The domestic liquidity environment is expected to remain loose, providing stable high-yield quality assets relatively scarce, thus, quality assets in the Hong Kong stock market with a dividend yield of 6% or even higher are favored.

According to the information from the International Finance News app, Guosen Securities released a research report stating that the domestic liquidity environment is expected to remain loose, providing stable high-yield quality assets relatively scarce, thus, quality assets in the Hong Kong stock market with a dividend yield of 6% or even higher are favored. In a low interest rate environment, the value of Hong Kong dividend assets allocation is highlighted. From the perspective of AH premiums, Hong Kong low-volatility dividend assets remain attractive. At the same time, the bank stated that domestic policies continue to strengthen the dividend system construction, and the dividend strategy aligns with policy orientation. The central bank stated that it will establish repurchase and additional loans to guide commercial banks to provide loans to listed companies and major shareholders, which means that major shareholders can increase their holdings of company stocks at lower costs, and have more incentive to increase the dividend ratio to obtain yield differentials. As a result, the allocation value of dividend varieties is further highlighted.

Guosen Securities believes that based on the basic allocation direction of Hong Kong dividend assets, it has further constructed a portfolio of 'Hong Kong central state-owned enterprises dividends + Hong Kong low-volatility dividends'. The bank stated that under the policy guidance of state-owned enterprise reform, the revaluation of high-quality high-dividend central state-owned enterprises is timely, with the stability and enhanced power of dividends in central state-owned enterprises. In market fluctuations, low-volatility dividend assets are excellent defensive varieties in the combination of 'Hong Kong central state-owned enterprises dividends + Hong Kong low-volatility dividends'. By integrating central enterprises and low volatility, two major long-term superior factors on the basis of dividends, it is expected to achieve a '1+1>2' effect.

1. Hong Kong Dividend Policy Persists in Steady Progress

1. Hong Kong Dividend Policy Persists in Steady Progress

1.1. Under the high winning investment paradigm, emphasis on the new bottom asset attributes of dividend assets

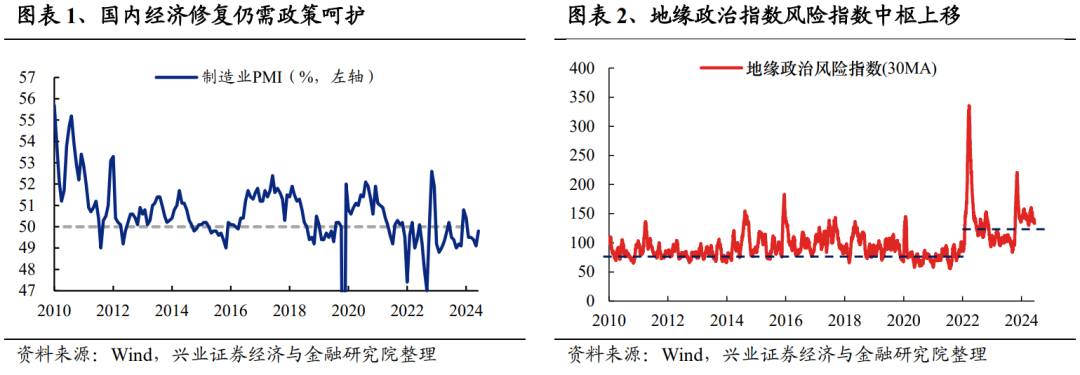

The global economic and political outlook has low visibility, and dividend assets are expected to continue to receive a certainty premium. Domestically, the current PMI is still running below the boom-bust line, and economic recovery still needs further macro policy nurturing; externally, with the escalation of the Russia-Ukraine conflict, the Israel-Palestine conflict, the global geopolitical situation is increasingly complex, and the geopolitical risk index has shifted upwards. Against the background of short-term uncertainty and disturbances both domestically and internationally that are difficult to eliminate, the pursuit of certainty makes high-winning rate investment a new consensus in the market. Dividend assets that provide relatively stable profits and certain dividend returns as natural high-winning rate assets are expected to continue to be the focus of the market as core assets.

1.2. In a low interest rate environment, the value of Hong Kong-listed dividend assets allocation is highlighted.

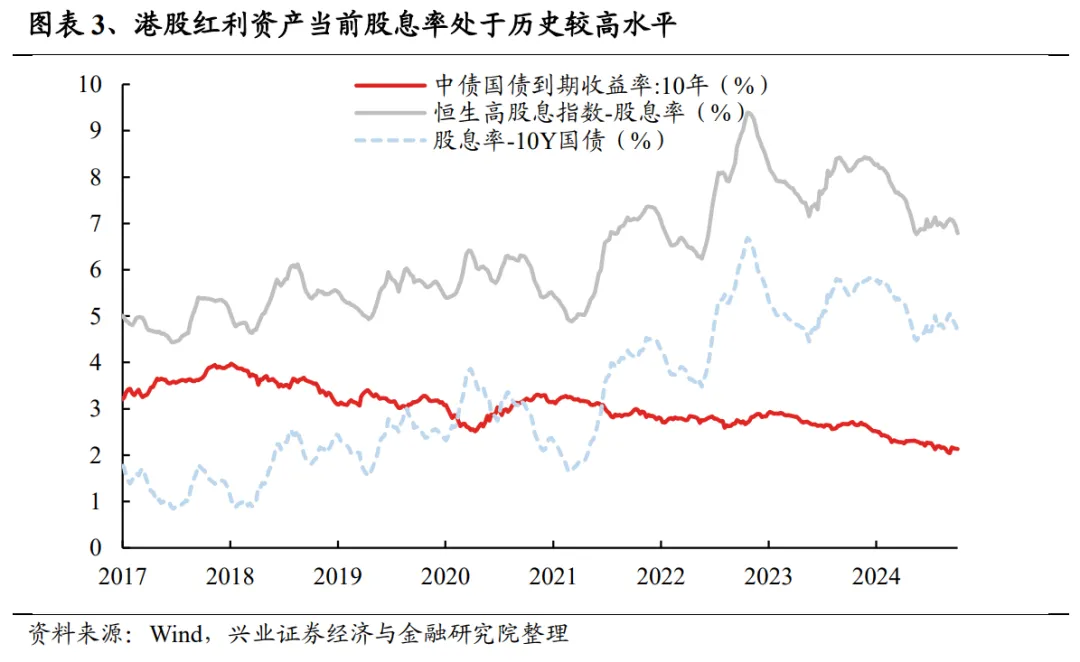

The domestic liquidity environment is expected to remain loose, providing scarce quality assets with stable high returns. Therefore, high-quality assets in the Hong Kong stock market with a dividend yield of 6% or even higher are favored. As bank wealth management yields continue to decline, long-term national bond rates are also easily stagnating under loose liquidity conditions. However, Hong Kong dividend assets (using the Hang Seng High Dividend Yield Index as an example) currently have a dividend yield of over 6.6%, still at a historically high level, with a yield spread of over 4 percentage points compared to ten-year national bond yields, possessing high allocation value.

1.3. The pricing power of northbound funds for low-volatility dividend assets in Hong Kong is still increasing.

In a low interest rate environment, allocation-type mainland Chinese assets are to some extent facing an 'asset shortage'. Particularly, the fixed income departments of mainland public fund companies, insurance, bank wealth management subsidiaries, and other institutions have a strong demand for high-quality, effective assets. High-quality Hong Kong stocks with deep value and high dividend yields have long-term allocation attractiveness. In 2024 (as of October 16, 2024), southbound funds have bought Hong Kong stocks with a net amount of approximately 489.8 billion RMB, reaching a new high in nearly four years; Among the top ten net inflows of southbound funds calculated by the holdings of the top ten active individual stocks, dividend assets hold 6 seats, including Bank of China (03988), China Mobile (00941), CNOOC (00883), China Construction Bank Corporation (00939), Industrial and Commercial Bank of China (01398), and Ping An Insurance (02318).

Southbound funds are gradually gaining pricing power over low-volatility dividend Hong Kong stocks. Compared to the beginning of 2024, as of October 16, 2024, the shareholding proportion of Hong Kong low-volatility dividend assets, represented by telecommunications operators, banks, and energy companies, through the Hong Kong Stock Connect has increased.

1.4, Capital market policies emphasize dividend returns, and dividend strategies are in line with policy guidance.

Domestic policies continue to strengthen the construction of the dividend system, and dividend strategies are in line with policy guidance. In recent years, the China Securities Regulatory Commission has been continuously promoting the construction of the dividend system, and the capital markets are paying increasing attention to investor returns. On September 24, 2024, at a press conference held by the State Council Information Office, the central bank governor stated that they will establish repurchase and shareholding refinancing, guiding commercial banks to provide loans to listed companies and major shareholders, which means that major shareholders will be able to increase their holdings of company stocks at a lower cost, and they will have greater motivation to increase the dividend ratio to gain interest rate differential income. As a result, the allocation value of dividend varieties is further highlighted.

1.5, From the perspective of AH premium, Hong Kong's low-volatility dividend assets remain attractive.

From the perspective of AH stocks, as of October 16, 2024, the AH premium index was 145.05, which is still at a relatively high level. Comparing the dividend yields of AH shares listed in both places (in the past 12 months), H-shares have higher dividend yields than A-shares (in the past 12 months). Even considering the approximately 20-28% dividend tax that Hong Kong stocks will face when investing through the stock connect program, Hong Kong high-dividend stocks are still more attractive.

2, Strategy construction: Hong Kong-listed central state-owned enterprises dividends + Hong Kong low-volatility dividends.

Based on the basic allocation direction of Hong Kong dividends, the bank further constructs a portfolio of [Hong Kong-listed central state-owned enterprises dividends + Hong Kong low-volatility dividends]. Specifically:

Under the guidance of state-owned enterprise reform policies, the reevaluation of high-quality and high-dividend central state-owned enterprises' value is timely.

Under the guidance of state-owned enterprise reform policies, the stability and momentum of dividends of central state-owned enterprises are enhanced. In May 2022, the SASAC issued the "Improving the Quality of Central SOE-Held Listed Companies Work Plan" (referred to as the "Plan" in this article), pointing out that some central enterprises have a mismatch between "value realization and value creation", and also mentioned that by the end of 2024, each central enterprise group's work plan will be assessed to evaluate the quality of listed companies. After 2023, a series of policies were implemented more intensively, including: SASAC optimizing the operating indicator system of central enterprises to "one benefit and five rates", central enterprises enhancing the quality of listed company's work through special meetings, and launching state-owned enterprises' actions to benchmark world-class enterprises. On January 24, 2024, the SASAC announced to "further study to include market value management in the performance assessment of central enterprise leaders". This is the first time that the SASAC has mentioned including "market value management" in the performance assessment system.

The enhancement of enterprise profit stability and the improvement of cash flow levels are important supports for enhancing dividend capability. The "Plan" and the SASAC's optimization of the operating indicator system of central enterprises to "one benefit and five rates" show that in the new era, central state-owned enterprises are shifting their focus from revenue scale to profitability and cash dividends. Including "market value management" in the performance assessment system serves as a guiding tool to encourage listed companies to "timely pass on confidence, stabilize expectations, and increase cash dividend intensity through market-oriented shareholding, repurchase, and other means".

Looking at the industry distribution, the energy (oil and petrochemical + coal) sector in the Guoxin Hong Kong Stock Connect Central State-Owned Enterprises Dividend Index has a high allocation proportion of 46%, indicating that the index is quite aggressive.

Amid market fluctuations, low-volatility dividend assets are excellent defensive assets.

Low volatility factor is one of the most common defensive factors, often showing significant excess returns in volatile markets. Looking at the annual data from 2015 to 2024, the Hong Kong Stock Connect Low Volatility Dividend Index demonstrates a "absolute in bull markets, relative in bear markets" characteristic, meaning that it can follow the market trends and achieve significant absolute returns during market uptrends, while being relatively resistant to market corrections, highlighting its defensive attributes.

From the perspective of industry distribution, the configuration proportion of sectors such as banks, transportation, and utilities in the stated-owned enterprises listed on HKEX dividend low volatility index is approximately 40%, indicating that the index has a considerable defensive attribute.

2.3 Portfolio Historical Performance

The portfolio combination of csi central state-owned enterprises dividend index and hkex dividend low volatility integrates two major long-term performance factors, state-owned enterprises and low volatility, on the basis of dividends, which is expected to achieve a "1+1>2" effect. For example, in the bear market from 2018 to Q1 2019, the low volatility factor made the portfolio more resistant to decline compared to the large-cap stocks; and in the first half of 2023's mid-special estimated market, the state-owned enterprise factor also contributed to the portfolio's good performance.

Risk warning

Unexpected fluctuations in macroeconomic policies both domestically and internationally.