分析认为,这些文件,包括财务报表和预测,可能会改变一些人对OpenAI财务前景的看法,产生乐观情绪。

分析认为,这些文件,包括财务报表和预测,可能会改变一些人对OpenAI财务前景的看法,产生乐观情绪。OpenAI previously completed a 6.6 billion US dollar financing, with a valuation already exceeding 150 billion US dollars.

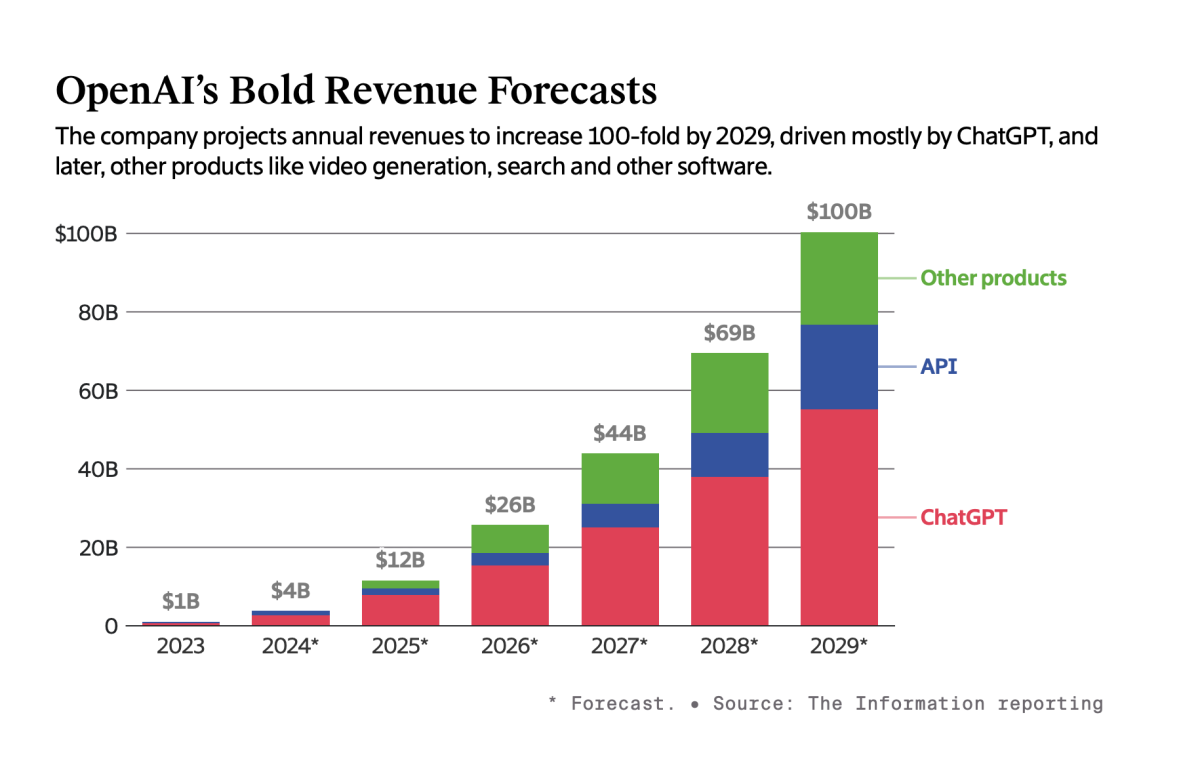

OpenAI previously completed a $6.6 billion financing, with a valuation exceeding $150 billion. However, according to media analysis of OpenAI's financial documents, the company's losses next year could reach $14 billion, nearly three times the expected loss this year. It is estimated that the company will not be profitable until 2029, when revenue will reach $100 billion. This estimate does not include equity compensation, although this expense is one of OpenAI's largest expenses but not a cash payment.

According to The Information, OpenAI's financial documents show that the company emphasizes profit indicators to investors by excluding some major expenses, such as the billions of dollars spent annually on training large language models. If these expenses are excluded, OpenAI is expected to be profitable by 2026.

Although losses are still high, the financial outlook is optimistic.

Analysts believe that these documents, including financial statements and forecasts, may change some people's views on OpenAI's financial prospects, generating optimism.

Analysts believe that these documents, including financial statements and forecasts, may change some people's views on OpenAI's financial prospects, generating optimism.

Firstly, OpenAI's cash burn rate is much lower than previously expected. In the first half of this year, the company burned around $0.34 billion, with $1 billion in cash on its balance sheet before financing. However, the documents suggest that cash consumption could increase sharply in the coming years.

Secondly, there is a significant gap between OpenAI's cash flow and its loss figures, reflecting different treatment of its major expenses (such as equity compensation and computing credits) in the two financial statements under standard accounting principles. In the first half of this year, OpenAI's calculated net loss was $3 billion.

OpenAI expects total spending to exceed $200 billion by 2029, excluding equity compensation costs. At the same time, 60% to 80% of the annual expenditure will be used for model training or operation.

The document analysis indicates that OpenAI is expected to incur a total loss of $44 billion from 2023 to 2028 (excluding equity compensation). The same analysis also shows that the company expects profits of $14 billion in 2029 based on this.

In the first half of this year, the company reported equity compensation of $1.5 billion, which may be comparable to the income for that period.

The document suggests that Microsoft extracts a 20% share of revenue from OpenAI, a ratio higher than previously expected.

OpenAI expects that the computational costs of model training may significantly increase in the coming years, reaching as high as $9.5 billion annually by 2026. This is a supplement to the upfront training costs amortization for large language model research, with financial documents allocating the computational costs over several years. This figure is also rapidly rising, from the expected $1 billion this year to over $5 billion in 2026.

Some of OpenAI's computational costs are not paid in cash. In last year's $10 billion investment in OpenAI, Microsoft prepaid for computing credits. According to documents and insiders revealing to the media, in the first half of this year, OpenAI had approximately $0.5 billion in data center leasing fees paid by Microsoft.

It is currently unclear how much computing credit OpenAI still has. However, if the company increases its computing expenses as per documents, it may need to use more of its own funds. Previously, there were reports that OpenAI is discussing borrowing to establish data centers more quickly, surpassing Microsoft’s pace.

Nevertheless, analysts believe that if future models are more sustainable than previous ones, because competitors cannot catch up quickly, or due to future breakthroughs leading to lower model training costs, OpenAI can reduce computing expenses. This would reduce the need for cash resources.

If OpenAI's popular product ChatGPT grows as expected, and the company can generate revenue from new products, investors may overlook the expenses. By 2029, when OpenAI's profitable business has been around for a decade, the company is expected to generate revenue comparable to the income of NVIDIA and Tesla in the past 12 months.

ChatGPT will lead sales.

OpenAI believes that ChatGPT will continue to account for the vast majority of its revenue in the coming years, far exceeding the revenue from selling AI models to developers through APIs. The company also forecasts that new products will surpass API sales by the end of 2025, reaching nearly 2 billion dollars that year.

Although it is unclear what these new products are, insiders told the media that the company is currently developing agent-related products, which can use people's computers to process complex and monotonous tasks, as well as research assistants.

In addition, the company has discussed raising subscription prices for its most advanced AI technology. Other products not yet fully launched in the market include the Sora video generator, a more direct competitor to Google search, and software for robot developers.

OpenAI also expects API sales growth to significantly slow down. The reasons are unclear, despite increased competition in this field from competitors like Anthropic, Microsoft, and Google.

However, these predictions may be based on the assumption of the company maintaining a leading position in AI development, despite facing increasing competition and more employee turnover.

The gross margin may increase.

OpenAI expects its gross margin (a profit indicator reflecting the percentage of direct operating costs to revenue) to reach about 41% this year. This ratio is far below the typical level of 65% to 70% for cloud software startups. The higher costs are mainly attributed to the computational power required to run existing models (known as inference computing), expected to reach 1.8 billion dollars out of 3.7 billion dollars in revenue this year.

Currently, OpenAI's direct business costs are slightly higher than the losses of the giant Uber in 2016, which went public three years later.

OpenAI stated that as revenue grows faster than computing costs, the business model will improve, with a gross margin of 49% next year and 67% in 2028.

One of OpenAI's supporters, Altimeter Capital, stated that this is mainly due to the decrease in inference costs. Altimeter cited OpenAI data showing that developer fees for using GPT-4 decreased by 89% from March 2023 to August 2024.

Employee numbers are increasing while data expenses are decreasing.

OpenAI's largest operating expense is employee costs, expected to reach around 0.7 billion USD this year, excluding stock-based compensation. The company expects that next year, the number of employees will increase, and salary expenses will almost triple to reach 2 billion USD. However, the growth of these costs is expected to slow down thereafter.

OpenAI predicts that another major operating expense, data costs, will expand to around 0.5 billion USD this year, gradually decreasing to 0.2 billion USD in the following years. This means that the company believes that future data expenses for training models will not be as high as this year's, as they have signed numerous licensing agreements with media companies this year.

Financial estimates also show that OpenAI does not expect to invest too much funds in sales and marketing to increase revenue, with these expenses expected to account for 5% to 7% of revenue. This is lower than the typical proportion sales and marketing expenses in popular consumer subscription businesses like Netflix and Spotify take up of revenue.