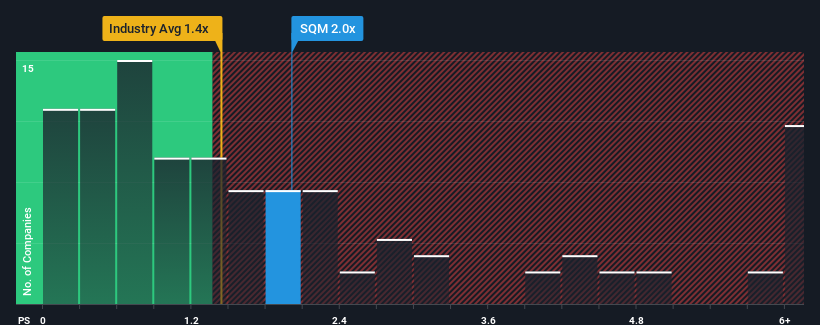

When you see that almost half of the companies in the Chemicals industry in the United States have price-to-sales ratios (or "P/S") below 1.4x, Sociedad Química y Minera de Chile S.A. (NYSE:SQM) looks to be giving off some sell signals with its 2x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

What Does Sociedad Química y Minera de Chile's P/S Mean For Shareholders?

Recent times haven't been great for Sociedad Química y Minera de Chile as its revenue has been falling quicker than most other companies. Perhaps the market is predicting a change in fortunes for the company and is expecting them to blow past the rest of the industry, elevating the P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Sociedad Química y Minera de Chile.Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, Sociedad Química y Minera de Chile would need to produce impressive growth in excess of the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 47%. However, a few very strong years before that means that it was still able to grow revenue by an impressive 165% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 47%. However, a few very strong years before that means that it was still able to grow revenue by an impressive 165% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 7.1% per annum over the next three years. That's shaping up to be similar to the 6.7% per year growth forecast for the broader industry.

With this in consideration, we find it intriguing that Sociedad Química y Minera de Chile's P/S is higher than its industry peers. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. Although, additional gains will be difficult to achieve as this level of revenue growth is likely to weigh down the share price eventually.

The Bottom Line On Sociedad Química y Minera de Chile's P/S

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Analysts are forecasting Sociedad Química y Minera de Chile's revenues to only grow on par with the rest of the industry, which has lead to the high P/S ratio being unexpected. When we see revenue growth that just matches the industry, we don't expect elevates P/S figures to remain inflated for the long-term. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

It is also worth noting that we have found 3 warning signs for Sociedad Química y Minera de Chile (2 don't sit too well with us!) that you need to take into consideration.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.