同时,台积电三季度营收预计也基本符合汇丰银行和市场一致预期,分别为7430亿新台币和7490亿新台币。汇丰预计台积电3Q24的毛利率为55.5%(市场一致预期为54.7%),达到指引范围53.5%至55.5%的高端。

同时,台积电三季度营收预计也基本符合汇丰银行和市场一致预期,分别为7430亿新台币和7490亿新台币。汇丰预计台积电3Q24的毛利率为55.5%(市场一致预期为54.7%),达到指引范围53.5%至55.5%的高端。HSBC recently released research reports stating that taiwan semiconductor's performance will continue to be at the high end of its performance guidance, indicating that the company's 2-nanometer technology accelerated mass production and pricing increases will drive profit margin expansion in the next two years, leading to profit growth. Nomura Securities, on the other hand, expects that taiwan semiconductor may indicate that its advanced packaging business will still be in short supply before 2026.

Taiwan Semiconductor will release its third-quarter financial report this Thursday. HSBC recently released research reports believing that Taiwan Semiconductor's performance will continue to be at the high end of its performance guidance. They believe that the company's 2-nanometer technology accelerating mass production and pricing improvements will drive profit margin expansion over the next two years, leading to profit growth.

HSBC: 2-nanometer mass production next year to assist profit expansion.

HSBC stated that Taiwan Semiconductor's third-quarter revenue and gross margin reached the high end of the company's guidance range. The total monthly sales from July to September were 760 billion New Taiwan Dollars (a 13% increase from the previous month), exceeding the revenue guidance range of 728 billion to 754 billion New Taiwan Dollars for the third quarter.

At the same time, Taiwan Semiconductor's third-quarter revenue is expected to basically meet the expectations of HSBC and the market, with estimates at 743 billion New Taiwan Dollars and 749 billion New Taiwan Dollars respectively. HSBC expects a gross margin of 55.5% for TSMC in 3Q24 (market consensus is 54.7%), reaching the high end of the guidance range of 53.5% to 55.5%.

At the same time, Taiwan Semiconductor's third-quarter revenue is expected to basically meet the expectations of HSBC and the market, with estimates at 743 billion New Taiwan Dollars and 749 billion New Taiwan Dollars respectively. HSBC expects a gross margin of 55.5% for TSMC in 3Q24 (market consensus is 54.7%), reaching the high end of the guidance range of 53.5% to 55.5%.

Taiwan Semiconductor had previously estimated its capital expenditures for 2024 to be between 30 billion and 32 billion US dollars. HSBC believes the company's capital expenditures in 2024 will be close to the high end, reaching 32 billion US dollars, higher than the market's consensus expectation of 30.5 billion US dollars. The bank expects TSMC's capital expenditure growth to continue into 2025, raising the capital expenditure forecast from 36.5 billion US dollars to 39 billion US dollars, a 22% year-on-year increase (market consensus is 35 billion US dollars, a 16% increase year-on-year).

HSBC indicates that this is because Taiwan Semiconductor will continue to invest in expanding CoWoS (chip packaging technology) capacity, which is still restricted when facing the demand for artificial intelligence, while the 2-nanometer technology is accelerating mass production. Taiwan Semiconductor's management mentioned in the last earnings conference call that the development progress of 2 nanometers is ahead of schedule, with mass production expected to begin in 2025.

HSBC expects that 2 nanometers will start contributing to revenue in the second half of 2025. The bank believes that compared to 3 nanometers, 2 nanometers show better customer engagement. Therefore, the utilization rate of 2 nanometers may be higher than that of 3 nanometers. The research reports suggest that the pricing of 2 nanometers will be 33% higher than 3 nanometers, coupled with higher utilization rates, which should help drive profit margin expansion in 2025 and 2026, leading to profit growth.

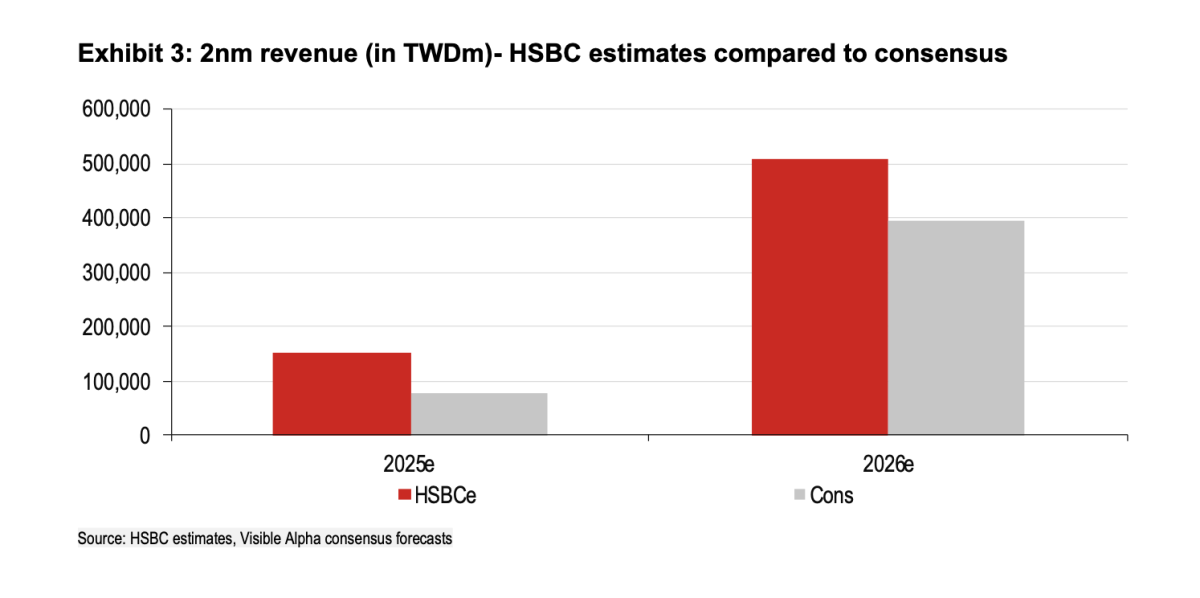

In 2026 (the first full year after the launch of 2-nanometer technology), HSBC expects the 2-nanometer business to contribute NT$507 billion in revenue, 28% higher than market expectations. In comparison, TSMC's 3-nanometer technology contributed NT$160 billion in its first full year (2023).

Therefore, HSBC reiterates a "buy" rating with a target price raised to NT$1535, up from NT$1410. HSBC has also raised the earnings per share forecast for fiscal year 2024 and 2025 by 4% and 9% respectively, reflecting better revenue and profit margins in 3Q24, as well as contributions from 2-nanometer technology starting from the second half of 2025. The research report believes that TSMC will maintain its leading position in advanced node manufacturing and become a major beneficiary of artificial intelligence/high-performance computing growth.

Nomura: TSMC remains one of the core holdings in the AI cycle.

Nomura Securities' research report states that TSMC is one of the core semiconductor holdings in the ongoing AI cycle. The institution believes that although non-AI related businesses, accounting for over 80% of TSMC's revenue, face downward risks, the supply chain has taken cautious construction measures, with a significant cyclical rebound expected by 2025.

Nomura expects that the ramp-up of NVIDIA's Blackwell chips and mobile chips will support TSMC's 5-nanometer, 4-nanometer, and 3-nanometer capacity utilization, thereby driving revenue growth of over 10% sequentially in the fourth quarter of 2024 and an annual revenue increase of 28% year-on-year (in USD).

Combining the 5%-10% pricing increase for 5-nanometer, 4-nanometer, and 3-nanometer nodes and CoWoS starting in the first quarter of 2025, expanded AI CoWoS production, and potential incremental outsourcing from Intel, Nomura forecasts a 24% year-on-year revenue growth in 2025 (in USD). The research report anticipates that the improved pricing dynamics and efficiency gains from the transition from 5-nanometer to 3-nanometer in 2024 will offset the drag from overseas factory production, supporting a gross margin of over 55%, believed to become the new norm. Overall, Nomura has raised the earnings per share and target price for 2024-2026 to NT$1355.

Moreover, Nomura believes that while Intel may outsource 20% of Panther Lake chip production to TSMC, the bank does not consider this additional revenue significant. It is expected that this foundry revenue will account for 10% of TSMC's revenue between 2025 and 2026.

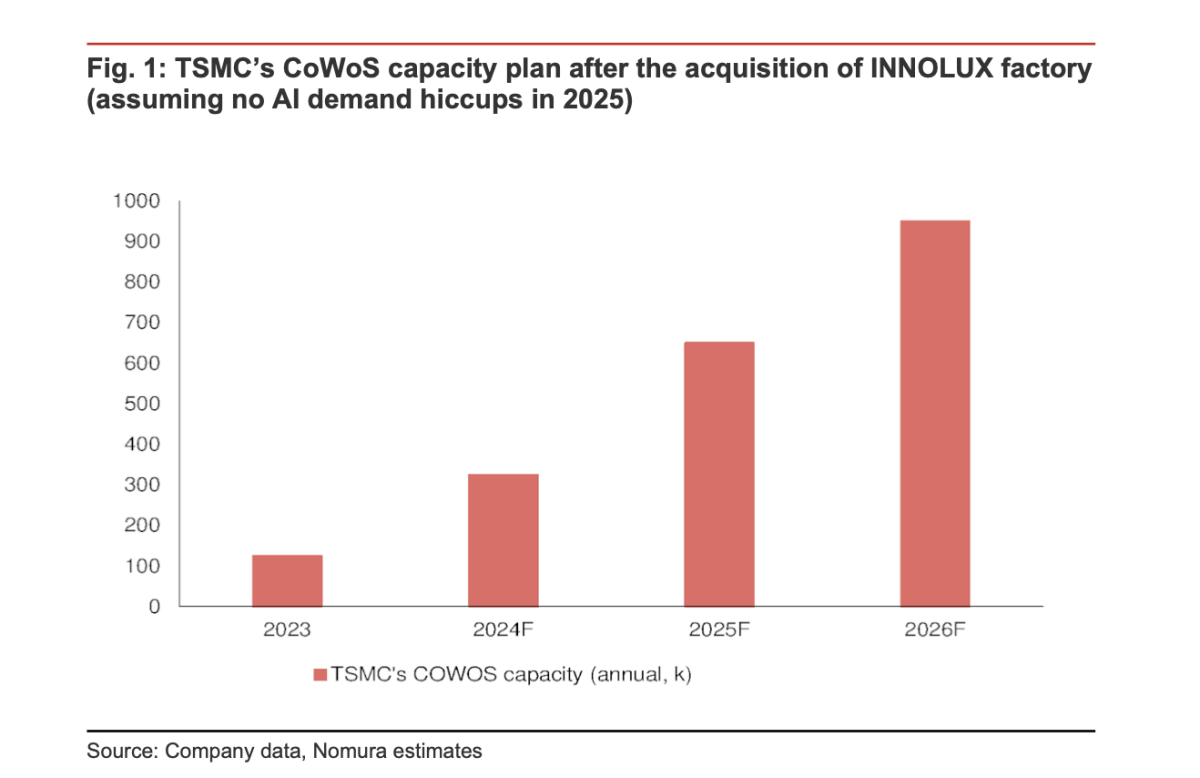

As for CoWoS, Nomura currently expects that taiwan semiconductor's CoWoS capacity will reach 90-100 thousand wafers per month by the end of 2026. The institution anticipates that taiwan semiconductor will convey a viewpoint that the supply and demand of CoWoS will not be balanced before 2026. However, Nomura still believes that the demand will only be truly understood after the delivery of nvidia's GB200 (around the second quarter of 2025).