所谓的Robotaxi,更加像一个“令人眼花缭乱的承诺”,但是这种承诺,或者说是“长期规划”,对于特斯拉股票的持续走高以及维系高估值而言可谓至关重要。Robotaxi也是马斯克本人对于人工智能、人形机器人所全面驱动的特斯拉未来发展愿景的重要组成部分,马斯克此前在特斯拉股东大会上甚至喊出看起来很疯狂的市值预期,马斯克预测在完全自动驾驶技术和擎天柱人形机器人的共同加持下,特斯拉市值将超过30万亿美元。

所谓的Robotaxi,更加像一个“令人眼花缭乱的承诺”,但是这种承诺,或者说是“长期规划”,对于特斯拉股票的持续走高以及维系高估值而言可谓至关重要。Robotaxi也是马斯克本人对于人工智能、人形机器人所全面驱动的特斯拉未来发展愿景的重要组成部分,马斯克此前在特斯拉股东大会上甚至喊出看起来很疯狂的市值预期,马斯克预测在完全自动驾驶技术和擎天柱人形机器人的共同加持下,特斯拉市值将超过30万亿美元。Tesla CEO Musk's "Robotaxi Blueprint" did not receive investor approval. Since the launch of this self-driving taxi, Tesla's stock price has fallen by 7.5% last week.

Zhitong Finance APP learned that Tesla (TSLA.US), the global leader in electric vehicles, disappointed investors in the financial market with the launch of the self-driving taxi Robotaxi last week. Musk, who is good at boosting Tesla's valuation by promising investors, surprisingly failed this time. The "Robotaxi pie" he painted did not gain full approval from Wall Street and Tesla stock believers. This disappointment led some Wall Street investment institutions to question whether the significantly overvalued stock could sustain.

Looking at Tesla's recent stock price trend, Musk's long-touted Robotaxi failed to attract global capital favor. This resulted in Tesla's stock price continuing to fall after the Robotaxi event, with a 7.5% decline since the launch of this self-driving taxi. Bernstein, a Wall Street investment institution, stated that Robotaxi tends to have grand narratives but seems to lack practical significance for Tesla's weak performance and expensive valuation at this stage.

The so-called Robotaxi seems more like a dizzying promise, but this promise, or "long-term plan," is crucial for the continued rise of Tesla's stock and maintaining its high valuation. Robotaxi is also an important part of Musk's vision for Tesla's future development driven by artificial intelligence and humanoid robots. Musk even shouted out what seemed like a crazy market cap expectation at a Tesla shareholder meeting, predicting that with the combined power of fully autonomous driving technology and Optimus humanoid robots, Tesla's market cap will exceed $30 trillion.

The so-called Robotaxi seems more like a dizzying promise, but this promise, or "long-term plan," is crucial for the continued rise of Tesla's stock and maintaining its high valuation. Robotaxi is also an important part of Musk's vision for Tesla's future development driven by artificial intelligence and humanoid robots. Musk even shouted out what seemed like a crazy market cap expectation at a Tesla shareholder meeting, predicting that with the combined power of fully autonomous driving technology and Optimus humanoid robots, Tesla's market cap will exceed $30 trillion.

"Wood Sister", Ark Investment Management, recently updated its target price for Tesla. Ark expects Tesla's stock price to reach $2,600 by 2029. Ark's strong bullish view on Tesla's stock price is mainly based on the expectation that by 2029, nearly 90% of Tesla's market value and profits will be attributed to the Robotaxi self-driving taxi network built on an incredibly powerful AI supercomputing system.

However, as for the actual situation presented at the Robotaxi event, Ark's aggressive expectations seem unrealistic. Due to investors' many questions about the specific technical details of Robotaxi self-driving cars and the rough timeline of the "Robotaxi blueprint," such as the advantages of the updated FSD compared to autonomous driving competitors, FSD regulatory progress, and when Robotaxi will be launched, many market focus areas remain unanswered.

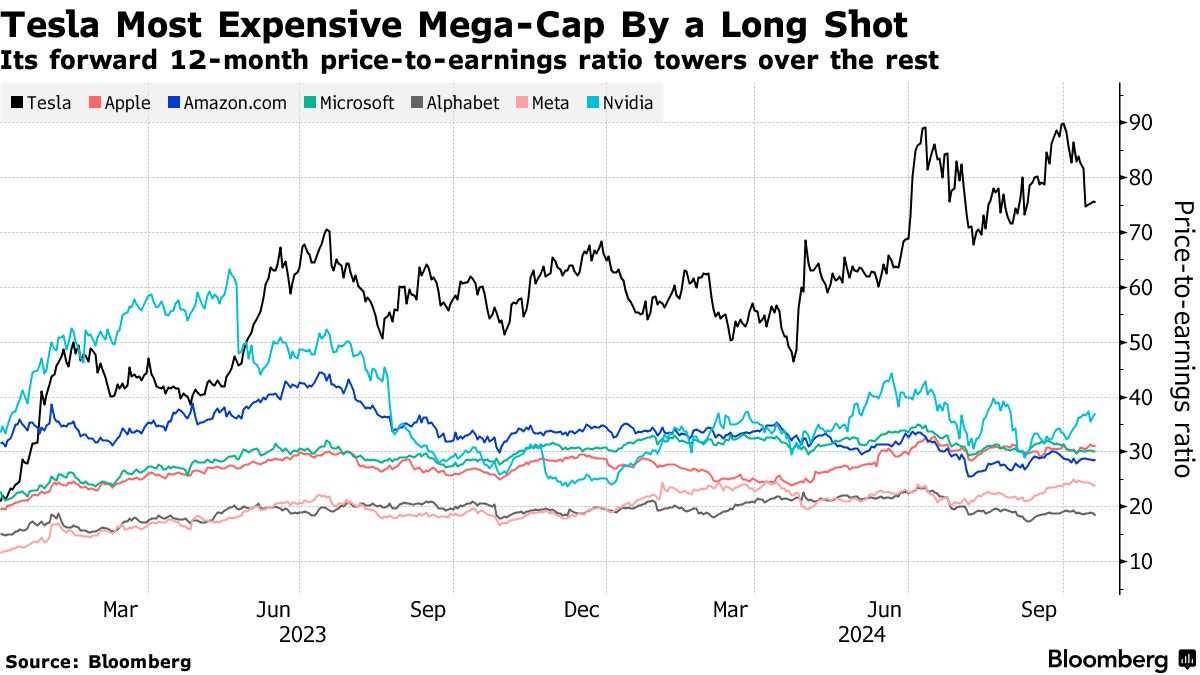

Therefore, Tesla's expected PE ratio of up to 75x appears too high for Wall Street traders and extremely expensive compared to the overall high valuations of American technology giants.

"This is still a carrot on a stick." Chief Strategist Steve Sosnick of Interactive Brokers said. "When Tesla's core automotive business inevitably slows down, and the company has not shown how it will achieve faster growth in the future, how many new investors are willing to buy this expensive stock?"

Outrageous phenomenon: Tesla's valuation is far higher than the Nasdaq 100 Index, yet it significantly underperforms this index.

Indeed, Tesla investors generally have high hopes for the success of the self-driving business and Robotaxi cars. Analyst Tony Sacconaghi from Bernstein estimates that Tesla's core electric vehicle business may be worth less than $200 billion, indicating that its current market valuation reflects the total value of all other businesses (including Robotaxi and Optimus humanoid robots) at around $600 billion. This expectation is clearly very high, and more importantly, this part of the business exists more in a virtual imagination space rather than concrete operational results.

Since the notable Robotaxi event on October 10th, Tesla's stock price has dropped by 7.5%, but this has hardly weakened its overly inflated valuation. Tesla remains the most expensive stock among the 'Magnificent 7' tech giants in the US stock market, and even though its stock price has underperformed almost all tech giants this year, its valuation has long been higher than theirs. Tesla's valuation is even higher than the market cap of the AI chip leader Nvidia, which has a market cap exceeding $3 trillion, far exceeding the moderate undervaluation of traditional auto manufacturing giants like General Motors and Ford Motor.

Furthermore, Tesla's valuation is much higher than the 26x expected PE ratio of the Nasdaq 100 Index, and more outrageously, while Tesla's stock price has fallen by over 10% this year, the Nasdaq 100 index covering giants like Nvidia, Apple, and Tesla itself in technology has risen by over 20%.

"Regarding Tesla's valuation, what concerns me the most is how strong Tesla's performance needs to be to achieve this high PE ratio of 75x," said Steve Sosnick of Interactive Brokers. "The only feasible way is if you have a technology that fundamentally changes the world, just like Tesla has done before, but the current valuation requires a larger-scale technological leap."

Undoubtedly, last week's grand event failed to instill confidence among global investors that this significant leap is forthcoming. Meanwhile, the slowing global demand for electric cars and intensifying competition with numerous Chinese competitors are continuously affecting Tesla's sales and profits.

"Tesla's Robotaxi activity demonstrates a long-term plan, but lacks specific delivery expectations or new drivers for incremental revenue," wrote Saknaji from Bernstein in a report.

In the Robotaxi activity, the company showcased an unmanned autonomous two-door sedan taxi named Cybercab, a concept car, and an upgraded prototype of the Optimus humanoid robot, but lacks many key details that investors hope to see. These include how Tesla will transition from selling advanced driver-assistance features to fully autonomous vehicles, the regulatory approval process and timeline, and evidence proving that its Robotaxi is far ahead of competitors like Alphabet Inc.'s Waymo.

There are other more serious issues. For example, the Robotaxi autonomous taxi 'may' not be in production until 2026. Earlier this week, reports surfaced suggesting that some employees may have remotely controlled certain functions of Tesla's humanoid robot during the activity.

Saknaji from Bernstein pointed out that Tesla still lags far behind competitors in terms of regulatory approval for autonomous driving technology, expressing concerns that even though it may be the first electric vehicle company to achieve fully autonomous driving that liberates human hands, competitors may quickly follow Tesla's lead.

"We believe that the Robotaxi event did not provide enough details to alleviate our concerns, and we believe that many investors may share the same concerns."

Bullish view: As long as Musk is alive, there is no reason to be bearish on Tesla.

It is certain that there are still some Tesla call believers or Elon Musk fans willing to give Tesla a chance to continue performing, and this view is mainly based on their long-standing trust in Musk himself.

"Firstly, Tesla is a technology company managed by Musk," said Nicholas Colas, co-founder of DataTrek Research. "As long as Musk is still alive, generating novel ideas, succeeding in other innovative businesses, people will say, if this person can make rockets return precisely, he can certainly solve all issues related to autonomous driving."

However, despite this, Tesla's stock price once rebounded sharply by 70% before the Robotaxi self-driving taxi activity, Tesla's stock price still appears to be facing significant challenges.

The next core catalyst worth paying attention to is the third-quarter performance to be announced next week, Wall Street analysts widely expect the company's profit to show a year-on-year decline of 10%, mainly due to weak demand for electric cars under the long-term high interest rates of the Federal Reserve and the intensifying market competition in the electric car industry.

"In the short term, what worries us is any substantial soft data related to electric car sales, which is still Tesla's 'bread and butter'". Brian Mobley, portfolio manager at Zacks Investment Management, said.