The Scotts Miracle-Gro Company (NYSE:SMG) shares have continued their recent momentum with a 26% gain in the last month alone. Looking back a bit further, it's encouraging to see the stock is up 79% in the last year.

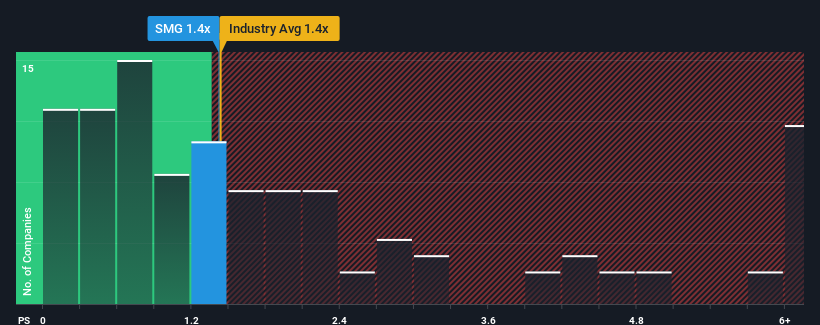

Even after such a large jump in price, there still wouldn't be many who think Scotts Miracle-Gro's price-to-sales (or "P/S") ratio of 1.4x is worth a mention when it essentially matches the median P/S in the United States' Chemicals industry. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

How Has Scotts Miracle-Gro Performed Recently?

Scotts Miracle-Gro's negative revenue growth of late has neither been better nor worse than most other companies. The P/S ratio is probably moderate because investors think the company's revenue trend will continue to follow the rest of the industry. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value. In saying that, existing shareholders probably aren't too pessimistic about the share price if the company's revenue continues tracking the industry.

Want the full picture on analyst estimates for the company? Then our free report on Scotts Miracle-Gro will help you uncover what's on the horizon.Is There Some Revenue Growth Forecasted For Scotts Miracle-Gro?

The only time you'd be comfortable seeing a P/S like Scotts Miracle-Gro's is when the company's growth is tracking the industry closely.

The only time you'd be comfortable seeing a P/S like Scotts Miracle-Gro's is when the company's growth is tracking the industry closely.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 4.3%. The last three years don't look nice either as the company has shrunk revenue by 31% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 2.9% per year as estimated by the eight analysts watching the company. With the industry predicted to deliver 6.7% growth per year, the company is positioned for a weaker revenue result.

In light of this, it's curious that Scotts Miracle-Gro's P/S sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

The Bottom Line On Scotts Miracle-Gro's P/S

Scotts Miracle-Gro's stock has a lot of momentum behind it lately, which has brought its P/S level with the rest of the industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our look at the analysts forecasts of Scotts Miracle-Gro's revenue prospects has shown that its inferior revenue outlook isn't negatively impacting its P/S as much as we would have predicted. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. A positive change is needed in order to justify the current price-to-sales ratio.

Before you settle on your opinion, we've discovered 2 warning signs for Scotts Miracle-Gro (1 is potentially serious!) that you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.