Mag 7股价近来表现突出,相关ETF本周上涨1.7%,过去三周更是大涨约12%。从Roundhill Mag7 ETF表现来看,Mag 7近期涨势几乎快要抹平前几个月的跌幅。

Mag 7股价近来表现突出,相关ETF本周上涨1.7%,过去三周更是大涨约12%。从Roundhill Mag7 ETF表现来看,Mag 7近期涨势几乎快要抹平前几个月的跌幅。The stock prices of the seven giant companies in the US have recently performed well, with related ETFs rising 1.7% this week, and even more significantly increasing by about 12% over the past three weeks. Analysis believes that the Mag 7 is still the powerhouse of the US stock market, and in a world full of uncertainties, investing in large companies seems to be a better choice.

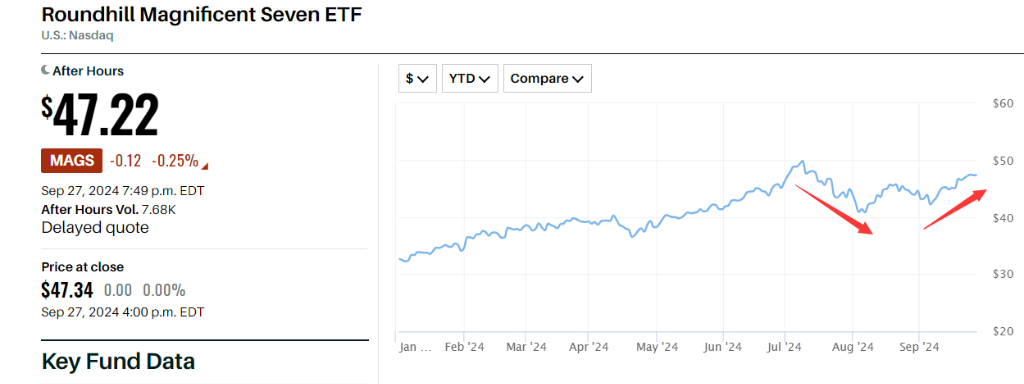

After experiencing sharp declines in July and August, the familiar Magnificent 7 is back again?

Currently, US technology stocks are picking up momentum again, with investors showing renewed enthusiasm for the Magnificent 7. On Friday, the S&P 500 index hit a new historical high, with technology stocks leading the gains.

The performance of Magnificent 7 stocks has been outstanding recently, with related ETFs rising by 1.7% this week and a significant increase of about 12% in the past three weeks. Looking at the Roundhill Magnificent 7 ETF performance, the recent surge of Magnificent 7 is almost erasing the declines of the past few months.

The performance of Magnificent 7 stocks has been outstanding recently, with related ETFs rising by 1.7% this week and a significant increase of about 12% in the past three weeks. Looking at the Roundhill Magnificent 7 ETF performance, the recent surge of Magnificent 7 is almost erasing the declines of the past few months.

Regarding the recent rise of the Magnificent 7, Barron's commented that we have already passed the stage of (technology stock frenzy). Over the past three months, investors' attention has shifted to the other 493 stocks in the S&P 500 index (small cap stocks). However, the continued rise of small cap stocks requires investors to believe that the significant rate cuts by the Federal Reserve are enough to prevent an economic recession.

But it seems that the economy has not gone that far at the moment. Meanwhile, the exacerbated geopolitical tensions in the Middle East have not helped improve the economy. In a world full of uncertainties, investing in large companies seems to be a better choice.

The report further points out that the sustained attraction of the Magnificent 7 may be another evidence of the extremely low market efficiency, as investors have ceased to price stocks in a rational manner.

AQR Asset Management partner Clifford Asness pointed out in a recent paper that from 1950 to the Internet bubble period (1995 to 2001), the stock market was relatively efficient, and this determination can be verified by comparing the price-to-book ratios of the most expensive large cap stocks and the cheapest stocks. Over a period of about 50 years, this ratio remained relatively stable until it surged during the Internet bubble period and rose again in the past decade, indicating that investors have ceased rational pricing.

Asness believes that the three reasons for the current market transformation are: indexing, long-term low interest rates, and new technologies driving the rise of retail traders, leading to 'retail investor frenzy stocks' such as GameStop far exceeding fair value. Asness's suggestion is to invest in 'value stocks.'

As the Fed's interest rate cuts kick off a global central bank easing cycle, European inflation continues to fall, and the People's Bank of China has launched a series of 'policy stimulus packages' to boost the international market, investors are beginning to reassess their investment portfolios and stock selection. The U.S. Magnificent 7 (Google parent company Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, Tesla) remain the powerhouse of the U.S. stock market.

The Mag 7 market has experienced ups and downs, with Wall Street bullish on the U.S. stock market.

In the first half of this year, the U.S. tech giants Mag 7 have been viewed as the key engine of U.S. stock growth. As of June, Mag 7 contributed to nearly 60% of the S&P 500 index's return. However, since July, this momentum has quickly stalled.

In July and August this year, the Mag 7 have seen varying degrees of significant declines. According to statistics, from July to early August, the market cap of Mag 7 plummeted by an astonishing nearly $2 trillion. In September, the downward trend of the Mag 7 stabilized somewhat, entering a phase of overall rebound.

Market analysts pointed out that the significant drop at that time was triggered by the huge investment of Mag 7 company in the AI field, leading to market doubts about its ability to realize returns. Funds began to flow into small cap stocks, and the market style subsequently changed. At the same time, due to the high market cap of Mag 7, the concentration of the US stocks hit a historical high. Deutsche Bank analyst Jim Reid stated that historically high valuations and concentration often accompany subsequent market adjustments.

After this recent decline, Mag 7 company's market cap still accounts for over 30% of the s&p 500 index.

However, the market outlook for the future trend of the s&p 500 index is optimistic, with Wall Street's highest target set at 6100 points. Some well-known sell-side institutions on Wall Street predict that the year-end target for the s&p 500 index ranges from a low of 4200 to a high of 6100.

In addition, Goldman Sachs found that from 1996 to 2023, the average daily trading volume of stocks and options peaks in October. Since October is the earnings season, listed companies typically manage their performance up to the end of the year and provide guidance for the next year's performance, making the next few weeks a crucial period for trading activity.