Helen of Troy Limited (NASDAQ:HELE) shares have had a really impressive month, gaining 34% after a shaky period beforehand. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 34% in the last twelve months.

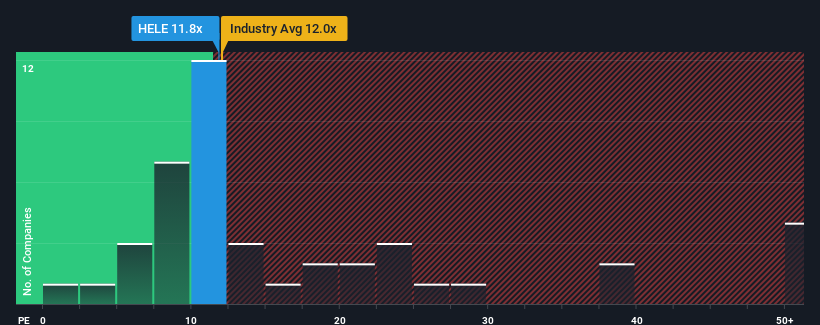

In spite of the firm bounce in price, Helen of Troy may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 11.8x, since almost half of all companies in the United States have P/E ratios greater than 19x and even P/E's higher than 35x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Helen of Troy certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Is There Any Growth For Helen of Troy?

There's an inherent assumption that a company should underperform the market for P/E ratios like Helen of Troy's to be considered reasonable.

There's an inherent assumption that a company should underperform the market for P/E ratios like Helen of Troy's to be considered reasonable.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 5.2% last year. Ultimately though, it couldn't turn around the poor performance of the prior period, with EPS shrinking 29% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 6.0% each year during the coming three years according to the six analysts following the company. Meanwhile, the rest of the market is forecast to expand by 10% per annum, which is noticeably more attractive.

In light of this, it's understandable that Helen of Troy's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What We Can Learn From Helen of Troy's P/E?

Helen of Troy's stock might have been given a solid boost, but its P/E certainly hasn't reached any great heights. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Helen of Troy's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for Helen of Troy that you should be aware of.

If you're unsure about the strength of Helen of Troy's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.