters of the year amounted to 94,974.6 billion yuan, growing by 4.8% year-on-year in constant prices. By industry, the value added of the primary industry was 5,773.3 billion yuan, growing by 3.4%; the value added of the secondary industry was 36,136.2 billion yuan, with a growth of 5.4%; the value added of the tertiary industry was 53,065.1 billion yuan, increasing by 4.7%. Looking at the quarters, the GDP grew by 5.3% in the first quarter, 4.7% in the second quarter, and 4.6% in the third quarter. Quarter-on-quarter, the GDP in the third quarter increased by 0.9%.

Data from the People's Bank of China shows that in the first three quarters, China's total imports and exports amounted to 32.33 trillion yuan, a year-on-year increase of 5.3%, marking the first time in history to break the 32 trillion yuan mark for the same period. The imports and exports for each quarter were 10.15 trillion yuan, 11 trillion yuan, and 11.17 trillion yuan respectively, all surpassing 10 trillion yuan, another historical first for the same period.

According to data from the General Administration of Customs, in the first three quarters of this year, renminbi loans increased by 16.02 trillion yuan, with a year-on-year increase of 8.1% in the renminbi loan balance at the end of September; the incremental social financing scale was 25.66 trillion yuan, 3.68 trillion yuan less than the same period last year; the social financing balance at the end of September grew by 8% year-on-year. By the end of September, the broad money supply (M2) increased by 6.8% year-on-year, 0.5 percentage points higher than the previous month, while the narrow money supply (M1) decreased by 7.4% year-on-year. Overall, the total financial indicators in September remained stable, with the credit structure continuing to improve.

4. Betting on the Fed to Only Cut Rates by 25 basis points Next Month Has Increased

Following the release of better-than-expected 'terrifying data' on retail sales and initial jobless claims, traders are expecting a reduced rate cut from the Fed for the remainder of the year.

In September, retail sales growth in the United States slightly exceeded expectations, supporting the view of strong third-quarter economic growth; The number of initial jobless claims in the United States unexpectedly decreased by 0.019 million people last week, the largest drop in three months. Signs of economic recovery are unlikely to prevent the Federal Reserve from cutting interest rates again next month, but it will reinforce the expectation of only a 25-basis-point rate cut.

This week, Federal Reserve Governor Waller believes that the Fed should be more cautious in cutting rates compared to the September meeting if inflation is below 2%, although this is unlikely, or if the labor market deteriorates, the Fed can cut rates preemptively. However, if inflation unexpectedly rises, the Fed may pause rate cuts. Minneapolis Fed President Kashkari indicated that further "moderate" rate cuts seem appropriate. San Francisco Fed President Daly stated that the Fed must remain vigilant to sustain economic growth as inflation and labor market cool.

5. Multiple banks have lowered deposit rates by 0.2 million yuan, resulting in 1500 yuan less interest for a three-year deposit.

On October 18th, Industrial and Commercial Bank of China, China Construction Bank, Bank of Communications, Agricultural Bank of China, and Bank of China have all updated their deposit listing rates. The listing rates for three-month, six-month, one-year, two-year, three-year, and five-year fixed deposits have all been reduced by 25 basis points, with the one-year rate dropping to 1.1%. The 7-day notice deposit rate also synchronously decreased by 25 BP to 0.45%. This is the major banks' second deposit rate cut in less than 3 months since July, and the sixth voluntary deposit rate cut by major banks since September 2022.

The three-year deposit rate decreased by 0.25 percentage points. With a 0.2 million yuan deposit for three years, the interest will be 1500 yuan less after the rate cut. Following the historical path of deposit rate cuts, state-owned banks are expected to lead the rate cut, followed by smaller and medium-sized banks. It is predicted that joint-stock banks will soon initiate deposit rate cuts.

6. Hamas leader Sinwar has died, and Israel may retaliate against Iran before the US election.

According to The Washington Post, Israel has agreed to limit retaliatory actions against Iran to military targets, avoiding attacks on Iran's energy and nuclear facilities. In terms of timing, CNN reports indicate that U.S. officials expect Israel to retaliate for this month's attacks on Iran before the November 5th election.

Iran has conveyed through secret channels to Israel that if Israel's response to attacks on Iran is limited, Iran will consider this round of confrontation between the two countries over.

Israel confirmed this week that Hamas leader Sinwar, who led the attack in southern Israel last October, was killed by the Israeli army. Vice President Harris of the United States stated that Sinwar's death provided an opportunity to end the Gaza war, but Netanyahu stated that Israel will continue to fight until all hostages are released.

7. Win rate soaring! 'Trump Trade' makes a comeback.

With only about three weeks left until the US election day, Trump's advantage in swing states has prompted the market to once again increase its probability of winning, heating up the 'Trump Trade'.

Trump is working to narrow the fundraising gap with Harris, with Musk becoming one of his biggest supporters, donating about $75 million to America PAC, a political group supporting Trump, from July to September.

During an interview this week, Trump emphasized that his tariff-heavy economic policy would stimulate growth, attempting to dispel concerns from the outside world about his economic plan raising inflation. Lutnick, co-chair of Trump's transition team, stated that if Trump wins the election, companies like Apple and Tesla will pay higher taxes in the USA.

Billionaire investor Druckenmiller stated that the market is currently digesting the scenario of a Trump victory based on the performance of assets such as bank stocks and cryptos. Bitcoin is approaching $0.07 million, eyeing historical highs, and analysts say the market will see a perfect storm.

Democratic presidential candidate Harris is reportedly intensifying efforts to win over dissatisfied Republican voters of Trump. Meanwhile, the escalating conflicts in the Middle East have become a key issue in the US election, with President Biden and Vice President Harris facing pressure from the left regarding their handling of the situation. Trump and other Republicans accuse the government of mishandling the crisis, plunging the world into chaos.

8. Wall Street big banks have successively announced impressive financial reports.

Thanks to the growth in stock trading revenue, Goldman Sachs' third-quarter profit soared by 45%; Citigroup's market department achieved its best performance in at least a decade; Bank of America's investment banking and trading businesses, as well as net interest income, all exceeded analysts' expectations; Morgan Stanley announced a sharp increase in third-quarter trading revenue, driving a strong 32% increase in quarterly profit and also stimulating the largest stock price surge in nearly four years.

With the release of impressive financial reports by the major Wall Street banks, bankers are expecting a significant increase in bonuses, indicating that this year is expected to be the highest-paying year for Wall Street banks since the record revenues in 2021.

9. The European Central Bank initiates a continuous interest rate cut mode.

The European Central Bank cut interest rates for the third time this year, with the crucial deposit rate reduced from 3.5% to 3.25%. President Lagarde reiterated that no specific rate path had been predetermined and would maintain restraint as needed; will continue to rely on data to make decisions at subsequent meetings; economic growth risks are skewed to the downside, inflation risks are skewed to the upside; officials did not discuss the option of cutting rates by 50 basis points this week.

Sources said that European Central Bank officials expect inflation to reach 2% in the first or second quarter of next year and consider it very likely to cut rates in December. Traders are increasing bets on the European Central Bank cutting rates at the end of the year, not ruling out a 50 basis point cut, and have nearly fully priced in the scenario of a 25 basis point cut at every meeting until April. Renowned economist El-Erian predicts that the European Central Bank's rate cuts may exceed those of the Federal Reserve.

10. With inflation falling below 2%, the Bank of England is expected to restart rate cuts.

UK data this week showed that September's CPI increased by 1.7% year-on-year, below the central bank's target and reaching the lowest level in three and a half years. Subsequently, traders increased bets on the Bank of England cutting rates, expecting a 24 basis point cut in November and a total of 42 basis points by the end of the year. The Bank of England initiated its first rate cut in August by 25 basis points and paused the cut in September with an 8:1 vote, reiterating the need for 'monetary policy to remain restrictive for a sufficiently extended period of time.'