Authors: Liu Gang, Li Yujie, Yang Xuanting

Since mid-September, there have been significant changes and reversals in global assets. On one hand, Chinese assets have rebounded rapidly under policy catalysts, with the Hang Seng index accumulating a rise of over 30% since mid-September; on the other hand, after the unconventional large rate cut of 50bp by the Federal Reserve, US bond yields instead climbed back from 3.6% to over 4%.

The seemingly independent performances of Chinese and American assets are intricately linked, reflecting the intertwined "interactions" of the macro cycle: the Federal Reserve's unconventional easing has provided room for China's policy relaxation, as China's financial policies bolstered a rapid market sentiment recovery; however, the substantial rate cut also benefits the US economic recovery, combined with fully priced-in expectations leading US bond yields to rise after hitting rock bottom, potentially constraining further easing space, evident in recent trends of US bond yields, the US dollar, and the Chinese currency.

In this sense, the external easing space may gradually wane at its peak, despite the direct benefits to the export chain from the real estate recovery under US easing; yet, the upcoming election poses a variable (recently seeing a resurgence in Trump's chances of winning), further underscoring the significant importance of fiscal policy for the future trend of the Chinese market.

In this sense, the external easing space may gradually wane at its peak, despite the direct benefits to the export chain from the real estate recovery under US easing; yet, the upcoming election poses a variable (recently seeing a resurgence in Trump's chances of winning), further underscoring the significant importance of fiscal policy for the future trend of the Chinese market.

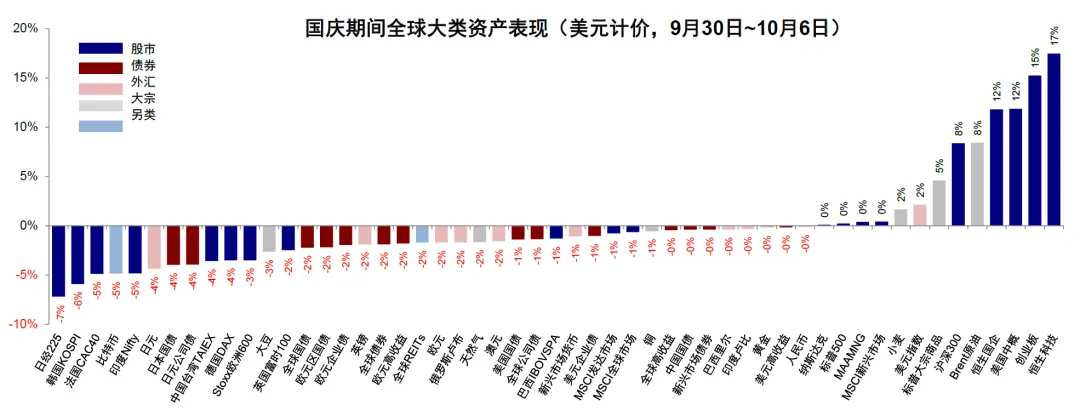

Chart: Performance of global major asset classes during the National Day holiday, with commodities> stocks> bonds, Chinese equity assets and crude oil leading, while the Japanese and Korean stock markets lag behind.

At present, there is a gradual recovery in private credit in the US, while the realization of Chinese policy expectations is more crucial than ever. Therefore, the current crossroads of the Chinese and American cycles show a higher level of certainty at the intersection points of US short-term debt, US real estate chains, Chinese export chains, as well as the Hong Kong growth sectors, all directly benefiting from monetary easing and industry trends. The overall market's broader upward trend requires greater policy support for industrial metals like copper, US manufacturing, and China's pro-cyclical sectors.

Chart: The most clear 'crossing point' is the synergy between short-term debt, real estate, China's export chain, and Hong Kong stocks growth.

China: Under policy catalysts, assets rebound significantly, emotions are relatively full, waiting for subsequent fiscal policy implementation.

In the last week of September, the policies of the three financial departments and the Central Political Bureau meeting exceeded expectations, igniting market sentiment, and causing Chinese assets to rebound significantly. Since mid-September, the Hang Seng Index has surged more than 30%, the Hang Seng Tech Index has risen by over 50%, A-shares have not opened during the holiday, but the previous Shanghai and Shenzhen 300 Index has also risen by 27.2%. This kind of rapid rebound is very remarkable compared to any historical stage. Especially during the National Day holiday when A-shares were closed, and the Hong Kong stock connect was suspended, the Hong Kong stock market maintained a strong momentum. From October 2nd to October 4th, the Hang Seng Index rose by 8%, the Hang Seng Tech Index rose by 10%, leading globally.

The market's response to policies has been so positive, with the core changes being: first, directly encouraging leverage in the private sector through financial policies (stock market and real estate), second, placing more emphasis on people's livelihoods and consumption, conveying signals and ideas that are not completely the same as before. Specific policy measures include:

1) Interest rate and reserve requirement cuts: Decrease interest rates by 20 basis points, October LPR is highly likely to decrease by 20 basis points simultaneously, allowing changes in the point increase magnitude of mortgage interest rates; cut reserve requirement by 50 basis points, provide long-term liquidity of 1 trillion yuan, with a possibility of further reduction by 25-50 basis points in the future.

2) Relaxing real estate policies: Lower the down payment ratio to 15%, lower the threshold for residents' mortgage loans; reduce existing mortgage rates to new issuance levels, with an average decrease of 50 basis points; the Central Political Bureau meeting for the first time clearly stated the target-oriented expression of 'promoting the stabilization of the real estate market', significantly exceeding market expectations.

3) Stable stock market: The central bank has introduced two new structural monetary policy tools to stabilize stock prices.

4) Consumer livelihood: The Politburo meeting's statements on fiscal policy, as well as its tilt towards people's livelihoods and consumption fields, convey a somewhat different perspective and signal than before.

However, after this rapid rise, the market has already factored in a high level of optimism.

1) The relative strength index (14-day RSI) of the Hang Seng Index, which measures the degree of overbought conditions, reached a new high of 90.9 on October 2nd.

2) The short selling ratio, which dropped from a rebound starting at 19.9% in the last week of September to below 14%, shows a characteristic of market pressure.

3) From a valuation perspective, the MSCI Chinese Index's dynamic valuation increased rapidly from a low of 8.6 times on September 11th to 11.7 times, exceeding the historical average of 11 times since 2010. The Hang Seng Index's dynamic P/E ratio also rose from 7.9 times to 10.6 times on October 7th, a new high since January 2023. The current Hang Seng Index risk premium has rapidly fallen from a high of 9.5% on September 11th to around 6%, lower than the historical average since 2010, a new low since January 2023.

Therefore, roughly speaking, the current level of optimism factored in is approaching the peak sentiment of early 2023, with the short-term technical aspects clearly overextended. We in "A New Round of Market Space Under the PolicyCalculating, if the risk premium improves to 6.1% corresponding to the high point after the adjustment of epidemic policies in early 2023, corresponding to around 22,500 for the Hang Seng Index. The market did indeed touch and even exceed this position during the National Day period faster than we expected, but also experienced some pullback due to the policy intensity.

Chart: Hang Seng Index relative strength indicator 14-day RSI reached 90.9 on October 2, hitting a new high.

Chart: Hang Seng Index risk premium quickly fell from the high point of 9.5% on September 11 to 6.0%.

USA: Unconventional rate cuts increase the possibility of a 'soft landing', cooling expectations of recession and rate cuts, waiting for validation from 'hard data'.

Overseas asset trends have also shown a 'turning point,' with declines in both recession and rate cut trades. Since July, the top technology performance of US stocks has been below expectations, macroeconomic data has turned weaker, and the unconventional substantial 50bp rate cut by the Federal Reserve has caused an increase in recession expectations. However, after the Federal Reserve actually cut interest rates, the main theme of US asset trading did not continue to move towards recession and rate cuts, but instead significantly reversed. The 10-year t-note yield rose from a low point of 3.6% on September 17th to 4%; at the same time, the USD rebounded from 100 to around 103; gold fell from $2672 per ounce to $2620 per ounce.

The surface reasons behind these changes are the improvement in economic data in September, while the underlying logic is the downward cost of financing driven by rate cut expectations. In our previous reports, we have consistently emphasized that this rate cut cycle requires 'thinking and doing backwards,' and rate cuts may also be nearing an end when rate cut trades are realized. The Federal Reserve's unconventional rate cut instead increases the possibility of a soft landing.After the rate cut is realized, assets that can solve both the molecular and denominator problems will be better. After the rate cut, assets benefiting from the demand-lifting brought about by the decline in financing costs, and then improving earnings on the molecular end, will have relatively increased relative value. After the rate cut is realized, it may also be the end of the interest rate cut trading, gradually turning to inflation-benefiting assets, such as US stocks and bulk resources such as copper and oil.《Federal Reserve's 'unconventional' rate cuts kick off》). The US t-note yield has shifted to an upward trend after the rate cut, mirroring the experience of 2019.

Chart: Overseas asset trends show a turning point, with reversals in recession and rate cut trades.

On the one hand, the current growth in the USA is not as bad as feared. Looking at the economic leading indicator PMI, the September ISM manufacturing PMI disclosed in early October, although still below the boom-bust line, saw an increase in new orders to 46.1 on a month-on-month basis. The service industry PMI far exceeded market expectations, rising to 54.9, marking the highest value since February 2023, exceeding the boom-bust line for three consecutive months since July. Compared to PMI, employment data is a lagging indicator of the economy, but it has also exceeded expectations across the board. Non-farm payrolls increased by 0.254 million, significantly surpassing the expected 0.15 million, with upward revisions to the July and August data; the unemployment rate decreased from 4.2% to 4.1%; wage increases surpassed expectations on a month-on-month and year-on-year basis, with upward revisions to previous values; the temporary unemployment plaguing employment in the previous two months has essentially disappeared.

Chart: Although the September ISM manufacturing PMI is still below the boom-bust line, there is an improvement in the new orders component, while the service industry PMI far exceeded market expectations, rising to 54.9.

Chart: Employment data exceeded expectations across the board.

On the other hand, the loose financial conditions have also created room for economic rebound. By comparing the financing costs and investment returns of residents and corporate sectors, as well as comparing real interest rates and natural interest rates, we calculated that the 3.7% long-term bond rate has already lowered financing costs below the investment return rate, which means it can boost demand.How much rate cut is "enough"? The decline in long-term bond rates and broad financial conditions occurred as early as the second half of 2023. Compared to the federal fund rate, financial conditions are more relevant to the actual financing costs of the real economy.

These changes have dampened the recession narrative and rate cut expectations. The CME interest rate futures imply that the probability of another 50bp rate cut in November has dropped to zero. By September 2025, a total rate cut of 100bp had taken place, 50bp less than the market expected before the September FOMC meeting. On September 30th, Powell reiterated at the National Association for Business Economics annual conference[2] that the U.S. economic conditions are good, and risks are two-sided. The Fed has not predetermined any path and will continue to make decisions at each meeting. On the same day, Fed Governor Bowman, who voted against the 50bp rate cut, once again stated[3] that the risks of inflation rising remain prominent, and they will continue to cautiously adjust their future policy stance.

Chart: The CME interest rate futures imply that the probability of another 50bp rate cut in November has dropped to zero.

In addition, there are still disturbances on the supply side, but it has not yet changed the rate reduction path. The consistent expectations for overall and core CPI month-on-month have slightly declined in September, but the changes in the Middle East geopolitical situation since October and the strike by East Coast port workers have increased the uncertainty of October inflation.

1) The escalating geopolitical situation in the Middle East has led to an increase in oil prices. The conflict escalation between Iran and Israel has raised concerns in the market about interruptions in crude oil supply, causing Brent crude prices to rise continuously from $72/barrel to $78/barrel. If the situation further intensifies, we believe that the supply-side shock will lead to an increase in inflation.

2) A three-day strike by American port workers has exacerbated short-term supply chain pressures. From October 1st to October 3rd, approximately 45,000 workers at 36 ports on the East Coast and near the Gulf of Mexico went on strike, blocking at least 54 container ships from unloading. After reaching a temporary agreement to increase wages by 62% over the next six years, the strike was quickly resolved. However, it will still take some time to restore normal cargo flow, and the pressure on the supply chain end may transmit to inflation prices.

Chart: Since October, Brent crude prices have continuously risen from $72/barrel to $78/barrel.

The "new" changes in the Sino-US cycle: rebound or reversal? The directions have all changed, with the U.S. private sector recovery or more clearly, and China requiring fiscal cooperation to match.

We in "New Changes in the China-US Credit CycleIt is pointed out that compared to the private sector leveraging up, the changes in China are more driven by the fiscal expenditure of the government sector, while in the USA, it is more affected by the monetary policy's impact on private credit, such as residential real estate and corporate investments. The resonance of the 'mini-cycle' of the credit cycle in the first quarter of this year between China and the USA is actually due to this, explaining the rise of the real estate chain in the USA, the export chain in China, and global industrial metal prices. Standing at the current position, the forceful policies in China and the cooling expectations of the USA recession indicate a change in direction, which in turn will limit our internal easing space and further emphasize the importance of fiscal intensity.

Chart: China and the USA actually achieved a 'mini-cycle' resonance of the credit cycle in the first quarter of this year

Due to the USA's earlier and sustained low financial conditions, high elasticity sectors have rebounded, and the trend of private sector leveraging up is more prominent.

1) Credit Pulse: Banks' credit pulses have already turned a corner by the end of 2023, with the industrial and commercial loan pulse already turning positive.

2) Corporate Sector: The credit spreads reflecting direct financing continue to narrow, with high-yield and investment-grade credit spreads narrowing by 30bp and 6bp in the third quarter respectively, falling back to levels prior to the rate hike in 2022, further driving a 16% quarter-on-quarter increase in bond issuance size to $502.3 billion in the third quarter.

3) Residential Sector: The 30-year mortgage rate has fallen to around 6.1% under the influence of the U.S. Treasury yield, approaching the level of September 2022. The refinancing application index has also risen to a new high since the rate hike in March 2022. Although high house prices to some extent restrain substantial sales recovery, the increase in refinancing volume can marginally improve residents' interest payment pressure, providing support for consumption.

Therefore, compared to the decline, what needs to be verified more is the credit cycle restarting transmission to hard data, as well as the extent and speed of economic rebound.

Chart: Financial conditions eased earlier and have been maintained at a low level.

Chart: The bank's crediting pulse has already shown a turning point by the end of 2023, and the industrial and commercial loans pulse has turned positive.

Chart: The scale of bond issuance in the third quarter increased by 16% to $502.3 billion compared to the previous quarter.

The certainty in China lies in the decrease of financing costs, but the external maximum space may gradually pass; it is necessary to observe whether the fiscal strength is sufficient. Compared to the current policy tools, a complete reversal of the credit cycle trend still depends on fiscal efforts. Otherwise, there may be a lack of clear fundamental support after being driven by emotions and liquidity. In terms of policy intensity, we attempt to calculate statically from the difference between investment return rates and financing costs.

1) Monetary: Our calculation shows that a further 45-70 basis point drop in the 5-year LPR to 2.95%-3.2% would help solve the current issue of investment return rates falling below financing costs.

2) Fiscal: In order to bring fiscal impulses back to historical highs, or to return the overall social financing growth rate from the current 8.1% to the 10% level at the beginning of 2023, our calculation indicates the need for an additional issuance of 7-8 trillion yuan.

From this perspective, the current policy intensity still has gaps, so it is necessary to pay attention to the subsequent implementation of policies.

Chart: A further 45-70 basis point drop in the 5-year LPR to 2.95%-3.2% would help solve the current issue of investment return rates falling below financing costs.

Chart: The growth rate of social financing has been restored to 10% (the level at the beginning of 2023), requiring an additional issuance scale of 7-8 trillion yuan.

For China, the restart of the U.S. credit cycle means that the fiscal importance is increasing further, so the most sensitive stage of loose expectations is gradually passing. On the one hand, this round of the United States is more likely to be a preventive rate cut under a soft landing scenario, and the rate cut space may not be very large. The more aggressive unconventional rate cuts may make subsequent rate cuts not need to be very large ("Federal Reserve's 'unconventional' rate cuts kick offThe unsecured environment faced domestically may gradually pass at the time when the biggest external loose environment may occur.

On the other hand, although the positive effect of the U.S. credit cycle restart is the support for exports, the impact of the elections needs to be considered. Currently, exports are an important support and bright spot for China's growth. The restart of the interest rate-sensitive U.S. real estate cycle will help stabilize China's export growth. Just as the resonance of the Sino-U.S. cycle in the first quarter pulled the export chain of our country. But next year, the export chain will also be affected by the elections. According to RCP statistics, Trump's recent approval rating has risen again, especially the gambling approval rating leading by nearly 4 percentage points, and the situation in key swing states like Pennsylvania has reversed again.

Chart: Trump's recent approval rating has risen again, especially the gambling approval rating is once again leading by close to 4 percentage points.

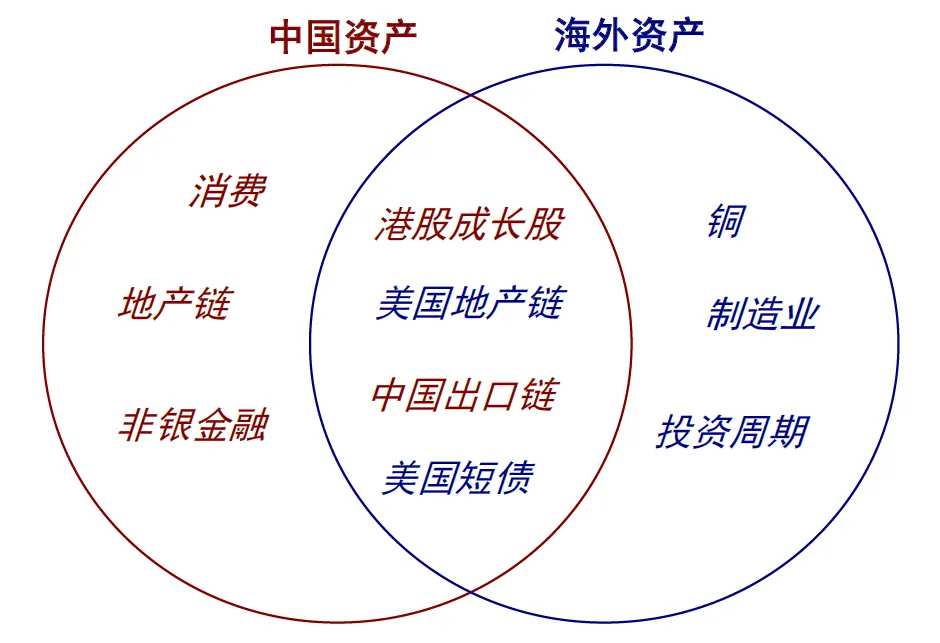

Allocation advice: The most clear 'crossing point' is the synergy between short-term debt, real estate, China's export chain, and Hong Kong stocks growth; a larger rebound and pro-cyclical policies require policy support.

Looking ahead, we believe that the changes in the Sino-US cycle have already spawned an asset 'crossing point'. The change in the Sino-US cycle brings a more certain 'crossing point' which includes U.S. short-term debt, real estate chain, China's export chain, with Hong Kong stocks (especially growth) outperforming A-shares.

1) Overseas: From economic data perspective, the expected full inclusion and the anticipated downward trend in long-term interest rates increase the possibility of a soft landing, thereby indicating that the Fed may not need to cut rates as much. The U.S. may be approaching an economic cycle turning point, and compared to U.S. bonds and gold, what is more certain is the short-term debt directly benefiting from the Fed rate cuts (short-term debt is more cost-effective than long-term debt, should steepen the curve), and the gradually recovering real estate chain (even driving the related Chinese export chain).

2) Domestic: Short-term market sentiment in the Hong Kong stock market has been overdrawn, and trading may return to core assets. We continue to recommend focusing on interest rate-sensitive growth stocks (internet, technology growth, biotechnology, etc.) and export chains driven by U.S. real estate demand.

Chart: The most clear 'crossing point' is the synergy between short-term debt, real estate, China's export chain, and Hong Kong stocks growth.

Larger index rebounds and pro-cyclical performance require the catalysis and coordination of data and events. If the future economic and fiscal data of the USA and China are validated in the next one or two months, industrial metals such as copper, the manufacturing sector of the USA, and pro-cyclical sectors in China are also worth paying attention to.

1) Overseas: Along with the recovery of economic, especially investment cycles, industrial metals such as copper can gradually become the focus, but currently they are still somewhat biased to the left side, awaiting validation of several important subsequent data points such as the USA's election day (November 5), November FOMC (November 8), and inflation in October following the rise in oil prices and strikes in September (November 13).

2) Hong Kong Stock Market: We estimate that if the risk premium falls to 6.7%, the level of the market high point in May 2024, or supports the Hang Seng Index at around 21,000 points; if sentiment continues to improve to 6.1%, the level of the market high point after China's epidemic policy adjustment in early 2023, the Hang Seng Index may reach around 22,500 points. However, at that time, China's supply chain is the fastest to recover globally, while the real estate sector is also at historical highs, and it is currently difficult to compare the balance sheets of various sectors. We believe that if the policies are constantly delivered and the fiscal efforts exceed expectations, pro-cyclical sectors directly benefit, such as consumption, real estate chains, and non-banking finance.

Chart: If fiscal policy strengthens to boost the cyclicals, on the contrary, focus on structural opportunities.

Chart: Overseas assets have a similar pattern to the 2019 cycle, trading interest rate cuts should be thought of and done in moderation in the opposite way.

编辑/Wade