过去一周,有关美联储不会在11月会议上进一步降息的猜测不断升温。美国9月就业报告帮助缓解了对就业市场迅速恶化的担忧,该报告显示,

过去一周,有关美联储不会在11月会议上进一步降息的猜测不断升温。美国9月就业报告帮助缓解了对就业市场迅速恶化的担忧,该报告显示,Source: Wind

This week, Wall Street will focus on the US retail sales data to assess whether the economic situation will prompt the Federal Reserve to keep interest rates unchanged in November.

In addition, the European Central Bank will announce its interest rate decision. $Bank of America (BAC.US)$Please use your Futubull account to access the feature.$Goldman Sachs (GS.US)$ and $Morgan Stanley (MS.US)$ Will announce earnings report, while $Netflix (NFLX.US)$the latest financial data will impact the sentiment of technology stocks this week.

The probability of a 25 basis point rate cut in November exceeds 80%.

Speculation that the Federal Reserve will not further cut interest rates at the November meeting has been increasing over the past week. The September U.S. employment report helped alleviate concerns about rapid deterioration in the job market, showing a drop in the unemployment rate again and one of the highest monthly job gains of the year.

Speculation that the Federal Reserve will not further cut interest rates at the November meeting has been increasing over the past week. The September U.S. employment report helped alleviate concerns about rapid deterioration in the job market, showing a drop in the unemployment rate again and one of the highest monthly job gains of the year.

In addition, the latest Consumer Price Index (CPI) report in the USA shows that the core CPI increase is higher than expected; the latest Producer Price Index (PPI) also presents a similar situation, with a 2.8% year-on-year increase in core PPI in the USA in September, while Wall Street's expectation was 2.6%.

Regarding rate cuts, the Federal Reserve's Williams stated that shifting policy towards neutrality as time progresses is appropriate. CME's 'Fed Watch' latest data shows an 86.9% probability of a 25 basis point rate cut in November, a 13.1% probability of maintaining the current interest rate, and an 86.2% probability of a cumulative 50 basis point rate cut by December.

Based on the latest US economic data, a soft landing of the US economy with inflation gradually falling remains the macro theme. In addition, with the November Fed interest rate meeting following the US midterm elections, it is expected that the likelihood of a single 25 basis point rate cut in November and December is higher.

Caitong Securities' Chief Macro Analyst Chen Xing's team believes that before the November Fed rate decision meeting, there will still be one more release of non-farm payroll data. Considering the strong momentum in the labor market, the economy may not quickly weaken in the short term, and the Fed may be more cautious about rate cuts. The Fed is more likely to cut rates by 25 basis points in November.

Overall, CPI data exceeded market expectations, but initial jobless claims were weak. The market expects a 25 basis point rate cut in both November and December, with an increased probability of a rate cut in November, leading to an upward trend in gold prices.

According to the CME Fed Watch Tool from the Chicago Mercantile Exchange, as of October 11th, the market expects about an 18% chance that the Fed will not cut rates in November, up from 3% a week ago.

On October 17th, the United States will release the retail sales report for September. Economists expect a 0.2% increase in retail sales from the previous month. In August, US retail sales rose by 0.1%, breaking the economists' predicted downward trend.

Jefferies' economic team led by Thomas Simons wrote in a report to clients: "Retail sales may become a particularly important factor influencing the market, as the divergence in this data has widened and scrutiny of consumer health has intensified. It is worth noting that retail sales data heavily weigh on spending, primarily on commodity expenditure rather than service expenditure, and the softness in this data may be due to persisting anti-inflation or deflation of commodities."

Will the European Central Bank cut rates?

On October 17th, this Thursday, the European Central Bank will convene another monetary policy meeting, where the ECB may once again adjust the deposit facility rate. Currently, the market unanimously expects the ECB to further cut rates, but there is a debate on whether it will be a larger-than-expected rate cut.

The current market widely believes that there is a higher probability of the European Central Bank cutting rates by 25 basis points this week. This is mainly due to the following reasons:

With a decrease in inflation: In September, the CPI in the Eurozone increased by 1.8% year-on-year, the first time in three years it fell below the European Central Bank's 2% target level. Inflation continues to decline, creating conditions for interest rate cuts.

Weak economic growth: The momentum of economic growth in the Eurozone is insufficient, with GDP growth in the second quarter reaching only 0.2%. Economic growth is under pressure. The inhibitory effect of high interest rates on economic growth is becoming increasingly evident. High interest rates have led to a large interest burden on the private sector in Europe, poor financial expectations and credit availability for households, and persistently weak confidence indicators such as investor confidence and manufacturing indicators.

Statement from central bank officials: ECB President Lagarde and some board members have given clear signals, stating that "it is very likely to have consecutive rate cuts."

However, there are also views that the interest rate cut decision is not entirely certain and there may be some uncertainty. Several weeks ago, reports indicated that doves pushing for rate cuts may face resistance from hawks. The final decision will still depend on the ECB's comprehensive assessment of the current economic situation and inflation prospects, as well as its judgment on future economic trends.

Analysts from Bank of America believe that the magnitude of the interest rate cut will far exceed the general expectations and market pricing. Market pricing suggests that the European deposit rate will be reduced from the current 3.50% to 2.00%.

HSBC's senior economist Fabio Balboni believes that the central bank deposit rate, as the policy rate, will decrease from the current 3.5% to 2.25% by April 2025.

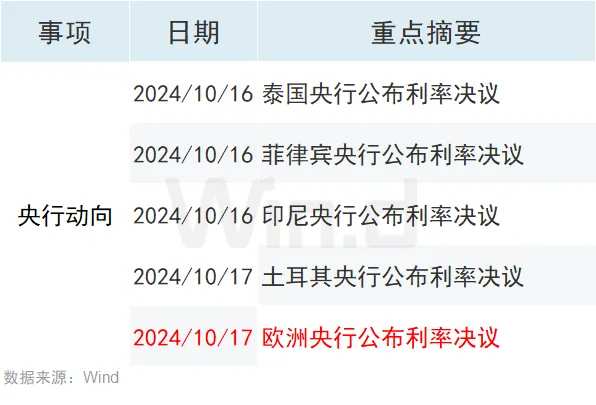

In addition, the central banks of Thailand, the Philippines, Indonesia, and Turkey have announced interest rate decisions.

Netflix's financial report is the focus of attention.

At the beginning of this week, investors' attention will still be focused on financial stocks, morgan stanley, goldman sachs, and bank of america will release earnings reports, and the market focus will shift to Netflix's earnings report after the market closes on October 17.

The stock price of this streaming giant has risen by about 50% this year, nearing its all-time high. Wall Street expects Netflix to have an EPS of $5.16 and revenue of $9.77 billion. This indicates a nearly 40% growth in earnings compared to the previous year.

But Wall Street is intensely discussing whether the stock can maintain its significant upward momentum. In the short term, Citigroup analyst Jason Bazinet believes that Netflix's announcement of further price increases in the United States could act as a catalyst for the stock.

Bazinet stated: "We expect that after announcing the price hike, Netflix's stock will rise, but as investors' expectations of an EPS of $25 by 2025 are shattered, Netflix's stock price will ultimately decline."

MoffettNathanson analyst Robert Fishman stated: "Netflix's engagement, meaning the time users spend on the platform, shows signs of weak growth. If the weak growth in engagement is due to actual weak user growth, then this means that the increase in subscription numbers we see is just a monetization of the existing user base - in other words, a price increase in reality."

Editor/Rocky