数据来源:CFTC/LSEG Workspace

数据来源:CFTC/LSEG WorkspaceIn September, the new job additions in the USA exceeded market expectations, causing the market to change the interest rate cut in November from 50 basis points to 25 basis points, reducing the popularity of gold.

According to the Zhutong Finance APP, European Natural Resources Fund Commodity Discovery analyst Li Gangfeng stated in a post that last week Powell stated that the Fed is not in a hurry to cut interest rates. He believes that if the US economy develops as they predict, the US will cut interest rates twice more this year, totaling 50 basis points (a total of 1% this year). After the speech, both the stock market and gold showed signs of deflation. In addition, the announcement last Friday that the new job additions in the USA in September exceeded market expectations caused the market to change the interest rate cut in the USA in November from 50 basis points to 25 basis points, reducing the popularity of gold.

The previously provided new job addition data from the US official institutions has been confirmed to be a joke (the number of new job additions in the past year has been adjusted down by nearly 1 million). It appears that the market is still trading simply based on the government-provided data. In other words, the investment market trend is entirely dependent on the government's preferences, disconnected from the fundamentals, which is a dangerous situation. He stated that even though there is a trend of technical deterioration in gold, the support provided by the Middle East situation should not be ignored.

Data source: CFTC/LSEG Workspace

Data source: CFTC/LSEG Workspace

*For comparison purposes, the metal equivalent of COMEX gold is divided by 10, while the metal equivalent of COMEX silver is divided by 100.

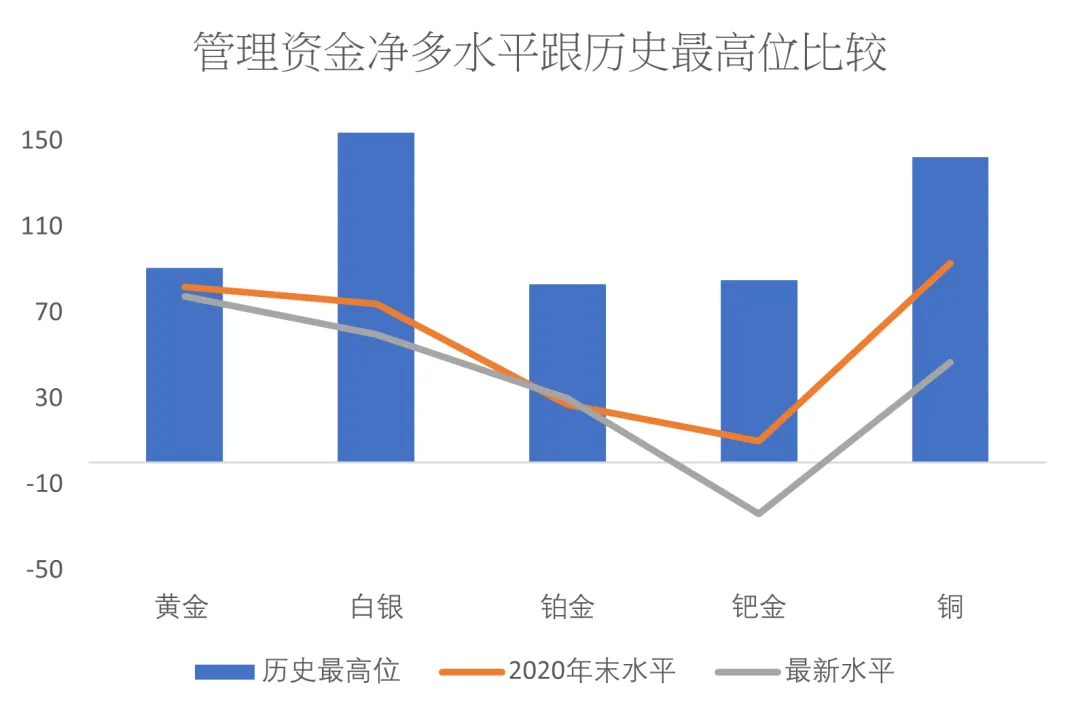

As of last Tuesday, only the platinum and copper funds in the US metal index continued to rise in net long positions, while other metals saw a decline in net long positions.

The bullish trend in US gold futures funds fell nearly 6% last week compared to the previous week, ending three consecutive weeks of gains; at the same time, bearish positions plummeted by 35%. As a result, fund holdings fell from a net long position of 793 tons to 775 tons, marking the 51st consecutive week of net long positions (previously 46 weeks). This also represents 85% of the historical peak of 908 tons in September 2019, nearing the highest levels in recent years. As of October 1st, the price of gold in US dollars has risen by 28.9% this year (up 28.7% from the previous week); meanwhile, fund long positions have accumulated a 49.7% increase during the same period (up 58.3% from the previous week).

Silver, which has a high correlation with gold prices, has always exhibited stronger volatility than its cousin, gold. Last week, bullish positions in US silver futures fell by 9% compared to the previous week; meanwhile, bearish positions rebounded by 18%. This led to a decrease in fund holdings from a net long position of 7167 tons to 5969 tons, marking the 30th consecutive week of net long positions and accounting for 39% of its peak period. As of October 1st this year, the price of silver in US dollars has risen by 32.2%, while bullish positions in silver funds have accumulated an increase of 44.6% (down from 59.4% the previous week), and bearish positions have decreased by 25.3% (down from 36.9% the previous week).

Bullish positions in US platinum funds rose by 7% last week compared to the previous week, while bearish positions fell by 10%. This resulted in an increase from a net long position of 24 tons to 30 tons, the highest level in the past 18 weeks. Historically, US platinum fund net short positions were maintained for the longest consecutive period of 31 weeks (from April 2018 to October 2018).

Net short positions in US palladium funds fell back to 24 tons. The author believes that even though the bull market in palladium may have ended, if palladium continues to maintain a significant net short position, it may still be quite difficult for other precious metals to completely reverse the trend. US palladium fund holdings have been in a net short position for a record 97 consecutive weeks, marking the longest net short period in history.

Funds in US gold futures have risen by 84% in net long positions from the beginning of the year to date (up 101% in 2023).

Data source: CFTC/LSEG Workspace

Fund net long position in US futures silver rose 125% from the beginning of the year to date (cumulative decline of 44% in 2023).

Data source: CFTC/LSEG Workspace

Fund net long position in US futures platinum has risen 13.2% since the beginning of the year (cumulative decline of 7% in 2023).

Data source: CFTC/LSEG Workspace

Fund net long position in US futures copper has risen 175% since the beginning of the year (cumulative decline of 0.3% in 2023).

Data source: CFTC/LSEG Workspace

Basically, it can be seen from the chart that despite the global inflation rising over the past few years, prices of various metals have all experienced different degrees of decline. The main reason is the lack of funds in the futures market to drive leverage. If someone had a crystal ball years ago and knew that global inflation, conflicts, and uncertainties would sharply rise this year, and went long on precious metals in the futures market, they would very likely lose money. Since the global spread of the pandemic in 2020, the net long positions of precious metals in the US futures market have continued to decline, reflecting the deliberate action of funds to prevent precious metals from rising.

CFTC's weekly reports on the COMEX copper market have been available since 2007. Due to the bear market in copper from 2008 to 2016, most of the time the net position in copper futures in the US has been negative, which is not surprising. However, starting from 2020, due to the impact of the global pandemic on the supply side and mining operations, and the market's expectation of strong demand for copper in electric vehicles, copper prices have risen, reaching new historical highs. But the current global investment concept is that the world is entering an economic recession, leading to a decrease in demand for commodities.

As the US presidential election approaches (in October) or in 2025, one should be cautious about the possible decline in copper prices. The price of copper is closely related to the US stock market. However, on the other hand, China's strengthening of funding into the stock market should help support copper prices from a confidence perspective.

The author has updated important insights into the short-term direction of gold prices and gold mining stock indicators. Last week, the US dollar gold price/North American gold mining stock ratio increased:

Data Source: LSEG Workspace

As of Friday (4th), the gold price/North American gold mining stock ratio was 16.78X, up 2.6% from the 27th, marking the third consecutive week of increase. The ratio reached a new high for the year of 19.22X (closing price basis) 33 weeks ago. It has accumulated a 2.1% increase for the year. The full-year increase of 13.2% for 2023 (6.4% for 2022), with the highest ratio at 17.95 in 2023, and the lowest in 2023 and 2022 at 13.99X and 11.24X in January, respectively.

The author believes that tracking the overseas gold mining stock prices is one of the more reliable forward-looking tools. That is, if the gold price continues to rise but the gold mining stocks experience a sharp drop, one should be careful.

Gold-to-silver ratio

The gold-to-silver ratio is an indicator of market sentiment. Historically, the gold-to-silver ratio has ranged from approximately 16 to 125.

Data Source: LSEG Workspace

Generally, the more fearful the market, the higher the gold-to-silver ratio. For example, in 2020, the spread of the virus globally led to a historical high in the gold-to-silver ratio, which once reached over 120 times.

Last Friday, the gold-silver ratio index was 82.37, a weekly decrease of 1.8%, a year-to-date decline of 5.0%. The cumulative increase in 2023 is 14.0%, with the highest and lowest points in 2023 being 91.08 and 75.93 respectively. In 2022, there was a decrease of 3.1%.

It is important to note that both the US dollar gold price/North American gold mining stocks ratio and the gold-to-silver ratio are clearly showing a trend of rebounding from the bottom. The financial market has clearly entered into recession trading.

The market expects a major turnaround in the probability of a US interest rate cut in November.

At the time of writing, the market believed that the probability of the Fed cutting interest rates on November 7 by another 50 basis points plummeted from 53.3% two weeks ago to 0% last Friday. Currently, the market believes that the probability of a 25 basis point reduction in November is as high as 97.4%:

Image source: CME Group

This is a futures market prediction of the interest rate probability distribution for the USA in December 2024 at the time of writing:

Image source: CME Group

As of last Friday, the mainstream market belief was that the United States would cut rates by 50 basis points for the remainder of this year.

One week ago, the market believed that there was a 49.7% chance that the United States would cut rates to 4.00%-4.25% at the end of the year, but by last Friday, this probability plummeted to 17.7%; on the other hand, the probability of a rate cut to 4.25-4.50% soared from 21.3% a week ago to 80.2% last Friday. The market believes that the pace of rate cuts in the United States has become more cautious. In just one week, the market has made such a significant adjustment in expectations for US interest rates, once again confirming what the author has said: After a long period of verification, futures market predictions of US interest rate trends, especially forward expectations, are generally wrong. For example, the market had originally expected the Fed to cut rates by only 25 basis points in September, but a week before the meeting, the market bet that the Fed would suddenly raise rates by 50 basis points, believing that some people in the market had received information.

The author originally believed that when the Federal Reserve cut rates by 25 basis points in September, it was the peak of the US stock market; therefore, a 50 basis point cut was indeed somewhat unexpected (it is important to note that a week before the interest rate meeting in September, the economic data released by the United States was not as poor). The result of the 50 basis point cut is to temporarily shift trading from recession to optimism.

Last week, Powell stated that the Federal Reserve is not in a hurry to cut rates. He believes that if the US economy develops as they predict, the US will cut rates twice more this year, totaling 50 basis points (a total cut of 1% this year). After the speech, both the stock market and gold showed signs of deflation. In addition, the favorable announcement of better-than-expected US job additions in September last Friday changed the market's expectation of a 50 basis point rate cut in November to 25 basis points, reducing gold's popularity.

Previously, the official data on new job additions provided by US government agencies has been confirmed to be a farce (with a downward adjustment of nearly 1 million new jobs in the past year). It seems that the market still simply trades based on government data, in other words, the trend of the investment market is completely controlled by the government's preferences and is detached from fundamentals, which is a dangerous situation.

The current market situation is clear - if there is no major drop in the US stock market (in the event of a major drop, safe-haven assets benefit), then risk assets (the most popular companies in the US stock market, digital currencies, silver, copper, and other commodities) and safe-haven assets (including bonds and gold) will rise to varying degrees.

However, it is important to note that the Federal Reserve will have its next interest rate meeting in November, in other words, the focus of the US stock market in October may very likely shift to the US presidential election. And given the current situation where the two candidates seem evenly matched, it is estimated that due to uncertain factors, the US stock market may become even more volatile in October.

According to the World Gold Council, before the National Day holiday in China and India, whether it is in China or India, local gold prices were at a discount to international prices, reflecting that, for the physical market, the gold prices have signs of being overbought:

Image Source: World Gold Council

Whether the Chinese gold price can return from discount to premium after the National Day holiday may be a short-term key for gold prices.

The biggest test in the next 12 to 24 months, if the USA starts to cut interest rates, but inflation pressures regain momentum, what will the Fed do?

Even though there is a trend of technical deterioration in gold, do not ignore the support provided by the situation in the Middle East for gold prices.

Although the local currency has appreciated recently, the author believes it is only a transitional reversal after the strong US dollar squeezed trades. Especially although environmental protection stocks rebounded generally last week, the author tends to believe that this rebound is just a flash in the pan / luring more funds to join the game. Therefore, it is recommended to gradually reduce risk assets during this rebound (but not sure how long it will last) and secure profits.