CICC stated that during the holiday period, Hong Kong stocks and Chinese concept stocks continue to surge, with accelerated inflow of passive foreign capital, but the proportion of existing stock scale is not large; there is a certain overdraft of trading-type funds, with active foreign capital turning into inflow this week, but the scale is not significant yet, and the subsequent trends of active foreign capital are worth attention. However, their continued inflow requires more policies and more optimistic expectations to drive.

This week, the noteworthy changes in global liquidity are: 1) The EPFR fund data we track shows that as of Wednesday of this week (October 2nd), overseas active funds turned into net inflow for the first time after 65 consecutive weeks of outflow, and passive funds accelerated significantly inflow; 2) Regarding the Stock Connect, only on Monday of this week, the average daily size of northbound transactions and southbound inflows increased; 3) Global stocks, bonds, and currency markets all maintained inflows; 4) Japan accelerated outflows, India turned to outflows, and emerging markets saw narrowing outflows.

In the domestic market, during the holiday period, Hong Kong stocks and Chinese concept stocks continued to soar. Which foreign funds are the main participants in the inflows? With the A-share market closed during the National Day holiday and only trading on Monday through the Stock Connect, it provided a good window for analyzing overseas fund flows with controlled variables. Hong Kong stocks surged this week, supported by foreign inflows, but analyzing which ones are the main inflows is key to determining the sustainability of the market and subsequent market performance. Compiling data from various sources, we found:

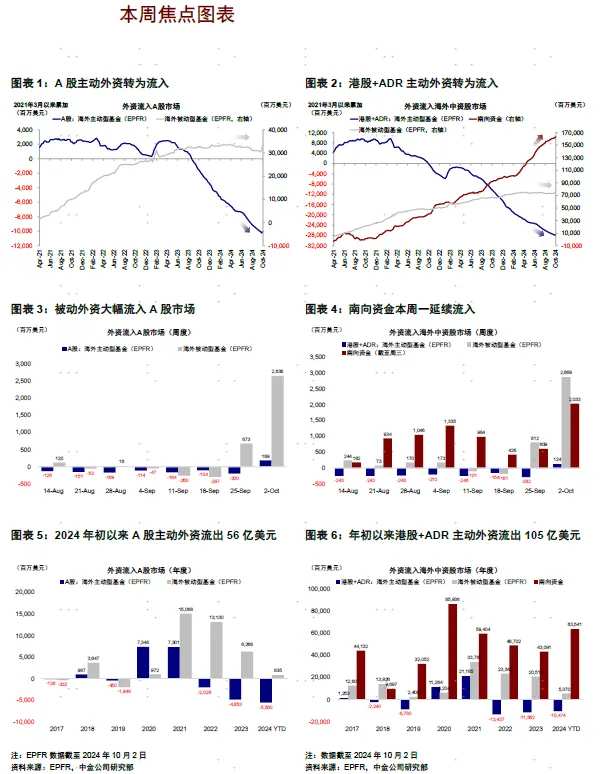

1) Passive foreign funds accelerated their inflows, but the proportion of existing funds is not significant. As of Wednesday of this week (September 26th to October 2nd), passive foreign funds flowed into A-shares with 2.64 billion US dollars, Hong Kong stocks and ADR with 2.87 billion US dollars, a volume that is 3-4 times that of the previous week, and hitting a new high since 2016. The main investments were in China, with inflows from funds investing globally not significant. Passive foreign funds have been flowing in since last week, mainly through ETFs by non-institutional investors, and based on statistics from MSCI and other channels, passive funds account for only 20% of the total, not a significant portion.

1) Passive foreign funds accelerated their inflows, but the proportion of existing funds is not significant. As of Wednesday of this week (September 26th to October 2nd), passive foreign funds flowed into A-shares with 2.64 billion US dollars, Hong Kong stocks and ADR with 2.87 billion US dollars, a volume that is 3-4 times that of the previous week, and hitting a new high since 2016. The main investments were in China, with inflows from funds investing globally not significant. Passive foreign funds have been flowing in since last week, mainly through ETFs by non-institutional investors, and based on statistics from MSCI and other channels, passive funds account for only 20% of the total, not a significant portion.

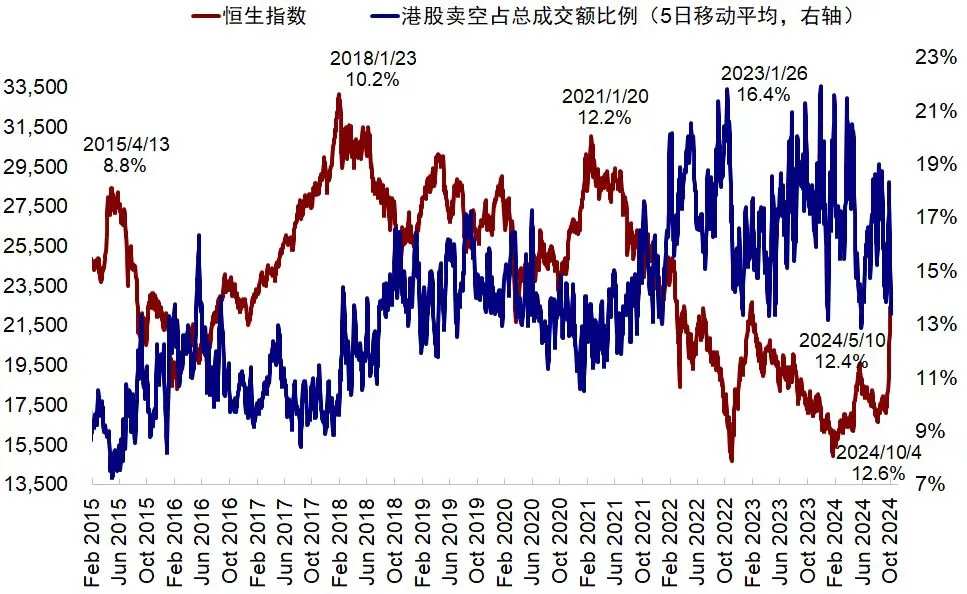

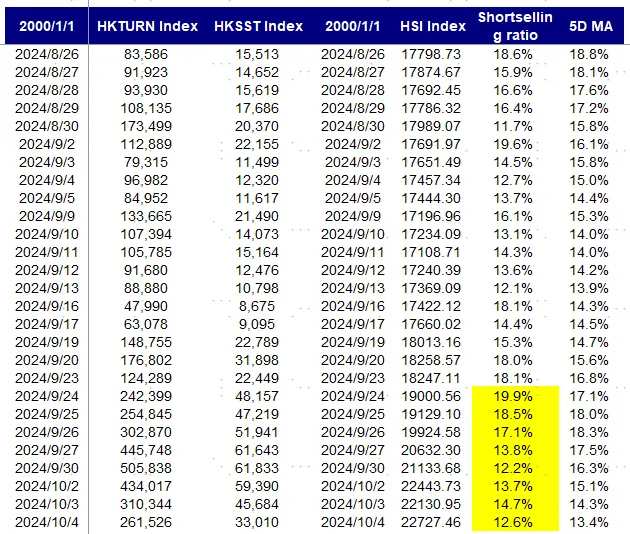

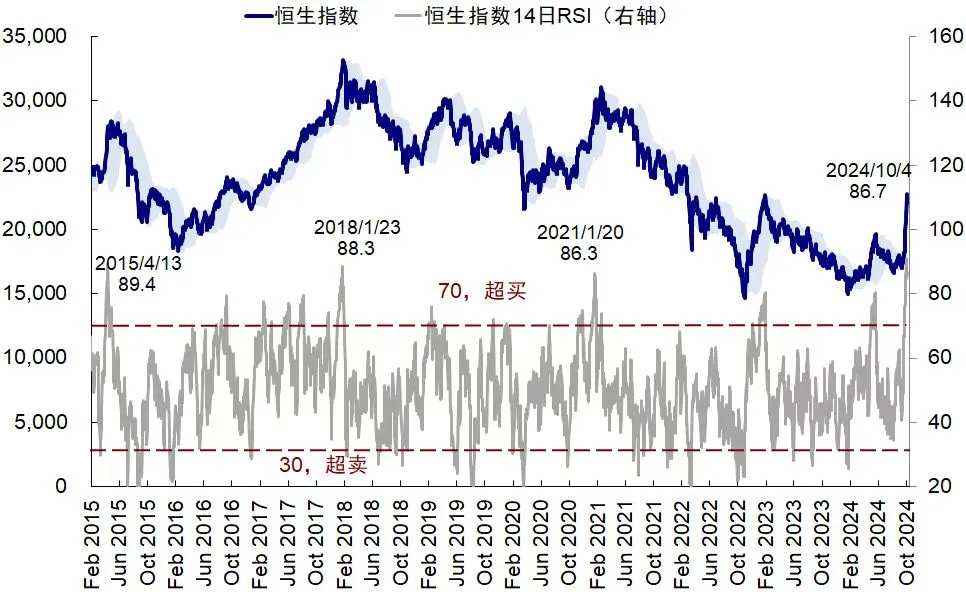

2) Trading funds are somewhat overdrawn. Trading funds were previously the main inflows, but recently short selling transactions in Hong Kong stocks as a percentage of total turnover fell from 17.5% of the 5-day moving average last week to 13.4%. The Hang Seng Index fell to 86.7 on the 6th, indicating the market is still overbought and somewhat overstretched. We speculate that hedge funds may have been forced to cut positions, so they might not be the main inflows again.RSI3) Active foreign funds turned into inflows this week, but the scale is not significant yet. Active foreign funds account for 80%, much larger than passive funds, thus more important and representative of long-term institutional investors. This week, actively managed funds flowed into A-shares with 0.19 billion US dollars, into Hong Kong stocks and ADRs with 0.12 billion US dollars, although the scale is small, it marks the first time turning into net inflow after 65 consecutive weeks of outflows since the end of June 2023. Regionally, the main focus is on funds investing in China and Asia, with no inflows from funds investing in emerging markets and globally. This is likely due to our speculation that some active funds, due to the continued market surge, are forced to reduce underweight positions to prevent excessive underperformance. The future trends of active foreign funds are worth paying attention to, but sustained inflows will require more policy support and more optimistic expectations. As of the end of August, global active fund allocation to Chinese stocks was 5% (peak at the beginning of 2021 was 14.6%), underweight by 1 percentage point. We estimate that if shifting from underweight to benchmark weight, it would lead to an inflow of nearly 40 billion US dollars, equivalent to the total outflows since March 2023.

Active foreign capital reversed to inflow this week, but the scale is not significant yet. Active foreign capital accounts for 80%, much higher than passive funds, therefore, it is more important and represents long-term institutional investors. This week, overseas active funds turned into inflow of $0.19 billion in A shares, inflow of $0.12 billion in Hong Kong shares and ADR, although the scale is small, it is the first net inflow after continuous outflows for 65 weeks since the end of June 2023. In terms of regions, funds mainly invested in China and Asia, while funds investing in emerging markets and global have not flowed in yet. This may be related to our speculation that some active funds are forced to reduce underweight positions to prevent too much underperformance as the market continues to surge. The future trends of active foreign capital are worth paying attention to, but sustained inflows require more policies and more optimistic expectations to drive them. As of the end of August, global active funds allocated 5% to Chinese stocks (the high point at the beginning of 2021 was 14.6%), underweight by 1 percentage point. We estimate that if the underweight is converted to neutral, it would correspond to an inflow of nearly $40 billion, equivalent to the total outflows since March 2023.

On a global basis, the outflow of US stocks slowed down, while Japanese stocks accelerated their outflow, and the Indian market shifted to outflow. As of this Wednesday (September 26th-October 2nd), the Indian market saw active foreign capital shift to an outflow of 0.05 billion US dollars (compared to an inflow of 0.16 billion US dollars last week), the outflow of US stocks narrowed to 0.12 billion US dollars this week (compared to an outflow of 0.22 billion US dollars last week), and Japanese stocks accelerated their outflow to 1.13 billion US dollars (compared to an outflow of 0.19 billion US dollars last week).

In the Chinese market: active foreign capital shifted to inflows, while passive inflows increased; the Shanghai-Hong Kong Stock Connect only opened on Monday.

Overseas funds: EPFR shows active foreign capital shifting to inflows. As of this Wednesday (September 26th-October 2nd), A-share active foreign capital shifted to inflows of 0.19 billion US dollars (compared to an outflow of 0.2 billion US dollars last week), passive funds saw a significant inflow of 2.64 billion US dollars (compared to an inflow of 0.67 billion US dollars last week); at the same time, Hong Kong stocks and ADR overseas funds overall accelerated inflows of 2.99 billion US dollars (compared to an inflow of 0.53 billion US dollars last week), with active funds shifting to an inflow of 0.12 billion US dollars (compared to an outflow of 0.28 billion US dollars last week), and passive funds saw a significant return flow of 2.87 billion US dollars (compared to an inflow of 0.81 billion US dollars last week).

Stock Connect Funds: Northbound funds ceased disclosing net purchase amounts since August 16th, with the average daily turnover expanding this week. The Stock Connect opened only on Monday this week, with Northbound funds achieving a turnover of 356.9 billion yuan, an increase from the previous week's daily average turnover of 162.6 billion yuan. In terms of individual stocks, Kweichow Moutai, Zijin Mining, China Yangtze Power, Ping An Insurance, and CM Bank were the most actively traded symbols.

Southbound funds accelerating inflows, with the Consumer and Diversified Finance sectors seeing the highest inflows. On September 30th, there was an inbound flow of 12.14 billion Hong Kong dollars (compared to an average daily inflow of 0.48 billion Hong Kong dollars last week). At the industry level, the Consumer and Diversified Finance sectors received the most Southbound funds last week, while Mainland banks and Energy/Material sectors overall saw outflows. In terms of individual stocks, according to daily disclosures of the top 10 most active stocks through the Hong Kong Stock Connect, Southbound funds favored symbols such as Alibaba and HKEX the most on Monday, while selling off symbols like Meituan-W, Tencent, CNOOC, and CM Bank.

Global markets: Global equities, bonds, and currency markets all saw inflows; Developed Europe and Japan witnessed accelerated outflows, while outflows from emerging markets slowed down.

Across markets and assets: US stocks continued to see outflows, with outflows expanding in Developed Europe and Japan while narrowing in emerging markets. Looking at active foreign capital, US stocks saw outflows of 0.122 billion US dollars this week (compared to 0.219 billion US dollars last week), Developed Europe witnessed accelerated outflows of 2.468 billion US dollars (compared to 0.442 billion US dollars last week), the Japanese stock market saw accelerated outflows of 1.128 billion US dollars (compared to 0.194 billion US dollars last week), and the outflow size from emerging markets narrowed to 0.25 billion US dollars (compared to 0.723 billion US dollars last week). Overall, inflows to global equities and currency markets have narrowed, while the bond market has seen accelerated inflows.

Allocation Ratios: As of August 31st, the allocation ratio of actively managed funds globally to China was lower than the benchmark by about 0.1%. From 2022 to date, actively managed funds globally have shifted from being overweight in China and India to underweight, with South Korea still maintaining an overweight position and Japan seeing a slight decrease in underweight. Since January 2022, the allocation ratio to China has decreased the most (-0.2%), while the UK (+1.8%), France (+0.5%), and Japan (+0.3%) have seen the largest increases. In terms of regional types, funds from Europe have been the main outflow drivers overall; at the sector level, overseas funds are overweight in Chinese medical care, consumer, semiconductors and hardware, and capital goods, while being underweight in internet, finance, and real estate.

Editor/Somer