而这一方面表明先前采取市场中性策略的机构的仓位部署中的看跌期权持仓正在迅速爆仓,另一个那面,投资者大量涌入看涨期权市场,以在短期内迅速博取投机收益。

而这一方面表明先前采取市场中性策略的机构的仓位部署中的看跌期权持仓正在迅速爆仓,另一个那面,投资者大量涌入看涨期权市场,以在短期内迅速博取投机收益。Last week, everything about the Chinese stock market seemed to have changed. Looking at the international markets, the Wall Street investment banks and hedge fund institutions, who have long been cautious about the Chinese stock market, suddenly turned overwhelmingly bullish on Hong Kong stocks and A-shares, with a collective voice of "long China" echoing through Wall Street.

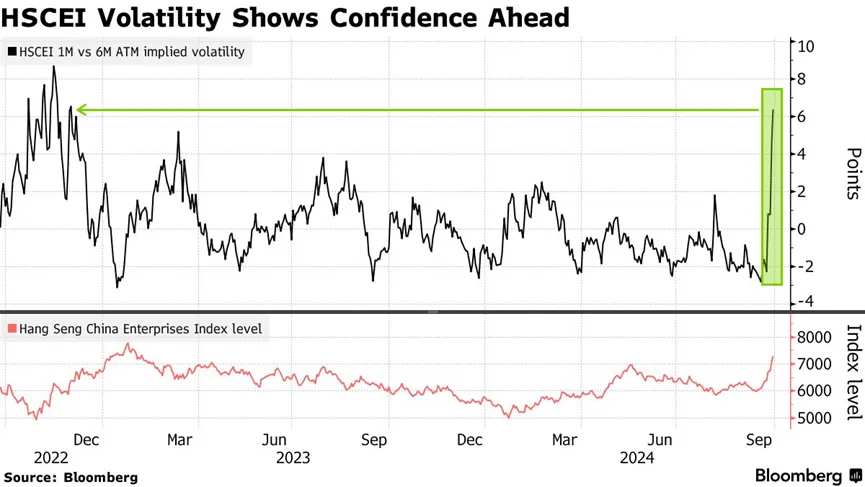

It is worth noting that market participants, especially foreign institutional investors, actively chased the rise through call options, leading to the sharp increase in the Hang Seng Volatility Index in the Hong Kong stock market to a new high in the past two years. As of the close on September 30, the Hang Seng Volatility Index closed at 32.56, reaching a high of 34.87 during the session. This is the highest level since December 2022.

The Hang Seng Volatility Index reflects the overall cost of the options market in the Hong Kong stock market. The volatility rate has significantly increased in the short term, indicating that options (whether call or put options) are rapidly becoming expensive. The fact it reflects is the high enthusiasm of investors or financial institutions seeking options as short-term chasing tools.

On one hand, this indicates that the institutions that previously adopted market-neutral strategies are rapidly unwinding their put options positions, while on the other hand, a large number of investors are flocking to the call options market to quickly gain speculative profits in the short term.

On one hand, this indicates that the institutions that previously adopted market-neutral strategies are rapidly unwinding their put options positions, while on the other hand, a large number of investors are flocking to the call options market to quickly gain speculative profits in the short term.

1. Policy shift exceeds expectations

The collective excitement of institutional investors is due to the rapid policy shift by the Chinese government in the economic field, far exceeding the expectations of almost all market participants.

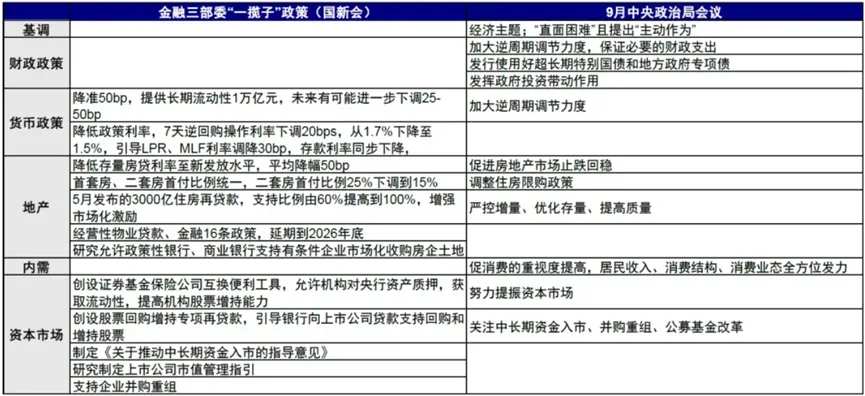

Since the central bank's reserve requirement ratio cut on September 24, the Chinese government has taken a series of stimulus measures that far exceed expectations in just a few days, covering everything from consumer spending to the real estate market and the stock market. For example, in terms of monetary policy, interest rates were cut by 20bp, 7-day reverse repurchase operation rates were reduced by 20bp, reserve requirement ratio was cut by 50bp, providing long-term liquidity of 1 trillion yuan. Depending on the liquidity situation, there may be further cuts of 25-50bp.

Regarding real estate, the down payment ratio was reduced to 15%, with the down payment ratio for first and second homes being unified, and the down payment ratio for second homes was reduced from 25% to 15%, lowering the threshold for residential mortgage loans; reducing the existing mortgage rates to the level of new loans, with an average reduction of 50bps. Pan Gongsheng stated that it is expected to help an average of 50 million families reduce their interest expenses by 3000 yuan per year, while also easing the pressure on residents to repay loans in advance.

The political bureau meeting clearly stated the stable real estate prices, for the first time putting forward the goal of 'promoting the stabilization of the real estate market', greatly exceeding market expectations, policies connecting the real estate demand and supply side may accelerate.

On the stock market side, the central bank has created two new structural monetary policy tools to stabilize stock prices, one is the convenient tool for securities, fund and insurance companies to exchange, and the other is a special refinancing for share buyback and increased holdings. These two tools are estimated to provide the market with incremental funds of 800 billion to 2.4 trillion yuan.

In addition, the political bureau meeting's statements regarding fiscal policy, and the inclination towards people's livelihood and consumption areas, conveyed a slightly different approach and signals compared to the past, if implemented, it will have a greater impact.

Just this past Sunday, the three major first-tier cities of Shanghai, Shenzhen, and Guangzhou collectively introduced new real estate policies, further relaxing purchase restrictions. For example, Shanghai implemented the 'Seven Policies of Shanghai', reducing down payment ratios, reducing inventory housing loans, and allowing non-local residents to purchase a house after 1 year of social security contributions; Guangzhou lifted various purchase restrictions for resident families buying homes in the city; Shenzhen adjusted the minimum down payment ratio for first-time commercial individual housing loans to 15%, and for the second home to 20%.

On the same day, the timing for lowering existing housing loan rates was specified, and a market interest rate pricing self-discipline mechanism initiative was issued, requiring all commercial banks to uniformly adjust the rates for existing housing loans (including first, second, and subsequent homes) to be no less than 30 basis points lower than the LPR by October 31, 2024.

These developments further confirm the expectations of further policy relaxation, keeping the market bullish. Like today the Hang Seng Index in Hong Kong broke through the 21,000 point mark, reaching a high of 21,488 during the day, the highest point since February 2023. The Hang Seng Tech Index surged by 6.7%, reaching a high of 4841 during the day, aiming for 5000 points.

As for A-shares, the SSE Composite Index surged by 8.06%, breaking through the 3300 point mark, the Shenzhen Component Index increased by 10.67%, and the ChiNext Price Index rose by 15.36%. With this, the three major A-share indexes have completely recovered from the decline since May 2023.

"It seems that this time the government departments feel the urgency," said Michael Oh, investment portfolio manager at Matthews Asia from San Francisco. "If investors believe that the Chinese government will continue to strongly support the market, then the rebound may continue. The valuation of the Chinese market is indeed too cheap."

Institutions are pouring into the options market.

With the sharp rise of the Chinese stock market (including Hong Kong stocks and A shares), the cost of hedging protection against the 'China Enterprise Benchmark Index' falling has dropped to the cheapest level since 2015. This reflects that the cost of put options will be at its lowest level since 2015, which means the number of investors using put options to hedge market downside risks is rare or almost non-existent.

It is worth noting that the cost of downside hedging protection reached its lowest level during the super bull market in 2015, and it reached its highest level during the period of the most intense decline in Hong Kong stocks in 2020 during the pandemic and in 2022. Currently, it is similar to 2015, indicating that the market generally believes that the likelihood of a decline is small and there is no need to hedge with put options. At the same time, the bears who previously bet on further declines in Hong Kong stocks may incur their highest losses in over a decade.

At the same time, the number of call contracts in the Chinese stock market has reached its highest level since June relative to the number of put contracts, indicating that the bullish sentiment in the market has become very strong, even possibly 'frenzied.' An increasing number of foreign investment institutions focusing on the Chinese stock market choose call options for leveraged profit without hedging the downside risk of the stock market.

For example, in the USA, top institutional investors including billionaire David Tepper are frantically buying Chinese stock assets, and the trading volume of call options on exchange-traded funds (ETFs) tracking some Chinese stock market benchmark indices has surged. In the U.S. stock market, there is an extreme trend of bullish trading in short-term contracts around Chinese companies' American Depositary Receipts.

Other bullish forces are continuously rolling over their call option spread positions by extending the expiration dates, allowing investors to continue their trades rather than closing or settling the options that are about to expire or close to expiration. They may also control costs or lock in profits through option spread strategies.

A call option spread strategy refers to an investor buying and selling call options with different strike prices. With this strategy, investors can limit potential risks. Because selling options can partly offset the cost of buying options, but it also limits the profit potential.

Mark Franklin, Senior Portfolio Manager of Asset Allocation at Manulife Investment Management, said that while people's concerns persist in the long run, investors are generally optimistic about their investments now. 'Since the proportion of global funds allocated to the Chinese stock market is still relatively low, we expect significant short-term rebounds in Hong Kong stocks and A shares, which may trigger a sharp rebound caused by massive short covering.'

Of course, among the investors who are crazy about chasing highs, there are also rational voices. For example, Chris Murphy, co-head of derivative strategy at Susquehanna International Group, warned that if the uptrend gradually disappears, the sudden surge in the volatility of call options could instantly reverse.

Chris Murphy believes that investors hoping to hedge this move by buying put options should also be very cautious, as prices fall but implied volatility levels are also decreasing, severely limiting the profit from buying put options even if the underlying asset price falls. He stated that buying put option spreads, protective collar strategies, or reducing risk exposure hedging options strategies make more sense.

How about the future market outlook?

As of the close of September 30, the Hang Seng Index's 6-day RSI (Relative Strength Index) has reached 96.5, the highest since the end of 2018, and the SSE Composite Index has also reached 94.1. In terms of RSI, generally above 70% indicates market strength, while over 80% implies some 'overbought' signals, and exceeding 90% means extremely overbought.

"Overbought" conditions persist, meaning the market has accumulated a large amount of profits, and once any slight disturbance occurs, even if these investors remain optimistic for the medium to long term, they will choose to take profits in the short term, causing the market to further lose momentum or experience a short-term pullback. Until technical indicators return to normal and the next market trend is brewed.

Unlike before, market statistics show that with the market rise, the proportion of short selling continues to increase, indicating that there are still some divergences in the market's future trends. So the question people care about is, after experiencing multiple consecutive days of sharp rises last week and the last trading day before the holiday, how much room is left for the future?

Regarding the outlook for the future market, China International Capital Corporation believes that in the short term, distressed state-owned enterprises and previously oversold sectors are still the direction of the market rebound. From a medium to long-term perspective, attention should be paid to the subsequent realization of policy expectations, whether they continue to exceed expectations, meet expectations, or even fall short of expectations.

In the short term, central bank financial innovation tools may directly benefit distressed enterprises, especially state-owned enterprises. On the other hand, lagging sectors such as internet software (-24.8% since the beginning of 2024), food retail (-16.6%), and medical service equipment (-14.8%) may also be the direction of speculative rebounds driven by emotions.

In the medium to long term, if policies continue to be fulfilled and fiscal stimulus exceeds expectations, pro-cyclical sectors directly benefiting are expected to outperform, including consumer, real estate chain, non-bank financials, etc. In addition, attention should be paid to interest-rate sensitive growth stocks (internet, technology growth, biotechnology, etc.), local dividends and real estate in the Hong Kong stock market, as well as export chains driven by US real estate demand.

However, if fiscal stimulus is insufficient or slower than expected, the market may need to digest through volatility. In this scenario, CICC believes that high dividends still have long-term allocation value and can be opportunistically entered during recent corrections. Additionally, certain sectors supported by policies or showing positive economic trends are still expected to benefit from bullish sentiment and demonstrate significant resilience, such as those with inherent industry vitality (internet, gaming, education), or technology growth supported by policies (technology hardware and semiconductors).

Overall, as October approaches with the US election and third-quarter earnings season nearing, volatility in the US stock market is expected to increase, making a correction seemingly unavoidable. On the contrary, Chinese assets in the Hong Kong and A-share markets are currently at historically low levels, with policy support for market stabilization at an all-time high. Comparatively, the value proposition of Hong Kong and A-shares is undoubtedly higher.

Editor/new