Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Hologic, Inc. (NASDAQ:HOLX) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

What Is Hologic's Net Debt?

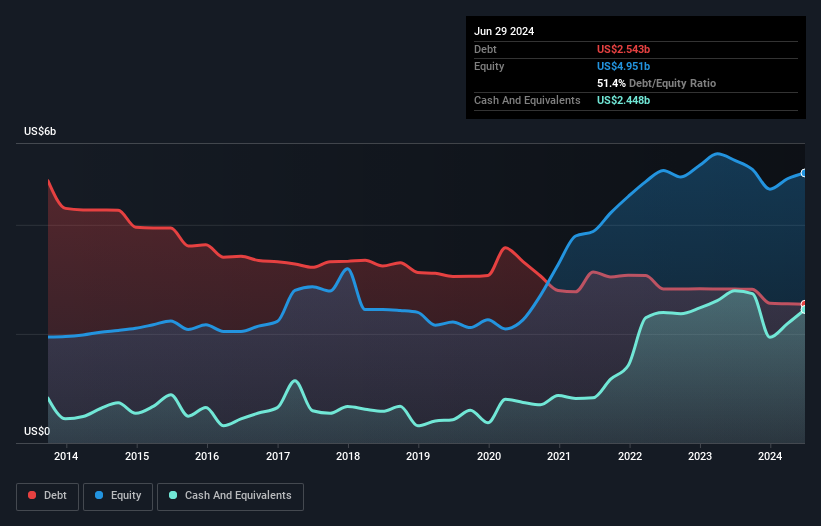

The image below, which you can click on for greater detail, shows that Hologic had debt of US$2.54b at the end of June 2024, a reduction from US$2.82b over a year. However, because it has a cash reserve of US$2.45b, its net debt is less, at about US$95.5m.

How Strong Is Hologic's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Hologic had liabilities of US$1.00b due within 12 months and liabilities of US$2.94b due beyond that. On the other hand, it had cash of US$2.45b and US$628.5m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$863.1m.

Zooming in on the latest balance sheet data, we can see that Hologic had liabilities of US$1.00b due within 12 months and liabilities of US$2.94b due beyond that. On the other hand, it had cash of US$2.45b and US$628.5m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$863.1m.

Since publicly traded Hologic shares are worth a very impressive total of US$18.5b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Carrying virtually no net debt, Hologic has a very light debt load indeed.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Hologic has very little debt (net of cash), and boasts a debt to EBITDA ratio of 0.077 and EBIT of 448 times the interest expense. Indeed relative to its earnings its debt load seems light as a feather. While Hologic doesn't seem to have gained much on the EBIT line, at least earnings remain stable for now. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Hologic's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Hologic actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

The good news is that Hologic's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that's just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. We would also note that Medical Equipment industry companies like Hologic commonly do use debt without problems. Overall, we don't think Hologic is taking any bad risks, as its debt load seems modest. So the balance sheet looks pretty healthy, to us. Another factor that would give us confidence in Hologic would be if insiders have been buying shares: if you're conscious of that signal too, you can find out instantly by clicking this link.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.