分析师们估计,如果散户继续保持乐观情绪,

分析师们估计,如果散户继续保持乐观情绪,According to Daiwa's estimation, if retail investors' sentiment remains high, as much as 2-3 trillion RMB in China's household financial assets will be reallocated to the stock market. As long as the momentum is strong enough, brokerage stocks are expected to rise by another 30%, and roe may rebound to around 13%.

Morgan Stanley believes that if individual investors' sentiment remains high, there is still room for further gains in the Chinese stock market.

Recently, Morgan Stanley's analyst team, led by Chiyao Huang, released research reports indicating that the trading volume and speed of the A-share market have exceeded the levels of 2020-2021, bearing many similarities to the retail bull market of 2015. They observed that new individual investors are the main driving force behind the stock market's rise, with a significant increase in the number of new investors opening accounts, indicating a growing participation of individual investors.

Analysts estimate that if individual investors continue to maintain optimistic sentiment, as much as 2-3 trillion yuan of Chinese household financial assets could be reallocated to the stock market, benefiting brokerage stocks. In addition, the relatively low balance of margin financing currently also indicates potential growth in the future.

Analysts estimate that if individual investors continue to maintain optimistic sentiment, as much as 2-3 trillion yuan of Chinese household financial assets could be reallocated to the stock market, benefiting brokerage stocks. In addition, the relatively low balance of margin financing currently also indicates potential growth in the future.

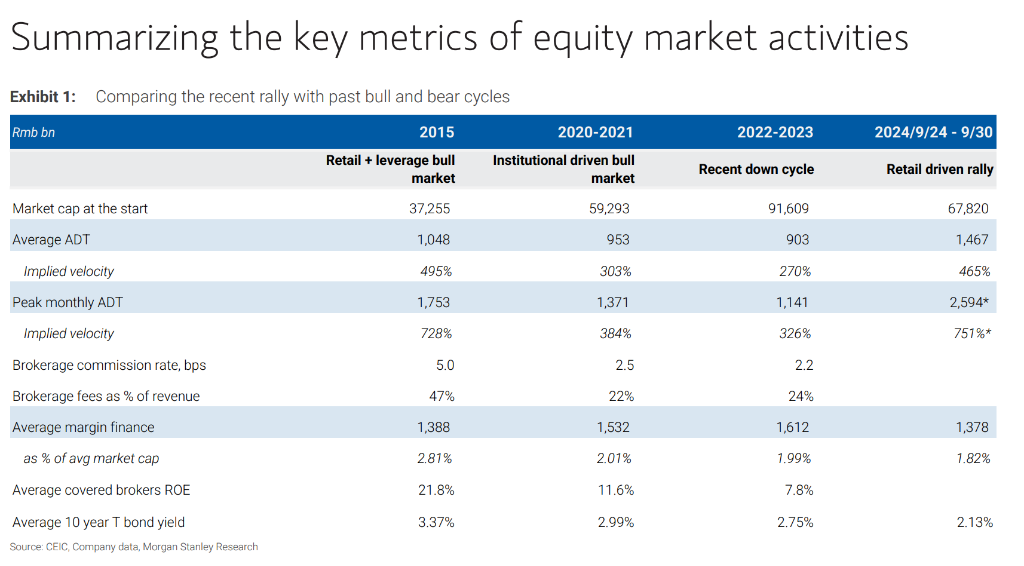

2015 Bull Market Redux? New individual investors become the biggest driving force behind the stock market's rise.

Morgan Stanley summarized the key drivers of the Chinese stock market in different periods: 2015 was a bull market driven by retail investors and leverage, 2020-2021 was institution-driven, and in September 2024, a retail-driven uptrend reappeared.

Data shows that in September 2024, the average daily trading volume and turnover ratio of the Chinese stock market exceeded the levels of 2020-2021, approaching the highs of 2015. On September 30, A-share trading volume hit a historical high of 2.59 trillion yuan, with a turnover ratio as high as 751%, significantly higher than the same period last year.

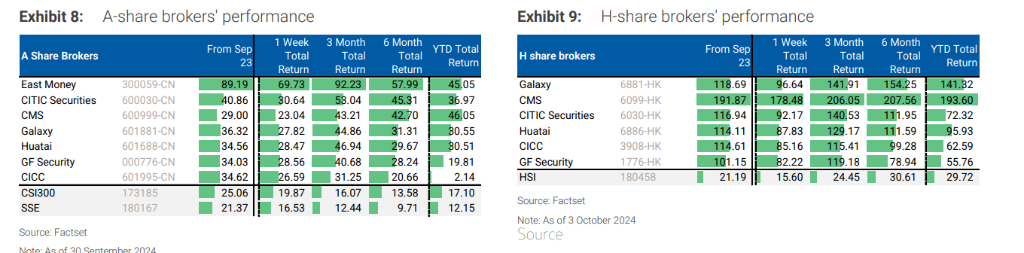

From a sector perspective, Chinese 'bull market leader' brokerage presents a clear uptrend driven by individual investors, sharing many similarities with the bull market of 2015. Morgan Stanley's report states:

Trading volume and speed have exceeded the levels of 2020-2021, similar to the retail-driven bull market of 2015.

According to our channel checks, the number of new brokerage accounts has also significantly increased.

So far, the demand for margin loans has lagged behind, indicating that this round of rise is more likely driven by funds from new investors.

Despite the stock market rise, significant outflows were seen last week in major brokerage ETFs (investors primarily institutional). Retail investors usually prefer to directly buy brokerage stocks to chase market returns.

Morgan Stanley believes that the growth of household financial assets has provided ample potential liquidity for the Chinese stock market, so retail investors have sufficient capacity to sustain the current uptrend.

In 2022 and 2023, Chinese household financial assets are expected to grow by an average of approximately 18 trillion RMB annually, but the proportion of stock allocation remains consistently low.

We estimate that if stock allocation in Chinese household assets returns to the levels of 2020-2021, there may be an inflow of 2-3 trillion RMB into the stock market.

The low interest rate environment in the past two years has limited households' investment choices. Currently, margin financing still has room for growth, reaching 1.39 trillion RMB, compared to approximately 1.9 trillion RMB in 2021.

According to Morgan Stanley's estimate, assuming a 25% rise in the stock market, the stocks in investors' hands will increase in value accordingly. In such a market environment, the demand for stocks by investors may increase, and the scale of capital inflow may reach 2.6 trillion RMB.

The Super Upside Potential of Brokerage Stocks

The report also mentioned that in a market largely driven by retail investors, brokerage stocks often exhibit a trend of super upsides. The valuations of Hong Kong brokerage stocks are currently higher than the levels in 2020 and 2021, but the momentum of retail investors may still drive them even higher.

Morgan Stanley believes that based on the current valuations of Hong Kong brokerage stocks, the market may have already factored in an approximate daily trading volume of 1.4 trillion RMB as the running rate, with the industry's return on equity (ROE) rebounding to low double-digit levels.

Analysts believe that if investors consider the recent high average daily trading volume as the norm, then brokerage stocks may experience a short-term super upside.

If the momentum is strong enough, we believe that retail investors may consider 2 trillion RMB (the ADT in the two days before the A-share market closed) as the running rate, which could further increase the (brokerage stocks') earnings by 30%, with the ROE potentially reaching around 13%.

Nevertheless, considering the reduced contribution from brokerage business, declining commission rates, and increased capital intensity, Morgan Stanley believes that the valuations of brokerage stocks are unlikely to reach the level of over 2 times the pb ratio seen in 2015.

Editor/Rocky