而如今美股屡创新高之际,这种对冲热潮却正在各种资产上创造出不同寻常的轮廓。在其中一个例子中,美国股票和国债市场的波动性衡量指数刚刚限制了今年股债市场两次较大规模的周涨幅。上涨使得两个市场的波动性恐惧指标都达到了20多年来的最高水平——尤其是与标普500指数创下历史新高的其他时期相比,意味着交易员们对于接下来股债行情的相对谨慎立场,并且推动一些交易员采取对冲措施应对可能即将来临的下跌。

而如今美股屡创新高之际,这种对冲热潮却正在各种资产上创造出不同寻常的轮廓。在其中一个例子中,美国股票和国债市场的波动性衡量指数刚刚限制了今年股债市场两次较大规模的周涨幅。上涨使得两个市场的波动性恐惧指标都达到了20多年来的最高水平——尤其是与标普500指数创下历史新高的其他时期相比,意味着交易员们对于接下来股债行情的相对谨慎立场,并且推动一些交易员采取对冲措施应对可能即将来临的下跌。Stock market continues to set records, risk premiums remain tight, while cross-asset volatility indicators hover near the highs since the beginning of the year.

Take a snapshot of the American financial market now, presenting an incredibly healthy picture: the stock market continues to hit historic highs, corporate bond prices show no signs of concern, and commodities remain actively traded globally amid optimistic economic sentiment. However, if a 'director' focusing on the market delves deeper into the market, the outlook will quickly become unclear. In addition to all the external optimism, volatility measurement indicators tending to expand are equally important topics across almost all asset classes.

For example, in the sharp downturn of the market in August and September, when trading in stocks and bonds became unfavorable, Wall Street traders were caught off guard and rushed into the hedge markets—driving hedge costs and volatility measurement indicators to rise almost as fast as the market itself.

As the US stock market repeatedly hits new highs, this hedging frenzy is creating unusual contours on various assets. In one example, the volatility measurement indexes of American stocks and government bond markets have just capped the weekly rises in the stock and bond markets this year. The rise has pushed the volatility fear indexes of the two markets to their highest levels in over 20 years—especially when compared to other periods when the S&P 500 index hit historic highs, indicating traders' relatively cautious stance on the upcoming stock and bond market trends, and prompting some traders to take hedging measures to counter the possible upcoming downturn.

As the US stock market repeatedly hits new highs, this hedging frenzy is creating unusual contours on various assets. In one example, the volatility measurement indexes of American stocks and government bond markets have just capped the weekly rises in the stock and bond markets this year. The rise has pushed the volatility fear indexes of the two markets to their highest levels in over 20 years—especially when compared to other periods when the S&P 500 index hit historic highs, indicating traders' relatively cautious stance on the upcoming stock and bond market trends, and prompting some traders to take hedging measures to counter the possible upcoming downturn.

In summary, due to the uncertainty of the upcoming US presidential election, the Federal Reserve's policy trajectory influenced by economic data, and recent financial market trauma making traders more cautious, some investment institutions on Wall Street are still highly concerned about the future stock and bond market trends.

Amy Wu Silverman, Director of Derivatives Strategy at RBC Capital Markets, said: 'I have to say that the likelihood of some low-probability, very bad events occurring is increasing.' 'After the VIX index soared due to the yen's unwinding turmoil in August, the US stock market has returned to normal and hit new highs. However, the potential sentiment of concern remains high.'

Although cross-asset prices, including stocks and bonds, often rise when investors are anxious, the current situation is particularly extreme, with both bullish and bearish sentiments equally evident, each accounting for about 50%. The US benchmark index—the S&P 500 index has risen for five consecutive weeks, closing with weekly gains in eight of the past nine weeks, especially as JPMorgan and Wells Fargo kicked off a new round of US earnings season, and their performance exceeded market expectations. Closing at the 45th historical high this year on Friday, the S&P 500 index reached an intraday record high of 5822.13. In the bond market, the US investment-grade bond spread hit its smallest level in over three years.

Rare trend chart: During the bull market in US stocks, the VIX index also rose.

However, due to the shadow cast by the sharp drop in global financial markets in early August and September, indicators measuring the nervousness of investors are showing cautious readings, which is very rare in the stock market bull market period.

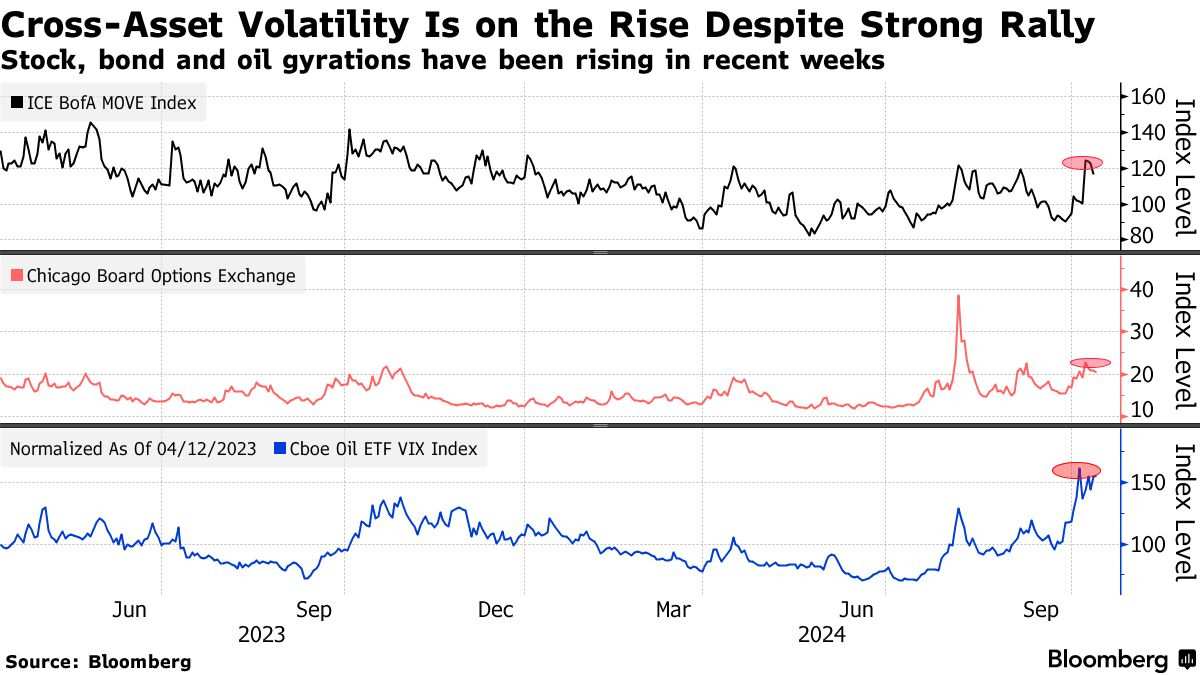

Statistical data shows that since the beginning of this month, stock market panic indicators—the Chicago Options Exchange Volatility Index (VIX Index) and the US bond market panic indicator—Intercontinental Exchange Bank of America MOVE Index (ICE BofA MOVE) have both risen significantly. The global cross-asset risk index compiled by Bank of America Corp. reached the second highest level of the year, second only to the scale of the market sell-off in early August, which wiped out trillions of dollars of global stock value in a few days. The index tracks pressure in global stocks, interest rates, currencies, and commodity markets, and measures the implied future price volatility of options.

In other words, although the US stock and bond markets are calm now, the past shock effects and uncertain future prospects are seriously affecting investors' sentiments, and a significant amount of funds are already prepared for a decline in the US stock market.

Traders who were shocked by the chaos of the summer are dealing with the stalemate in the US presidential election, local wars in the Middle East, and the still expanding US economy. However, whether the US economy can successfully achieve a 'soft landing' continues to raise market doubts, such as this week's unemployment claims data, which exceeded expectations for the first time in recent weeks.

At the same time, more and more investors believe that the Federal Reserve led by Chair Powell may not be inclined to immediately inject new vitality into the US economy. Data released on Thursday showed that consumer inflation was higher than expected, and last week's US employment report surged, causing traders to reduce their bets on a 50-basis-point rate cut in 2024. Raphael Bostic, the Atlanta Fed president with FOMC voting rights this year, even said he would be willing to skip another rate cut next month.

"There's almost a sense of distrust in the market," said Peter P. Cheer, head of macro strategy at Academy Securities. "There have been some big moves overnight. Investors do have a lot of concerns, but overall the stock market is on an upward trend. We've also experienced several rapid declines during this period."

"The air forces" are getting ready to make a comeback.

After investors have driven a simultaneous rise for five consecutive months, the "air forces" of bonds and stocks, that is, short positions, also show clear signs of rebuilding. According to IHS Markit data, bets against the SPDR S&P 500 ETF Trust (i.e. the S&P 500 Index ETF) have reached 2.4% of its outstanding shares, higher than the four-year low of 1.6% earlier this month. Similarly, the short interest ratio of the iShares 20+ Year Treasury Bond ETF hit a new low in August for 15 months, but has now risen to over 1%.

Option market statistics show that as the U.S. stock market continues its bull market trend, investors' demand for hedging protection against a big drop in the U.S. stock market is growing stronger, reaching rare levels of tail risk hedging measures seen in the past two years. The MOVE index tracking bond market volatility has surged to its highest level since January, while a similar indicator in the crude oil market has soared to levels not seen in two years. Since August, the implied volatility of the iShares iBoxx Investment Grade Corporate Bond ETF has increased relative to actual price fluctuations, which is the latest sign that traders are buying insurance against losses.

In the past month, the yield on the 10-year U.S. Treasury bond has risen by more than 40 basis points, while the S&P 500 Index has risen by about 3% under the pressure of rising U.S. bond yields. This is an unprecedented rebound since April 2022 - with the 10-year U.S. Treasury yield moving in the same direction as U.S. stocks, typically during a period of rising U.S. stocks, the U.S. Treasury yield falls or moves sideways.

Erika Maasmeier, Portfolio Manager at Columbia Threadneedle Investments, said: "Despite some macro and micro-level risks, the market has been very strong. As we approach the peak of the election season and the next Fed rate decision, we wouldn't be surprised to see a pullback."

In addition to the U.S. presidential election and Fed monetary policy, the earnings season is also the next major test facing the market, with the overall price-to-earnings ratio of the S&P 500 Index reaching its highest level since 2021. While Wall Street analysts expect overall profits to grow by 4% in the third quarter, the slowest growth in a year, investors remain very focused on earnings reports, especially those of the seven major U.S. tech giants with a high weighting in the S&P 500 Index. Data compiled by Bloomberg Intelligence shows that Wall Street analysts generally expect next year's overall profit growth of S&P 500 component companies to accelerate, potentially reaching 14%.

"Investors have shown extreme optimism, despite the very high valuations," said Michael Orrock, Chief Market Strategist at JonesTrading. "Strong economic data, coupled with the Fed FOMC's aggressive loose stance in the past month, has fueled investors' overconfidence."

Editor/new