在短短几天内,中国政府采取一系列超预期的刺激措施,从消费支出到房地产市场以及股票市场,可谓无所不包。港股基准指数——恒生指数全年涨幅勉强达到22%,实现连续11天大举反弹,这是自2018年辉煌时期以来该港股指数持续最长的一次上涨。

在短短几天内,中国政府采取一系列超预期的刺激措施,从消费支出到房地产市场以及股票市场,可谓无所不包。港股基准指数——恒生指数全年涨幅勉强达到22%,实现连续11天大举反弹,这是自2018年辉煌时期以来该港股指数持续最长的一次上涨。l stocks ETFs in the US also saw a significant increase in call options volume.

The Wall Street hedge funds have turned optimistic about the Chinese stock market, especially the institutions holding high-leverage derivative options. The Chinese government announced a combination of stimulus measures far beyond expectations last week, driving Hong Kong stocks to achieve the largest weekly gain in nearly 13 years. It is expected to become one of the best-performing stock markets globally in 2024. The A-share Shanghai Composite Index soared last week from 2700 points to the long-term challenging level of 3000 points.

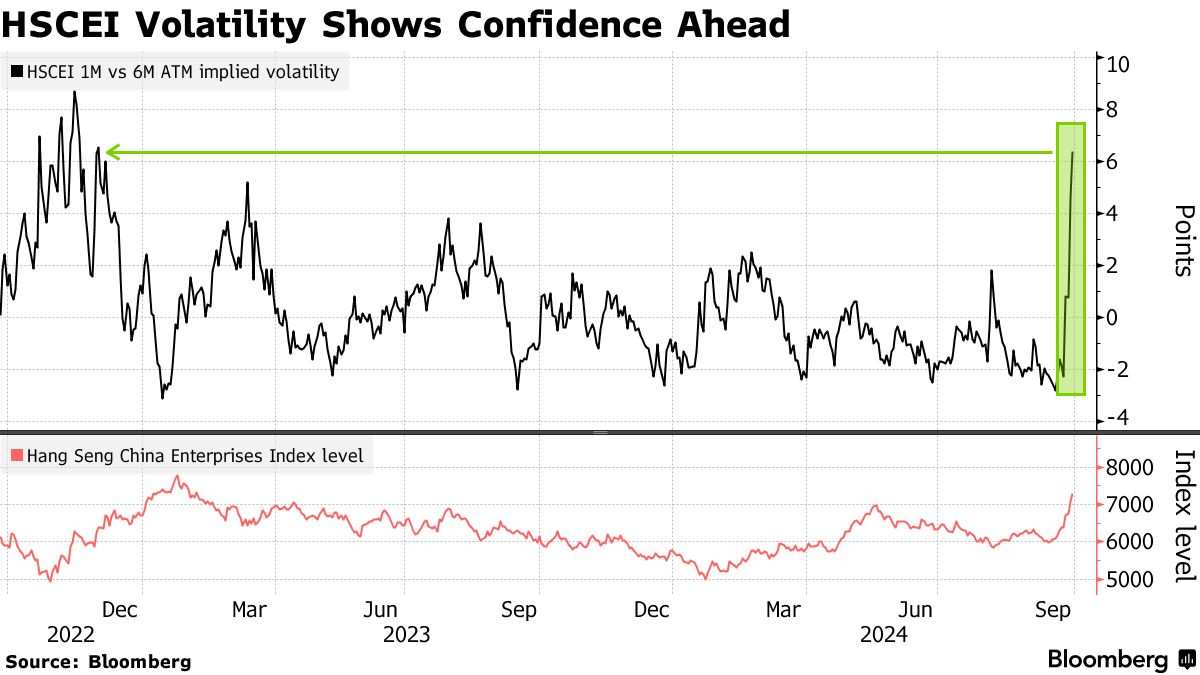

It is worth noting that market participants, especially foreign institutions, actively chased after the bullish options derivative, leading to a surge in the volatility hedging costs of Hong Kong stocks for the next month compared to the six-month contract level, hitting a two-year high. This indicates that investors are increasingly confident in at least the medium term, but also suggests significant losses for funds shorting the Chinese stock market and seeking 'neutral hedging' strategies. Some institutions even faced forced liquidation. If investors short the Chinese stock market in the short term or use neutral hedging strategies (such as holding long positions while buying put options), these strategies may suffer significant losses due to the recent market frenzy.

Within a few days, the Chinese government implemented a series of stimulus measures beyond expectations, covering everything from consumer spending to real estate and the stock market. The Hang Seng Index, a benchmark index in Hong Kong, barely achieved a 22% annual increase, marking an 11-day consecutive rebound, the longest continuous rise since the glorious period of 2018.

Within a few days, the Chinese government implemented a series of stimulus measures beyond expectations, covering everything from consumer spending to real estate and the stock market. The Hang Seng Index, a benchmark index in Hong Kong, barely achieved a 22% annual increase, marking an 11-day consecutive rebound, the longest continuous rise since the glorious period of 2018.

The abundant 'water' provided by monetary policy and convenient liquidity, together with the established tone of fiscal stimulus, enabled the Shanghai Composite Index to recover from the temporary low point of 2689 to the seemingly insurmountable level of 3000 in just 7 trading days. The A-share benchmark index, the CSI 300 Index, surged over 15% this week with an outstanding bullish trend.

In the Hong Kong stock market, the optimistic sentiment of envisioning a 'long bull market' has intensified. Benefiting from the unexpected 50 basis point rate cut by the US Federal Reserve initiating a rate-cut cycle, and the liquidity support provided by domestic monetary stimulus policies, Hong Kong stocks have enjoyed the 'dual liquidity dividend' from China and the US. Under the influence of many favorable catalysts such as domestic sales promotion fees and policies promoting private sector development, the Hang Seng Tech Index surged by over 20% this week, while the Hang Seng Index rose by over 13%. By the end of this week's trading, the Hang Seng Index had accumulated a 21% increase year-to-date, surpassing the S&P 500 Index's approximately 20% annual gain.

"It seems this time the government departments feel the urgency," said Michael Oh, a portfolio manager at Matthews Asia in San Francisco. "If investors believe that the Chinese government will continue to strongly support the market, then the rebound may continue, and the valuation of the Chinese market is indeed too cheap."

Last week, everything about the Chinese stock market seemed to have changed. Looking at the international markets, the Wall Street investment banks and hedge fund institutions, who have long been cautious about the Chinese stock market, suddenly turned overwhelmingly bullish on Hong Kong stocks and A-shares, with a collective voice of "long China" echoing through Wall Street.

The Chinese government reduced benchmark interest rates, bank reserve requirements, and various borrowing costs, promising billions of dollars to boost the Chinese stock market. They also announced relief funds to stimulate consumer spending, and made explicit the top-level policy orientation to boost the private economy, stimulate consumption vigorously, comprehensively improve residents' income, and even support local milk production.

With the significant rise of the Chinese stock market (including Hong Kong and A-shares), hedging protection against the 'Chinese Enterprise Benchmark Index' decline has become the cheapest scale since 2015. The data reflects the market generally believing in the small likelihood of a decline, investors' concerns about future market downturns weakening, and potential record losses for bearish positions in the Chinese stock market, especially in Hong Kong stocks, in over a decade. In the meantime, the number of bullish contracts on the Chinese stock market has reached its highest level since June, compared to the number of bearish contracts.

Combining these two points, more and more foreign investment institutions focusing on the Chinese stock market are choosing to leverage profits with bullish options trading, without hedging against market downturn risks. This means the bullish sentiment in the market has become very strong, even potentially 'enthusiastic.' Investors are more inclined to bet on the market continuing to rise rather than preparing for a downturn risk.

In the USA, top institutional investors including billionaire David Tepper are aggressively buying Chinese stock assets. The trading volume of bullish options trading on ETFs tracking some Chinese stock market benchmark indexes has surged on US stock exchanges. In the US market, there is an extremely bullish trend in short-term contract trading on American Depositary Receipts of Chinese companies.

In the current Chinese stock market, bullish bets dominate. Some early option buyers choose to take profits later in the week, while other bullish forces roll positions with bullish option spreads, meaning investors move soon-to-expire or close-to-expire option positions to later expiration dates to continue their trades instead of closing or settling. However, they may control costs or lock in profits through option spread strategies. A bullish option spread refers to investors buying and selling two different strike price bullish options. With this strategy, investors can limit potential risks (as the sold option can partially offset the cost of the bought option) while also capping profits.

As the frenzy of call options trading around the Chinese stock market emerges, Chris Murphy, co-head of derivatives strategy at Susquehanna International Group, warns that if the uptrend gradually fades, the sudden surge in call options volatility may reverse instantly.

"In my view, investors hoping to hedge this move by buying put options should also be very cautious, as prices fall but implied volatility levels are also decreasing, severely limiting the profits from buying put options even if the underlying asset price falls." Chris Murphy added that buying put options spreads, protective collar strategies, or reducing risk exposure hedging options strategies make more sense.

Mark Franklin, Senior Portfolio Manager in Asset Allocation at Manulife Investment Management, said that although concerns still exist in the long term, investors are generally optimistic about current investment. "Due to the relatively low global allocation of funds to the Chinese stock market, we expect significant short-term rebounds in Hong Kong stocks and A-shares, possibly triggering a sharp rebound caused by large-scale short covering."

Editor/ping