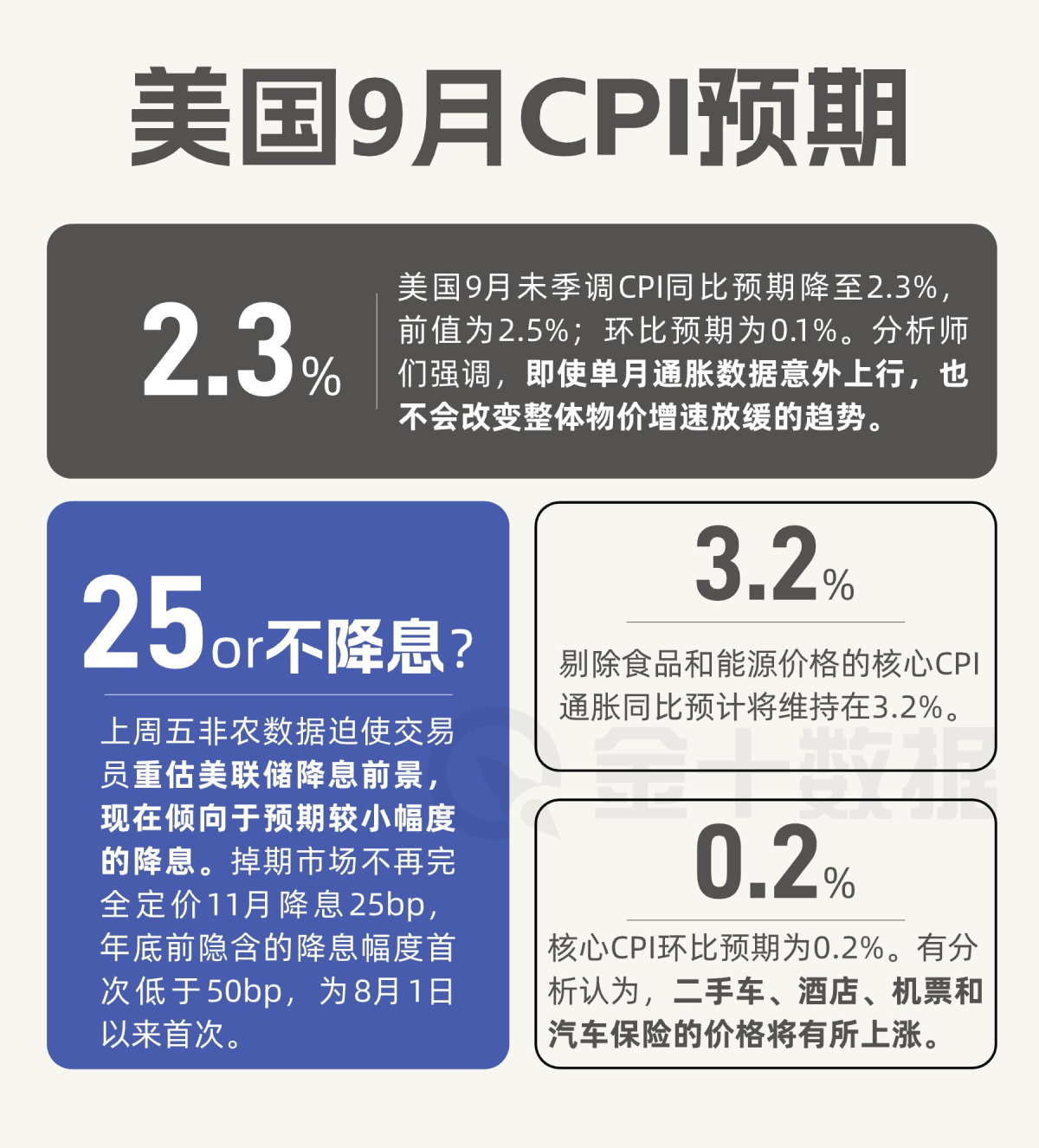

根据FactSet的共识预期,经济学家预计9月的CPI环比上涨0.1%,而8月的前值为上涨0.2%。这将使整体通胀同比从8月份的2.5%下降至2.3%。排除波动较大的食品和能源价格后,

根据FactSet的共识预期,经济学家预计9月的CPI环比上涨0.1%,而8月的前值为上涨0.2%。这将使整体通胀同比从8月份的2.5%下降至2.3%。排除波动较大的食品和能源价格后,This is the most significant inflation data before the November meeting of the Federal Reserve, and also the last CPI report before the 2024 USA presidential election.

The usa will release the September CPI inflation data on Thursday, October 10th at 8:30 pm. This is the most significant inflation data before the Fed's November meeting and also the last CPI report before the 2024 U.S. presidential election. Market forecasts indicate that the overall inflation level in the U.S. for September will continue to show modest performance, mainly benefiting from the decline in energy prices.

With inflation pressure easing and signs of cooling in the labor market, the Fed began cutting interest rates in September, with an unexpected 50 basis point cut. Analysts believe that even if the inflation data for September continues to improve, it is unlikely to significantly alter the Fed's policy path in the long term, but they warn that risks still exist in the inflation outlook. "It seems that the Fed is very satisfied with the current level of inflation and its trend," said Josh Hirt, Senior U.S. Economist at Vanguard Group, "But we remain cautious, especially in the services sector."

According to FactSet's consensus expectations, economists expect a 0.1% month-on-month increase in CPI for September, with a previous value of 0.2% in August. This will bring the overall inflation year-on-year down from 2.5% in August to 2.3%. Excluding volatile food and energy prices, core inflation is expected to be slightly higher, due to price increases in used cars, hotels, airfares, and auto insurance. Core inflation in September is expected to increase by 0.2% month-on-month and 3.2% year-on-year.

According to FactSet's consensus expectations, economists expect a 0.1% month-on-month increase in CPI for September, with a previous value of 0.2% in August. This will bring the overall inflation year-on-year down from 2.5% in August to 2.3%. Excluding volatile food and energy prices, core inflation is expected to be slightly higher, due to price increases in used cars, hotels, airfares, and auto insurance. Core inflation in September is expected to increase by 0.2% month-on-month and 3.2% year-on-year.

However, analysts emphasize that the unexpected upward trend in monthly inflation data will not change the overall trend of slowing price pressures. Economists at UBS Group wrote last week:

"While we expect core CPI in September to be slightly higher than in recent months, this does not change our expectation of further easing in mid-term inflation."

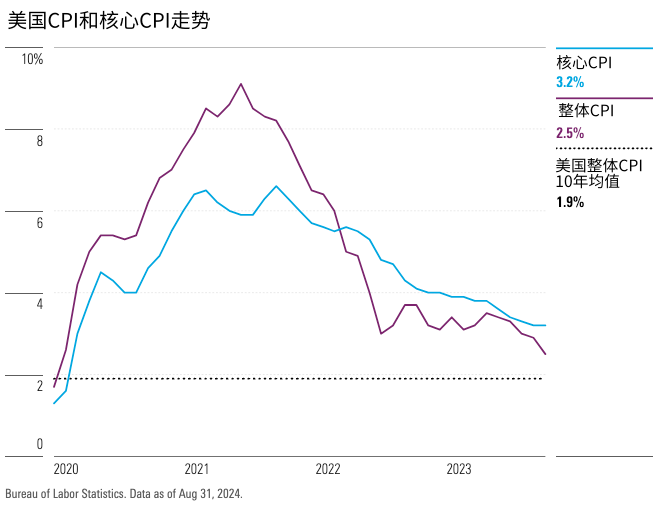

Overall CPI and core CPI.

The CPI data released this Thursday closely follows last week's better-than-expected non-farm payroll report. The report indicates that the US economy added 254,000 jobs last month, significantly exceeding expectations. Combined with the upward revision of data from the previous months, it alleviated investors' concerns about economic slowdown.

"The data we received last Friday was much stronger than expected. The data from the previous months was revised upward, and importantly, the unemployment rate further decreased," explained Brian Rose, Senior US Economist at UBS Global Wealth Management.

"Now, the issue of rising unemployment is no longer as concerning, and the risks in the labor market are not as high as before."

According to Hirt, strong employment data means that inflation will once again become a focus of attention for investors and policymakers. "We do see more attention turning back to inflation." Economists at Vanguard Group expect core inflation to rise by 0.24% month-on-month, with overall inflation rising by 0.10% month-on-month. Senior US Economist at Vanguard Group, Hirt, stated that while these numbers are a step in the right direction, core inflation still remains slightly elevated.

Service sector inflation risks and rate cut expectations.

Hirt pays special attention to inflation risks from the service sector, primarily due to strong wage growth. He noted that the wage growth in the service sector is "still high," which is not entirely consistent with the 2% inflation target.

The analyst at Bank of America also pointed out that rising oil prices and increased shipping costs bring risks, which could push inflation up in the short term. Housing costs remain high, also one of the main drivers of inflation.

The impressive job report in September significantly changed investors' expectations for the Fed's November meeting. The market previously expected a 50 basis point rate cut, but now tends towards a smaller cut. According to the cme FedWatch Tool, bond market prices indicate an 88% probability of a 25 basis point rate cut in November.

Rose, a senior US economist at UBS Group, believes that if inflation data is stronger than expected, it may prompt the Fed to pause rate cuts in November, especially if concerns remain about whether inflation will return to the target range. He stated: "This weakens the argument for 'we must cut rates quickly' because the downward risks in the labor market or unemployment rate no longer seem so terrifying." With the improvement in the labor market conditions, inflation data 'becomes important again.'

He believes that the core inflation on a month-on-month basis will range from 0.2% to 0.3%, which the Fed would find satisfactory. However, if it exceeds 0.4%, it could trigger more serious concerns and increase the possibility of the Fed maintaining interest rates in November.

Editor/Rocky