利率期货市场的交易员们现在认为,美联储在 11月份转向降息25个基点的可能性高达85%。相比之下,在非农就业报告出炉之前债券市场押注降息25基点的押注概率则勉强超过50%,押注降息50个基点的概率则一度高于25个基点。

利率期货市场的交易员们现在认为,美联储在 11月份转向降息25个基点的可能性高达85%。相比之下,在非农就业报告出炉之前债券市场押注降息25基点的押注概率则勉强超过50%,押注降息50个基点的概率则一度高于25个基点。If the US CPI data in September is very strong, the rate cut in November will become "uncertain".

According to 36Kr Finance, the Wall Street financial giant Bank of America recently released a report stating that the importance of the upcoming consumer inflation data report (CPI data report) this week has significantly increased, as data higher than the market's general expectations may further sow doubts among investors about whether the Fed will choose to cut rates next month. For months, non-farm payrolls have been the most closely watched U.S. economic data by global investors because the strength of non-farm data is crucial for the pace and rhythm of the Fed's rate cuts. However, this week investors are refocusing on the U.S. CPI data report, which will determine whether the Fed will continue to cut rates throughout the year. The September CPI statistics will be released on Thursday night Beijing time.

The latest release of extremely strong U.S. non-farm payroll data, coupled with the unexpected drop in unemployment rates, has led traders to significantly reduce their bets on the Fed making another large 50 basis point rate cut. Since August 1, the interest rate futures market pricing has for the first time suggested that by the end of the year, the Fed's benchmark interest rate cut may be less than 50 basis points, indicating that some traders are even pricing in the possibility that the Fed may pause its rate cuts at the November or December FOMC meetings.

Traders in the interest rate futures market now believe that there is an 85% chance that the Fed will shift to a 25 basis point rate cut in November. By comparison, before the non-farm payroll report was released, the probability of a 25 basis point rate cut in the bond market was just over 50%, while the probability of a 50 basis point cut once exceeded that of a 25 basis point cut.

Traders in the interest rate futures market now believe that there is an 85% chance that the Fed will shift to a 25 basis point rate cut in November. By comparison, before the non-farm payroll report was released, the probability of a 25 basis point rate cut in the bond market was just over 50%, while the probability of a 50 basis point cut once exceeded that of a 25 basis point cut.

In the U.S. bond trading market, with most global bond traders at least temporarily abandoning their bullish bets on U.S. Treasuries, the yield on the 10-year U.S. Treasury, known as the 'anchor of global asset pricing,' has risen to its highest level since August, breaking the key 4% yield threshold. Short-term U.S. Treasuries of 2 years and below have performed particularly poorly, indicating a temporary reversal in a key part of the yield curve trend, highlighting a significant cooling of the bond market's expectations for the Fed's future rate cuts.

A rate market strategist from TD Securities commented: "The market discourse is even shifting towards whether the rate cuts will continue." "From an economic perspective, things are not that bad, which has led the market to reassess the Fed's rate cut path." TD Securities continues to expect the Fed to choose a 25 basis point rate cut in November, rather than sticking to a 50 basis point cut.

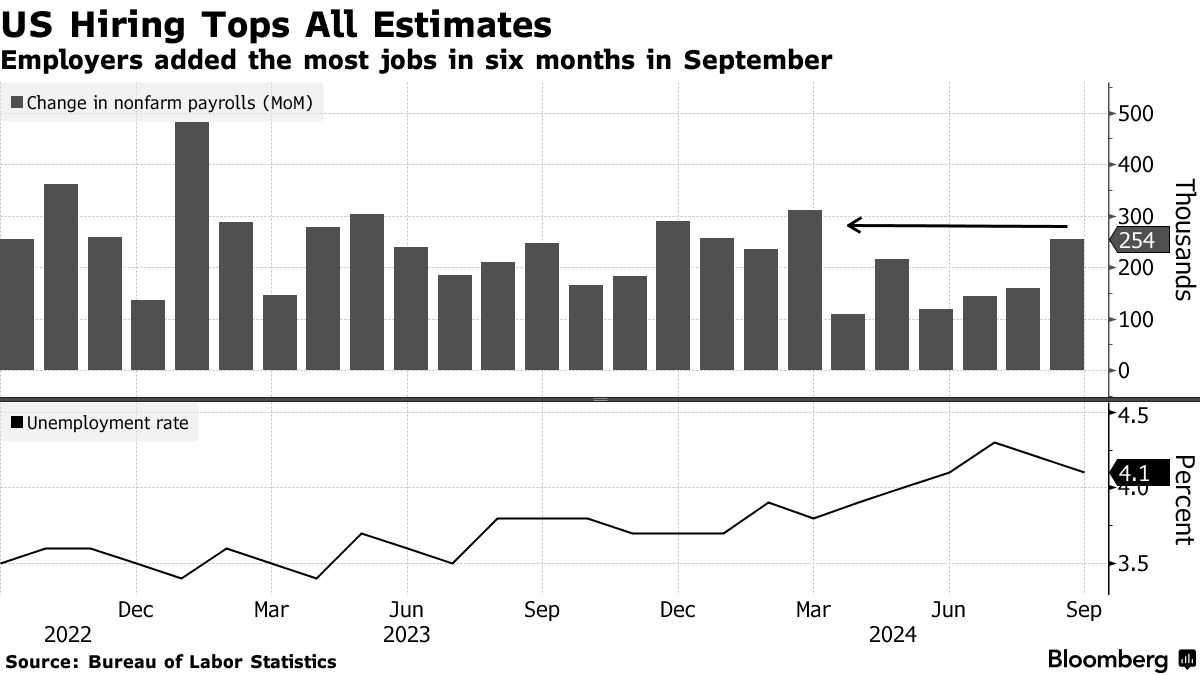

According to data released by the US government on Friday, following upward revisions of 0.072 million non-farm employment in the previous two months, non-farm employment in September surged unexpectedly by 0.254 million, marking the largest increase in non-farm additions in six months. In contrast, economists' median expectation was only 0.15 million, with the latest non-farm figures exceeding even the most optimistic expectations shown in media surveys. According to another data released by the US Bureau of Labor Statistics on Friday, the unemployment rate unexpectedly fell to 4.1%, hourly earnings rose by 0.4% more than expected, both data points surpassing economists' expectations (4.2% for the unemployment rate and 0.3% for hourly wage growth).

Combined with other data released last week, US companies' demand for workers remains healthy, with very low layoff numbers. Earlier economic data also indicates the resilience of the US economy, and the non-farm employment report is likely to significantly alleviate economists' concerns about a rapid cooling of the US labor market and fears of an economic recession. The situation in the US labor market is closely related to US consumer spending, with employment scale and wage income being crucial for overall consumption. Consumer spending resilience will undoubtedly drive the US economic juggernaut forward, as 70%-80% of components in the US GDP are closely related to consumption.

USA Bank predicts: If CPI is higher than expected, the expectation of 'pausing rate cuts' may sweep through the financial markets.

The September CPI data to be released this week in the USA may provide a clearer picture of the Fed's rate cut trajectory. USA Bank forecasts a month-on-month increase of 0.3% for the core CPI index in September, which is in line with economists' expectations. If this expectation becomes a reality, it could result in two consecutive strong performances for core CPI indexes. In terms of overall CPI expectations, USA Bank expects a 0.1% month-on-month increase in line with economists surveyed by institutions, potentially recording the smallest increase in 3 months. Regarding year-on-year growth, economists generally expect a 2.3% increase in overall CPI in September, down from 2.5% previously; expected core CPI to increase by 3.2% year-on-year, consistent with the previous value.

Ohsung Kwon, stock and algo strategist at Bank of America, stated in a report released on Sunday: 'If our predictions are proven correct, it will further solidify the market's expectation of a 25 basis point rate cut by the Fed in November.' 'At the same time, inflation is unlikely to be soft enough to guarantee a 50 basis point rate cut, but very strong inflation data may make the Fed's rate cut process in November less certain. Calls in the market to pause rate cuts may grow stronger.' This crucial CPI data report will be released on Thursday evening Beijing time.

The Bank of America strategy team led by Ohsung Kwon stated that after the employment report was released, the market's forecast for the Fed's rate cut magnitude before the end of the year was less than 50 basis points. However, the US stock market rose due to expectations of a 'soft landing' for the US economy. After the non-farm employment report was released, traders in the financial markets basically ruled out the possibility of a significant 50 basis point rate cut by the Fed in November.

Strategist Kwon does not believe that there is substantial upward risk in the Bank of America's latest inflation forecast. 'Although the September non-farm payroll growth was stronger than market expectations, the overall labor market data indicates a better balance between demand and supply,' stated the team led by this strategist. 'In fact, the continuing downward trend in quit rates suggests that wage and price inflation should continue to moderate.'

Kwon stated that the expected volatility from the Consumer Price Index report is estimated to cause the benchmark index of the US stock market - the S&P 500 index - to fluctuate by approximately 109 basis points this Thursday, an increase from last week's 91 basis point fluctuation. This will also be the largest scale of 'US Consumer Price Index Day' stock market volatility since May. The average volatility of the S&P 500 index for the current 3-month benchmark period is around 70 basis points.

The strategist also stated: "Although given the continuous improvement of more macro data, the US stock market should be able to withstand a slight unexpected increase in inflation, but a significant unexpected outcome beyond expectations may bring great uncertainty to the Fed's easing cycle and cause larger-scale volatility in the stock market."

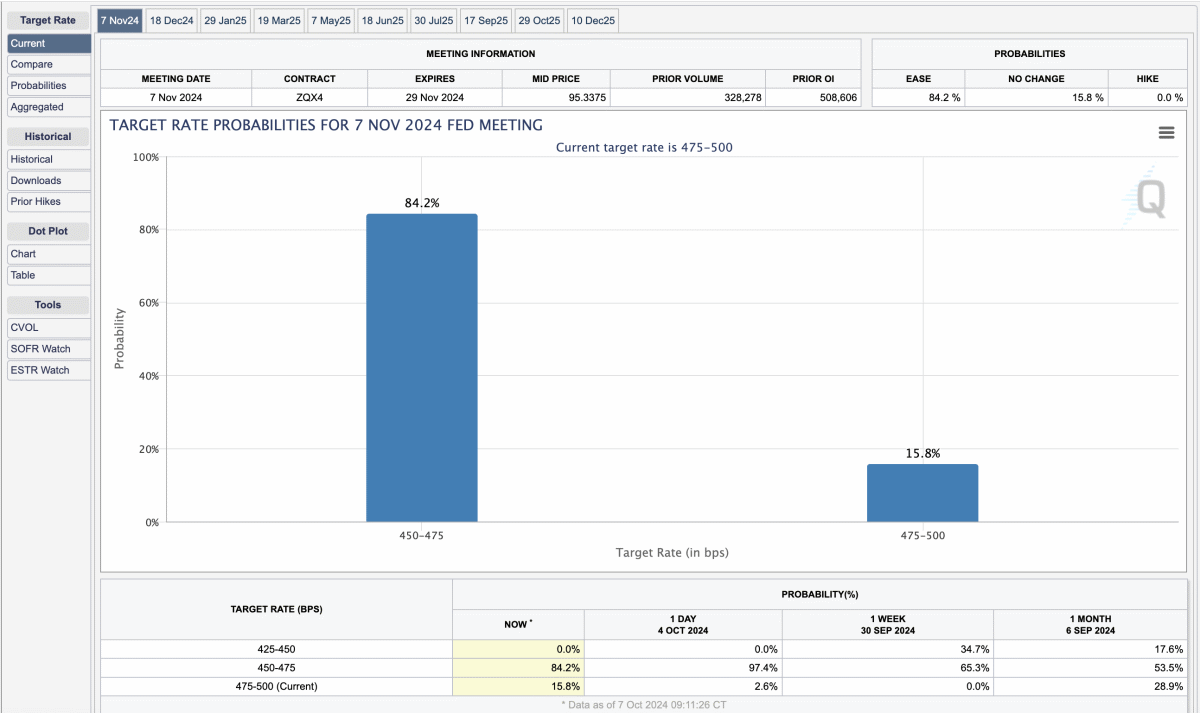

According to the CME's "Fed Watch Tool," during the period when US Treasury prices across all maturities fell due to the expectations of interest rate cuts on Monday, the probability of the Fed remaining unchanged next month surged from 2.6% on Friday to 15.8%. The probability of a normalized 25 basis point rate cut decreased from a high of 97.4% to 84.2%, and the voices calling for a 50 basis point rate cut have almost disappeared. These latest rate cut probabilities compiled by CME imply that an increasing number of interest rate futures traders are betting that the Fed's next rate cut will be a normalized 25 basis point cut, and some more aggressive traders are betting that strong non-farm payrolls data will push inflation back up, thereby prompting the Fed to choose not to cut interest rates in November or December.

In a report on Monday, the economist team at Citigroup on Wall Street indicated that they expect the Fed to cut interest rates by 25 basis points in November, rather than the previously expected 50 basis points cut by the group. After the September non-farm payroll data released on Friday implied that the US economy remains robust, Citigroup, like other Wall Street banks, abandoned the aggressive prediction of a 50 basis point rate cut.

In this report, economists at Citigroup wrote: "The threshold for the Fed not cutting rates in November is quite high, as one month of labor market data has not convincingly reduced the downward economic risks, which have been persistent for several months, and many data sets have prompted Fed officials to choose a 50 basis point rate cut in September." "We believe that there will be a recurrence of a weak labor market in the coming months, the overall inflation trend will continue to slow down, and this may prompt Fed officials to choose a 50 basis point rate cut in December."