As the outlook for the Fed rate cut path becomes increasingly uncertain, bond investors are now starting to take defensive measures. Last week, higher-than-expected US CPI and mixed labor market indicators caused traders to further reduce bets on the extent of Fed rate cuts this year, while also pushing the 10-year US Treasury yield to its highest level since July.

As the outlook for the Fed's rate cuts becomes increasingly uncertain, bond investors are now also starting to take defensive measures.

Last week, higher-than-expected US CPI and mixed labor market indicators caused traders to further reduce bets on the extent of Fed rate cuts this year, while also pushing the 10-year US Treasury yield to its highest level since July.

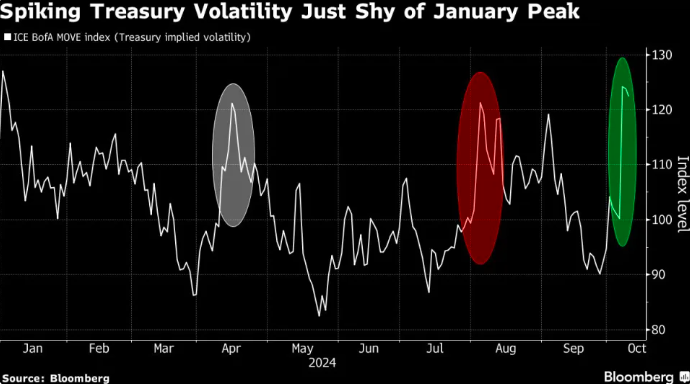

The Merrill Lynch MOVE index, a closely watched measure of expected volatility in US Treasuries, rose to its highest level since January.

The Merrill Lynch MOVE index, a closely watched measure of expected volatility in US Treasuries, rose to its highest level since January.

Interest rate market traders currently estimate that the probability of the Fed maintaining rates at November or December meetings is about 20%. For comparison, before the release of the September non-farm payrolls report, a 50 basis point rate cut over two meetings was once considered a certainty within the industry.

Meanwhile, activity in derivatives markets such as options indicates that investors are hedging against the decreasing number of Fed rate cuts: a significant demand for secured overnight financing rate (SOFR) options has emerged recently, focusing on contracts speculating that the Fed will only cut rates once more this year. Some extreme bets even anticipate the Fed pausing its easing cycle early next year.

In the past week, US Treasury prices have seen a sharp decline. The Bloomberg US Bond Index has weakened for the fourth consecutive week, marking the largest drop since April. The 10-year Treasury yield has risen above the 4% threshold, while the 30-year Treasury yield hit 4.42%, reaching its highest level since July 30th.

In last Friday's mmf options trading, there were several noteworthy put options trades, attempting to bet on a steeper yield curve. One target of a put option on the 10-year Treasury was for the yield to rise to around 4.5% before the expiry on November 22, while several bulk trades hoped to touch around 4.75% by then.

Kit Juckes of ubs group in Paris, France, wrote in a report: "The market seems uncertain about the outcomes of the next few Federal Reserve decisions. The rapid rise of nearly 50 basis points in the 10-year Treasury yield since mid-September indicates increasing market confidence that the U.S. economy will not experience a 'hard landing.' This suggests an equal likelihood of 'no landing' as 'soft landing,' raising concerns that inflation risks may reappear if fiscal tightening measures do not materialize."

Considerations for investment allocation

In this context, many industry professionals seem to struggle with deciding whether to deploy cash in the short end or long end of the world's largest bond market. This has made the relatively less risky intermediate curve segment a safe haven in the eyes of some investors.

To mitigate vulnerabilities under economic recovery, potential fiscal shocks, or turbulence related to the U.S. election, asset management giants like blackrock, PIMCO, and ubs group's Global Wealth Management currently advocate buying five-year bonds. Compared to similar bonds with shorter or longer maturities, five-year bonds are less sensitive to such risks.

Solita Marcelli, Chief Investment Officer for the Americas at ubs group Global Wealth Management, recommends investing in mid-term bonds, such as around five-year government bonds and investment-grade corporate bonds. Marcelli states, "We continue to recommend that investors prepare for a low-interest rate environment, reallocating excess cash, money market positions, and maturing fixed deposits into assets that offer more sustainable income."

The U.S. bond market will be closed on Monday for Columbus Day. However, in the coming weeks, the bond market is likely to see significant volatility – not only related to the U.S. election.

Due to investors awaiting quarterly bond issuance data from the U.S. Treasury (expected to remain stable), the next monthly non-farm payrolls report, and the Federal Reserve's rate decision on November 7th, some industry insiders anticipate that the market's sharp fluctuations may continue for several weeks.

Citadel Securities is warning clients to prepare for the so-called "major future volatility" in the bond market. The company predicts that the Federal Reserve will only cut interest rates by another 25 basis points in 2024.

Blackrock's fundamental fixed income portfolio manager David Rogal also stated, "As the election enters the options game window, implied volatility will rise." the company favors intermediate-term government bonds because it believes that as long as inflation cools down, the Fed will readjust the policy cycle, pushing policy rates from 5% to between 3.5% and 4%.

Of course, with the anchor known as the "global asset pricing" returning to around 4.1% high, the current round of bond market selling is also causing some long-term investors to believe that the "buying zone" has arrived.

Roger Hallam, Global Rates Director of Vanguard Group, said in an interview, "Our core belief is that due to the Fed's policy remaining restrictive, next year's economy will indeed slow down. This means that for the company, when the 10-year yield exceeds 4%, there will be an opportunity to start extending the duration of our portfolio, while taking into account the downward growth trend next year.

He added that this will gradually shift the company's focus more towards bonds.

Editor/Rocky