以色列与伊朗的冲突以及中国经济刺激计划的推出推动布伦特原油上周创下一年多来最大的五个交易日涨幅。本周一,油价曾一度升至每桶80美元以上,但周二又一泻千里,下跌了5%。

以色列与伊朗的冲突以及中国经济刺激计划的推出推动布伦特原油上周创下一年多来最大的五个交易日涨幅。本周一,油价曾一度升至每桶80美元以上,但周二又一泻千里,下跌了5%。Everyone is speculating about the timing of the next market turnaround. In fact, these instigators are not so concerned about the future of OPEC or the Middle East.

"Geopolitical risk premium" is a vague concept, which roughly corresponds to trading about 6 billion barrels of "virtual" oil per day in today's oil market, this premium causes the price of oil to be $5 higher per barrel.

Global consumption of (only) 0.1 billion barrels of oil per day indicates that the oil market is controlled by speculators. This also explains why oil prices have been so volatile in the past few weeks.

The conflict between Israel and Iran and the launch of China's economic stimulus plan drove Brent crude oil to its largest five-day trading gain in over a year last week. On Monday, oil prices once rose to over $80 per barrel, but on Tuesday they fell by 5%.

The conflict between Israel and Iran and the launch of China's economic stimulus plan drove Brent crude oil to its largest five-day trading gain in over a year last week. On Monday, oil prices once rose to over $80 per barrel, but on Tuesday they fell by 5%.

jpmorgan commodity futures and Options strategy.Analyst Tom Skingsley from JPMorgan wrote in a client memo that the initial rebound was "largely caused by (reasonable) risk premiums", but he added that investors' "positions" were also an important factor.

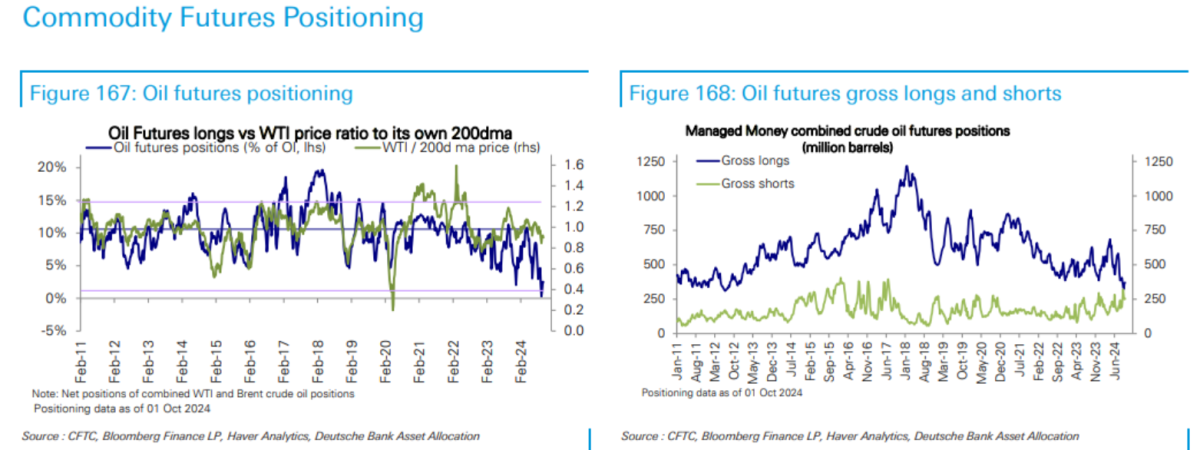

Perhaps the biggest news in the oil market in the past few months is the algorithmic selling reaching historical extremes.

Speculative trend-following hedge funds (also known as commodity trading advisors, CTA) have recently had the largest net short positions. These funds analyze complex technical factors such as the term structure of Brent crude oil and WTI crude oil prices, rather than fundamental factors such as macroeconomics or geopolitics.

Ryan Fitzmaurice, Marex's commodity investment portfolio manager and strategist, told FTAV: "CTAs are the dominant force this year. Historically, there has been a lot of sticky money in the oil market, coming from passive long positions by index managers and those seeking inflation hedging. However, a large amount of sticky money left the market in April and May."

Due to OPEC's preparation to increase supply in December and global soft demand, Brent crude oil prices fell from above $90 per barrel in mid-April to below $70 in mid-September. Trend followers actively buy when prices rise and sell when prices fall, accelerating the selling pressure.

Subsequently, China's preliminary fiscal plans and escalating tensions between Israel and Iran caused a dramatic upheaval in the market. Free investors who had been sitting on the sidelines for months, eager to hedge a broader investment portfolio, began buying oil futures and call options, breaking the negative momentum that was driving CTA selling.

Former President of Koch Global Partners, Ilia Bouchouev, explained that the shift in sentiment is not profound, but it is sufficient. Bouchouev said:

"Free investors are now turning bullish, but they are not really looking to buy. Before the U.S. elections, they have no incentive to buy. If Trump wins, we will face tariffs, which would be an additional risk. Since they can do the same thing on November 6th, why invest now?"

A month ago, producers bought a large number of put options, forcing traders to sell futures to hedge this risk. However, a few weeks ago, as retail investors suddenly bought a large number of call options through ETFs like the United States Oil Fund (USO) and macro hedging tools, this bearish trend gradually weakened and started moving in another direction.

Given that no one really knows what will happen in the Middle East, people actively buy call options for $100 as a form of insurance. What people know is that if oil prices really rise to $100, the Fed's plans will derail, and other assets will also be greatly affected.

Bouchouev added, "The biggest short" - momentum-driven CTAs are mechanically forced to cover their positions.

"Historically, their positions often reverse. So, if they are already at an extreme, there is no way other than to turn around. CTA has covered 10% now, so there is still 90%. The problem with CTAs is... if the momentum is negative, they will continue to sell. But if the market stabilizes for about a week, or there is a small peak, suddenly this negative momentum will be broken. The momentum does not necessarily have to turn positive, just not too negative for CTAs to start buying back. We do not have a positive momentum yet, but they have already started covering.

However, over the past few days, as concerns about Israel striking Iranian energy facilities have subsided, the market has once again undergone dramatic changes. In a report released by Skingsley of JPMorgan on Tuesday morning, he said:

"Capital flows on the trading floor are showing a polarized trend, with an increasing amount of discretionary funds starting to reduce positions at these levels, or at least profit-taking, while systemic funds continue to unwind significant shorts... Taking this into consideration, what should be the next step?

It remains difficult to determine until Israel takes clear action, but considering the magnitude of the rebound we have seen and the fact that the rebound is almost entirely driven by the (reasonable) risk premium and positioning, if Israel's response is 'disappointing' (does not affect the oil balance/does not target nuclear facilities), then there is now a significant downside potential, a view that did not exist about a week ago, but the risk-return is much greater now...

According to research analyst Martha Dowding and market design expert Jorge Montepeque, some interesting individuals have also joined the selling ranks, all working at Onyx Capital Group, an oil derivatives liquidity provider, who almost certainly made a profit from the recent volatility.

Companies like Trafigura and TotalEnergies have been selling on Tuesday. Exxon has been in a selling position for several months. However, they could switch to buyers at any time. TotalEnergies switches from buyer to seller every few weeks...

On Tuesday, the Austrian group OMV sold a batch of North Sea goods to Total. BP plc sold approximately 0.7 million barrels of oil to Mercuria. OMV is not a typical seller and they usually do not sell publicly, so this is very unusual. Exxon Mobil selling oil for two consecutive months is also very unusual.

Everyone is speculating about the timing of the next market reversal. "It's an endless cycle," Fitzmaurice of Marex said. "CTAs are not necessarily concerned about OPEC or Middle East prospects. They just want to capitalize on the momentum, geopolitics are just another number on the screen."

Editor/ping