Foreign capital is an important incremental fund for the current rise in the Hong Kong stock market, preferring the consumer and information technology sectors.

Since the Fed confirmed easing in mid-September, the Hong Kong stock market has ushered in a broad and epic rally, with the Hang Seng Tech Index soaring by 36.6% in just half a month. On October 2, the first trading day after the National Day holiday, with the absence of southbound funds, the Hong Kong stock market surged, with the Hang Seng Index closing up by 6.2% and the Hang Seng Tech Index up by 8.53%.

During the 'absence' of southbound funds, who is entering the Hong Kong stock market? Which sectors do incremental funds prefer? How much incremental funds could still enter the market in the future? Institutions have analyzed these in their latest research reports.

Foreign capital is an important incremental fund for the recent rise in Hong Kong stocks.

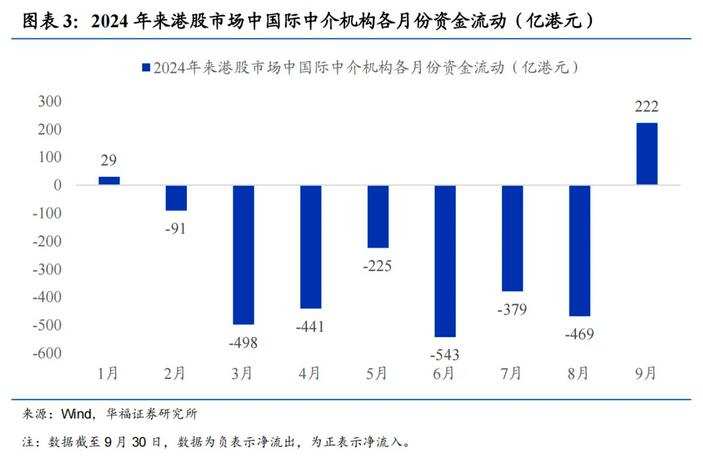

Huafu Securities stated that in September, after consecutive months of continuous outflow of international intermediary funds from the Hong Kong stock market, they have once again turned into net inflows, becoming an important source of incremental funds for the market.

Huafu Securities stated that in September, after consecutive months of continuous outflow of international intermediary funds from the Hong Kong stock market, they have once again turned into net inflows, becoming an important source of incremental funds for the market.

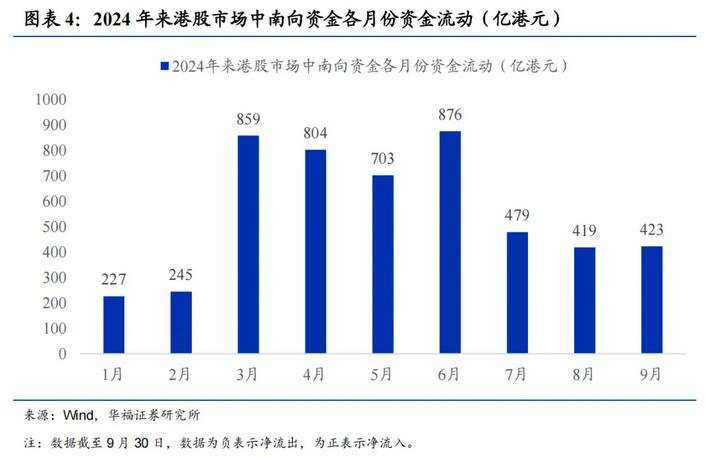

Since the outbreak of the pandemic in 2020, there has been a significant change in the structure of incremental funds in the Hong Kong stock market. On one hand, overseas funds represented by international intermediaries have been continuously withdrawing from the Hong Kong stock market, while on the other hand, mainland funds represented by southbound funds have been continuously flowing into the market. However, the latest marginal changes show an interesting phenomenon where since September, overseas funds in the Hong Kong stock market have turned into net inflows, with international intermediary institutions seeing a net inflow of 39.6 billion Hong Kong dollars since mid to late September, exceeding the net inflow of southbound funds by 20.5 billion Hong Kong dollars.

Similarly, some institutions point out that the return of foreign capital in the allocation plate (especially passive index-type foreign institutions) has played an important role in the capital aspect.

Firstly, according to EPFR, from September 19th to 25th, passive index-type foreign capital had a net inflow of 1.8 billion US dollars into Chinese equity assets, showing a significant increase (note that this data only covers the two trading days after the '924' policy combination).

Secondly, since late September, with the rise of Chinese assets, other emerging markets have experienced volatile market conditions, which may reflect foreign capital re-balancing within emerging markets.

Thirdly, in the past month, the proportion of short selling transactions in the Hong Kong stock market has significantly decreased, mainly due to the increase in long trading amount, and as of September 30, the marginal change in the number of outstanding unsettled shares is not significant compared to September 23.

Foreign capital prefers consumer and technology sectors.

Huafu Securities pointed out that the significant inflow of foreign capital into the Hong Kong stock market since the middle and late September is an important reason for the dominance of the Hang Seng Tech Index.

In the Hong Kong stock market, international intermediaries prefer the consumer and information technology sectors, which are also important components of the Hang Seng Tech Index. From this perspective, we believe that the rapid inflow of international intermediary funds since the middle and late September is a key factor in the outperformance of the Hang Seng Tech Index. As of September 30, the international intermediaries in the Hong Kong stock market had a 30% stake in the consumer industry and a 25% stake in the information technology sector, far higher than other industries. The information technology sector accounts for 50% and the consumer sector accounts for 49% in the Hang Seng Tech Index, also much higher than the 19% and 35% in the Hang Seng China Enterprises Index. Therefore, we believe that the significant capital inflow of foreign capital into the Hong Kong stock market since the middle and late September is a key reason for the dominance of the Hang Seng Tech Index.

Two major sources of future incremental funds.

HTSC estimates that future incremental funds in the Hong Kong stock market may come from the replenishment effect of foreign capital and the closing effect of short positions:

First, the global inflow effect of foreign capital; as of the end of the second quarter, the world's top twenty asset management institutions (includingMutual fundsIn the equity portfolios of hedge funds, reits, etc., the proportion of Chinese stocks is 1.3%, which is underweight by 1.9 percentage points compared to the MSCI ACWI China benchmark weight; if there is an expected improvement, foreign investment may return to the allocation level in the first quarter (underweight by 1.7%), potentially bringing about a net inflow of around $17 billion from top asset management institutions; if it returns to the central level of 2018-2020 (underweight by 0.5%), it may bring about a net inflow of around $100 billion.

Secondly, there is the effect of unwinding existing short positions; although the proportion of short selling in Hong Kong stocks has been at a historically low level since September, the number of outstanding short positions in the entire market has not yet significantly declined, and the force of unwinding existing short positions has not been adequately released.

Huafu Securities also believes that the impressive performance of Chinese assets represented by Hong Kong stocks recently is the result of multiple factors working together. On the one hand, domestic favorable policies have been frequently introduced, greatly boosting market confidence; On the other hand, the Federal Reserve cut interest rates in September, leading to a more lenient global liquidity environment. In the initial stages of the Fed rate cut, global equity markets typically benefit from the denominator logic seeing overall good performance. Therefore, overall, we believe that the current situation in the Hong Kong stock market is still in progress, and there is still room for further upside. Structurally, if the follow-up inflow of intermediaries funds in the Hong Kong stock market continues, growth sectors represented by the Hang Seng Tech Index may continue to perform well.

Editor/Somer