10月10日,中国人民银行公告称,正式创设“证券、基金、保险公司互换便利(SFISF)”,首期操作规模5000亿元,即日起接受申报。

10月10日,中国人民银行公告称,正式创设“证券、基金、保险公司互换便利(SFISF)”,首期操作规模5000亿元,即日起接受申报。Source: MEGA WAVE

Author: Xiao Luyu

The stock price trend of the insurance sector has benefited from multiple factors. First, because A-share investors have favored assets with high dividends and high dividends this year; second, after the new policy on 9.24 ignited market sentiment, the sector's beta effect was obvious; third, the stock prices invested by insurance companies are expected to rise in the stock market, thereby enhancing the intrinsic value of insurance companies.

On October 10, the People's Bank of China announced the official establishment of the Securities, Fund, and Insurance Companies Interchange Facility (SFISF), with an initial operation size of 500 billion yuan, accepting applications from today.

On October 10, the People's Bank of China announced the official establishment of the Securities, Fund, and Insurance Companies Interchange Facility (SFISF), with an initial operation size of 500 billion yuan, accepting applications from today.

This policy tool supports eligible securities, funds, and insurance companies to pledge assets such as bonds, stock ETFs, and csi 300 index constituents as collateral, exchanging with high-grade liquid assets such as national debt and central bank bills from the central bank, thereby significantly enhancing the funding and shareholding capabilities of relevant institutions.

Multiple leading insurance companies have expressed their attention to this news and are preparing for related matters. For example,$CPIC (02601.HK)$Chief Investment Officer Su Gang stated that the company will combine its own investment strategy to conduct in-depth research on the application scenarios of the 'interchange facility' business, fully leveraging the role of long-term funds and patient capital in the capital markets.

PICC Asset Management believes that the establishment of swap convenience tools is not only of great significance for promoting the healthy development of the capital markets, but also provides a new tool for optimizing the asset-liability structure of insurance funds and improving the efficiency of fund utilization. The company will enhance its political position and carry out the implementation of swap convenience tools.

Due to the lack of experience in using swap convenience tools by domestic insurance funds, the actual demand in the short term remains to be seen, and there may not be a clear increase in A-share holdings by insurance funds in the short term.

This still means that insurance funds will become one of the most important long-term funds in China's capital market, and the performance of insurance companies will have a closer connection with their investment capabilities.

In other words, as an industry, the insurance sector is ready to move away from the bottom range.

Bullish

The current insurance sector is benefiting from multiple factors.

Every bull market has shining performances of insurance stocks. However, even before the market started on September 24, this year's insurance sector had already shown significant strength. The sector index rose from around 1015.13 in August to near 1400 points, with an interval increase of over 40%.

Compared to the sector's bottom of around 776 points in 2022, the current insurance sector index has doubled, and it seems to be only a step away from the historical high of 1845.42 points in 2018.

The stock price trend of the insurance sector benefits from multiple factors. One is that since the beginning of this year, A-share investors prefer assets with high dividends and high profits, and insurance companies with strong profitability and good cash flow typically have stable dividend policies and the ability to actually pay dividends.

In 2020 so far,$PING AN (02318.HK)$the total amount of cash dividends paid annually exceeds 20 billion yuan, with a dividend per share exceeding 2.1 yuan, a dividend yield of about 4.2%, $CPIC (02601.HK)$ the total amount of cash dividends paid annually exceeds 6.8 billion yuan, with a dividend per share exceeding 1 yuan, a dividend yield of about 2.74%.

Compared with the dividend yield of around 4.7% for the four major banks, the top insurance companies also have decent dividend payout.

Secondly, after the 9.24 new policies sparked market sentiment, the sector's beta effect was obvious. In historical bull markets, insurance stocks often perform well in the early stages. With the overall market rising, the funds flowing into the stock market are abundant enough, and insurance stocks, as blue chips and defensive stocks, usually attract the favor of many funders.

Looking back at the two bull markets, the insurance industry saw improvements in fundamentals, premium income, and investment gains in 2007. However, in 2008, affected by the economic environment, the overall industry performance was poor, and stock prices experienced a process of rapid rise followed by a sharp decline.

The period of 2014-2015 was a standout period for insurance stocks, as they benefited from favorable policies, improved market conditions, and sustained improvement in industry fundamentals, resulting in excellent overall performance.During this period, stock prices rose by 77.71%. $PING AN (02318.HK)$ Throughout this period, the stock price of insurance stocks increased by 77.71%.$Hubei Biocause Pharmaceutical (000627.SZ)$The stock price increase range exceeded 310%.

After this bull market cycle, the insurance sector continued its upward trend, with better stability in returns compared to many A-share sectors, only testing historical low-range levels after 2021.

Considering that insurance companies heavily relied on agent sales channels that were unable to operate normally at the time, the industry also faced a painful transition period from traditional "quantity battle" to high-quality development, along with regulatory policy changes, increased claims, and other practical difficulties. It is not surprising to see this kind of bottoming range.

Starting from the end of 2023, the industry gradually overcame the adverse effects of the transformation pains and the related stock prices also showed obvious strength after consolidation.

Thirdly, the stock prices of insurance company investments are expected to rise in the stock market, thus increasing the intrinsic value of insurance companies.

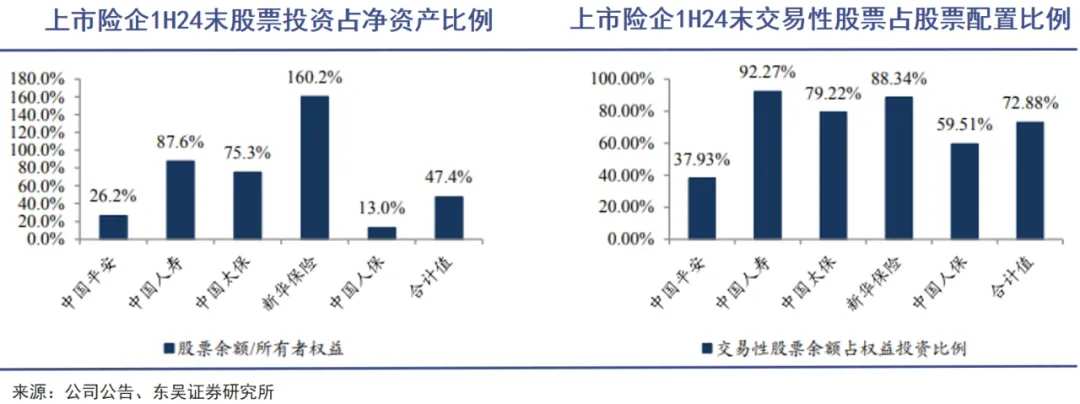

According to the 2024 interim report information, the stock balance/owner's equity ratios of leading listed insurance companies are respectively$NCI (01336.HK)$160%、$CHINA LIFE (02628.HK)$88%、 $CPIC (02601.HK)$ 75%、 $PING AN (02318.HK)$ 26%、 $PICC GROUP (01339.HK)$ 13%。

If the equity market continues to rise in the future, the performance flexibility of these insurance companies will be further unleashed. HTSC predicts that the impact of stock market rise on the embedded value of life insurance companies in the third quarter of this year may reach 2%-5%.

Of course, beyond the stock market situation, the continuous operational capability of insurance companies is even more important.

Risk reduction

The value of insurance policies is increasing in a low interest rate environment.

Regardless of the ultimate direction of this stock market cycle and whether the central bank can perfectly achieve its goal of regulating bond interest rates, it is certain that the Chinese economy will face a long period of low interest rates in the future, leading to increased operational pressures for many industries and companies.

In fact, over the past two decades, the central core of domestic long-term interest rates has been trending downwards, but this year the long-term interest rates are under more significant pressure, dropping below 2.3% at one point. The decline in interest rates will lead to a contraction in interest rate spreads, which is currently the highest proportion of income sources for domestic insurance companies.

Therefore, in 2023, due to the impact of declining interest rates and stock market fluctuations, the net income of insurance companies has generally decreased, with the total industry net income at 181.7 billion yuan, a year-on-year decrease of 17.2%. Among them, the net income of life insurance companies has experienced an even higher year-on-year decline, reaching 18.7%.

Fortunately, regulatory authorities have promptly recognized the issue of interest rate spread risk and have issued a series of policies to adjust the guaranteed interest rates of life insurance products in order to reduce the liabilities cost for insurance companies.

Starting from September 1, 2024, the upper limit of the guaranteed interest rate for ordinary insurance products will be lowered to 2.5%, and the related reserve assessment interest rate will be set at 2.5%. Starting from October 1, 2024, the upper limit of the guaranteed interest rate for dividend-type insurance products will be lowered to 2.0%, and the minimum guaranteed interest rate for universal life insurance products will be lowered to 1.5%.

Although the upper limit of the guaranteed interest rate has been lowered, the returns on savings-type insurance policies still seem somewhat attractive compared to the 30-year national bond yield of 2.35% and the less than 2.0% interest rate on bank medium to long-term deposits, and are also easier to purchase compared to scarce large-denomination deposits.

In fact, during the window period before the interest rate switch and the suspension of old products, the performance of many life insurance companies has surged. From January to August this year, the five listed insurance companies raked in premiums totaling 2,165.53 billion yuan, an increase of 5.63% year-on-year, with a total premium income of 212.996 billion yuan in August alone, representing a significant increase of 30.3% year-on-year.

It can be seen that under the rigid demand for savings of Chinese residents, additional life insurance, dividend insurance and other types still have high sales heat and considerable market space, which can continue to contribute to the revenue and profit of insurance companies.

At the mid-year performance conference in 2024, the management of many listed insurance companies also stated that they will focus on dividend insurance with the characteristic of 'guaranteed + floating' returns in the future, because this will help the company better cope with the downward cycle of interest rates, the pressure on asset allocation, investment income fluctuations, and reduce the risk of interest rate spread loss.

However, the most crucial factor affecting the operational risk of the insurance industry is whether the real estate industry can stabilize and no longer undermine everyone's confidence in the insurance industry. Although the proportion of real estate investment by most insurance companies is not high, the market is more concerned about the devaluation of these assets.

At the press conference of the State Council Information Office on October 12th, the Ministry of Finance announced a series of incremental policies for the real estate market, including allowing special bonds to be used for land reserves, supporting the acquisition of existing houses, optimizing the supply of affordable housing, and optimizing related tax policies, to help stabilize the real estate market.

If the real estate market gradually improves marginally under policy influence, the pressure of asset devaluation and investment risk for insurance companies may also be alleviated, and the suppression of the insurance sector market by real estate risk exposure will also be reduced.

Stability to preserve value

How to understand and practice the phrase 'invest for the long term'.

In the past, many people did not value the profit rate of insurance products, nor liked the fact that insurance products have a longer maturity period than general financial products. They were more interested in making some quick profits, quick trades, flexible and agile money, or seeing real estate investment as the best and only channel for wealth inheritance.

However, in the situation of plummeting house prices, real estate companies going bankrupt, and continuous bear markets, it was actually the insurance industry that withstood this wave of risks, and continued to thicken its profits through investing in fixed income and equity products, fulfilling commitments to customers.

As mentioned in the "Opinions on Strengthening Supervision, Preventing Risks, and Promoting the High-Quality Development of the Insurance Industry" issued by the State Council, the insurance industry plays the role of an "economic shock absorber" and "social stabilizer".

Insurance companies not only help enterprises and individuals diversify and transfer various risks encountered in economic activities by providing claims and compensation, but also help residents solve retirement issues through providing returns and services, further improving the social security system.

The role of insurance funds as a shock absorber and stabilizer for the stock market is expected to be enhanced with the introduction of convenient tools for swaps. Even without this incremental capital, as of the end of June this year, the amount invested by insurance funds in stocks and securities investment funds has exceeded 6 trillion yuan, highlighting their importance in the equity market.

Furthermore, due to their characteristic of seeking long-term stable returns, insurance funds can maintain a relatively stable investment strategy, reduce short-term speculative activities, and help stabilize stock market fluctuations.

For A-shares that need to increase the proportion of institutional investors to strengthen the long-term investment behavior and market inherent stability, insurance funds are undoubtedly valuable buyers to strive for. This is also an important reason for the joint issuance of the "Guiding Opinions on Promoting the Entry of Medium and Long-Term Funds into the Market" by the Central Financial Office and the China Securities Regulatory Commission.

By referencing the participation rate of over 90% institutional investors in US stocks and the Nikkei, it can be understood that as the Chinese investment market matures, it becomes increasingly unsuitable for retail investors to participate directly. If we were to make a comparison, the probability is high that insurance companies have better stock trading capabilities than individual investors, and they also do not cause such drastic market fluctuations.

It is believed that the recent trend of A-shares after the National Day has caused many people who wanted to make quick money to suffer losses. Therefore, for investors, especially those with poor investment abilities and those who are stuck with fund investments, it may be a better choice to indirectly invest in the equity market through insurance products and gain a relatively stable guaranteed return.

By stepping out of the traditional framework of "getting compensation in case of accidents," and looking at the function of insurance more from the perspective of personal retirement needs, family asset allocation, preservation, and inheritance, one will realize that insurance and investment have always been complementary.

Editor/Rocky