Idol's Dusk.

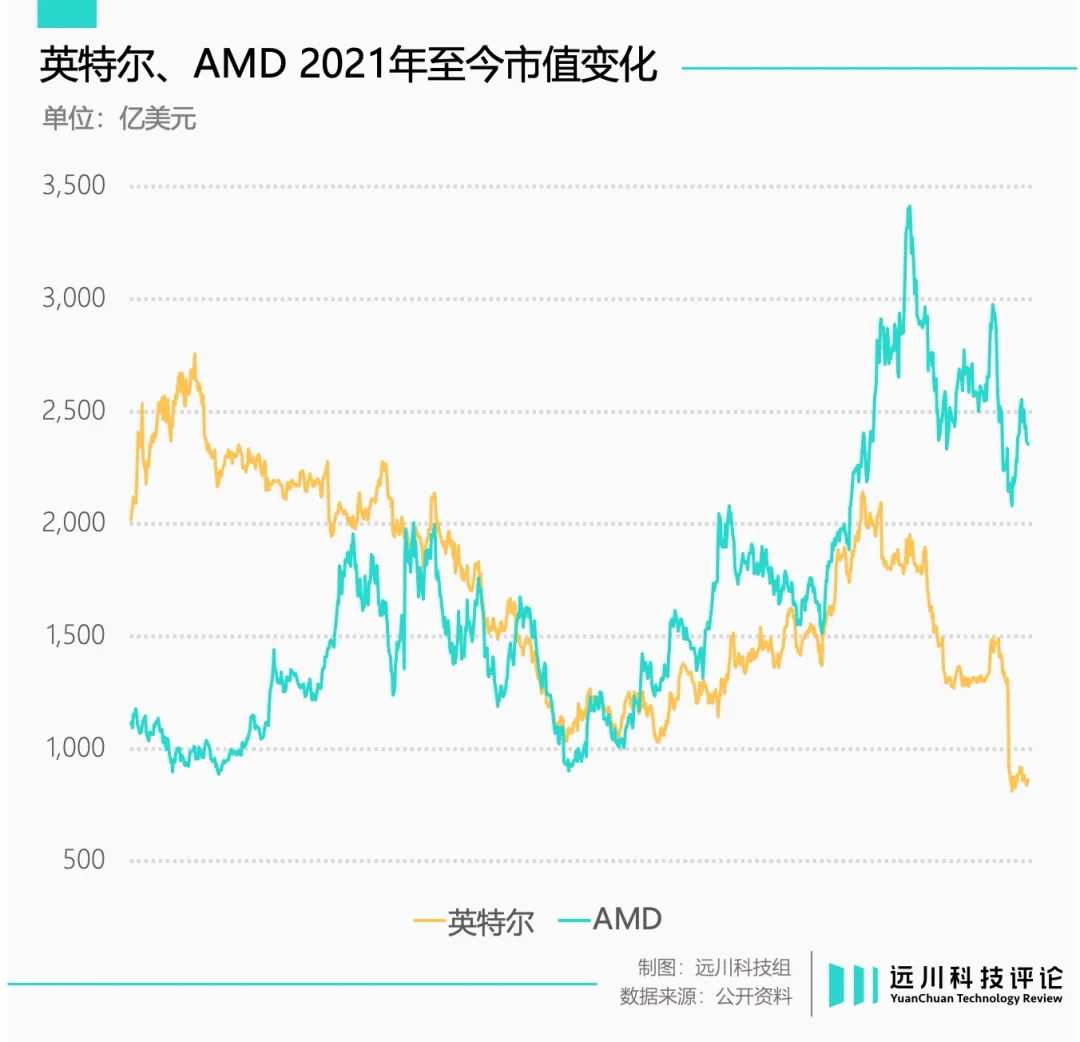

After delivering a disastrous second quarter report, $Intel (INTC.US)$ the next day's opening plunged by 26%, with the market cap shrinking to below $100 billion, barely reaching $Advanced Micro Devices (AMD.US)$ of a third, less than $NVIDIA (NVDA.US)$ 3%.

CEO Pat Gelsinger immediately began the three-pronged approach to open-source savings: first, transferring 15,000 employees to society; then selling off assets to raise funds, with the shelved programmable chip department, Altera, and the autonomous driving chip company, Mobileye; finally, Intel planned to spin off the chip manufacturing department to permanently get rid of this burden.

$Qualcomm (QCOM.US)$Five years ago, the rumors of acquiring Intel would have been considered onion news, but when public opinion began to seriously analyze the feasibility of the acquisition, the severity of the problem became apparent.

$Qualcomm (QCOM.US)$Five years ago, the rumors of acquiring Intel would have been considered onion news, but when public opinion began to seriously analyze the feasibility of the acquisition, the severity of the problem became apparent.

In 2020, Gelsinger returned to Intel with a technical background, and the market expects him to correct the situation as CEO and lead Intel back to a growth trajectory. However, the bold reform plan reached the mid-term evaluation stage, and the former semiconductor overlord could only be left to reflect in the triumphant song of the Magnificent 7.

A building does not collapse overnight, and the twilight of the blue giant did not come without warning.

The failure of the swinging pendulum.

The backwardness of the chip manufacturing process has been a core factor in Intel's rapid decline over the past few years.

Intel is one of the few companies in the semiconductor industry that still adheres to the IDM mode. IDM, in simple terms, can be understood as a one-stop shop for chip design, manufacturing, and testing. The advantage is strong production capacity, able to comprehensively implement its own strategies, the disadvantage is a long business line and high investment costs.

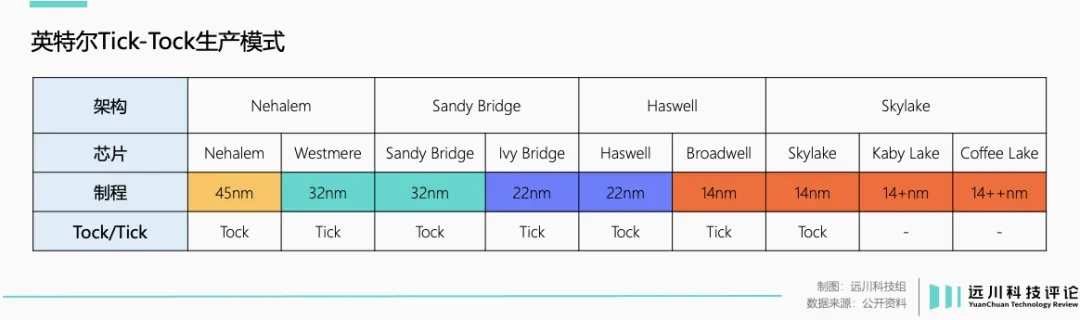

Based on IDM architecture, Intel has developed a production model called the tick-tock production cycle: with a two-year cycle, focusing on chip manufacturing during the 'tick year' and updating chip processes, and focusing on chip design during the 'tock year' and updating the architecture.

For example, the Sandy Bridge in 2011 and Ivy Bridge in 2012 adopted the same architecture, but the process was upgraded from 32nm to 22nm (tick). Haswell in 2013 continued to use the 22nm process but updated the architecture (tock).

Intel relied on this strategy to dominate the world, gaining a near-monopoly market position. However, in 2014, the 'tick-tock' pendulum began to fail.

Although the 14nm process was successfully mass-produced in 2014, there was already a gap of two and a half years since the previous 22nm generation. The 10nm process took a full 4 years to mass produce.

In these years of squeezing toothpaste, Intel coincidentally faced the rapid advancement to 5nm by Samsung and Taiwan Semiconductor allowed AMD to strike back decisively, surpassing Intel historically in market cap in 2022.$Taiwan Semiconductor (TSM.US)$In 2021, when Pat Gelsinger took office, Intel's stock price surged by 7% on the same day. However, he actually inherited a mess: AMD had eroded its core business, chip manufacturing lagged far behind Taiwan Semiconductor, and Intel was completely unprepared for the upcoming AI market explosion.

Intel’s former global dominance in the semiconductor industry is being challenged on multiple fronts.

Henry Kissinger's solution is an ambitious IDM2.0 plan - breaking the traditional model of 'in-house chip production', where the design department can have foundries like Taiwan Semiconductor manufacture chips, while the manufacturing department can take on foundry orders from other chip companies.

However, Intel's uniqueness lies in the fact that its manufacturing business serves only its own chips. The chip processes have been continuously upgraded, leading to the old processes being idle and phased out.

For example, when Samsung advances its in-house chips to 7nm, the outdated 14nm production lines are used for external orders. Intel, on the other hand, did not have a foundry business previously, resulting in an immature production capacity in terms of chip manufacturing. By 2021, Intel's production capacity at 28nm and above had been mostly phased out.

As a result, Intel proposed the acquisition of the ninth-ranked Israeli chip foundry, Taiwan Semiconductor (TSEM.US), which not only has a mature production line but also excels in areas such as automotive chips and industrial chips, complementing Intel perfectly.$Tower Semiconductor (TSEM.US)$, not only possesses complete and mature production lines, but also has a strong presence in areas such as automotive chips and industrial chips, making it a perfect complement to Intel.

However, geopolitical factors have caused governments around the world to tighten regulations on multinational companies, leading to unforeseen circumstances.MergerAlthough holding a considerable amount of orders, the acquisition case ultimately fell through, unable to contribute to the company's revenue.

In 2023, intel's foundry division contributed a $7 billion loss, with a further loss of $5.3 billion in the first half of this year. The aggressive 'four-year five-node' plan is still at the PowerPoint presentation stage, with substantial investments in wafer fab in the 'three connections and one basic' stage.

It is hard for a company to make mistakes in the downturn but easy to make blunders in its heyday. Intel's various hidden problems were buried in their peak days.

Audience at the center of the stage.

The 2010s were a brilliant yet lost decade for Intel. They struggled to find competitors in various product lines, costing them the missed opportunities of almost everything.

Refusing to supply mobile chips to Apple was an epic stain on Intel's record. However, reviewing the technological revolutions in the semiconductor industry after 2010, from smart phones, automated driving to artificial intelligence, Intel has remained that awkward audience in the center of the stage.

In the ai race, Intel had at least four chances to enter the field, all of which ended without results.

In 2009, Intel launched a project called Larrabee, aiming to introduce a truly universal GPU based on the x86 architecture.

At that time, Nvidia's GPU had attracted attention from the academic community due to its powerful parallel computing capabilities. Pat Gelsinger, the current CEO of Intel, was in charge of the Larrabee project. However, Gelsinger jumped to EMC in the same year the project started, leading to the project being abandoned midway.

Xeon Phi was the successor to Larrabee, still positioned as a general-purpose GPU. However, Intel's approach shifted from designing a completely new GPU to 'endowing CPUs with computation capabilities comparable to GPUs'. Due to high costs, Xeon Phi had almost no customers in an extremely limited product lifecycle. Coupled with the 10nm production difficulties, it was eventually discontinued in 2017.

Prior to discontinuing Xeon Phi, Intel completed two major acquisitions in succession. One was acquiring the 'second in FPGA' Altera and the other was purchasing the AI chip company Nervana. The former represented the potential hot track of AI inference chips, while the latter followed a similar technology route to Google's TPU – TPU was the driving force behind AlphaGo.

Unfortunately, before being divested or terminated, Altera only contributed an average of $0.5 billion in revenue per quarter, and Nervana delivered only one product, Nervana-NPP.

In the two emerging technologies of mobile chips and autonomous driving, Intel repeated a similar story:

The Atom series, targeting the mobile terminal market, was launched in the second year of the iPhone's debut. Instead of seizing the opportunity for rapid iteration, Atom faced five years of stagnation. Due to concerns about Atom's focus on cost-effectiveness squeezing the production capacity of other products, Intel's internal resource investment priorities were repeatedly pushed back.

Mobileye当年贵为自动驾驶芯片之王,但被英特尔收购后反而裹足不前,芯片性能掉出第一梯队,只能靠L1/L2低级别自动驾驶,勉强维持体面。

and $IBM Corp (IBM.US)$N/A.$Cisco (CSCO.US)$的故事不同,英特尔对新兴领域的嗅觉非常敏锐,对新技术的投资也没有丝毫懈怠。巅峰时期,仅英特尔一家的研发开支就占据了半导体产业的30%。

打开英特尔的“技术工具箱”,里面还摆放着从 $INFINEON TECHNOLOG (IFNNY.US)$ The baseband business acquired and later sold to apple, the high-speed storage product that has been losing money, Optane (shutdown in 2022), and even the drone business (sold to musk in 2022).

However, throughout the 2010s, this style of "working hard but only a little" in research and investment persisted, ultimately causing Intel to miss almost all emerging technologies after the PC era.

Corresponding to these missed opportunities is the frequent turnover of the company's CEOs - when an avalanche occurs, no snowflake is innocent.

Let the CEO work for a few more years.

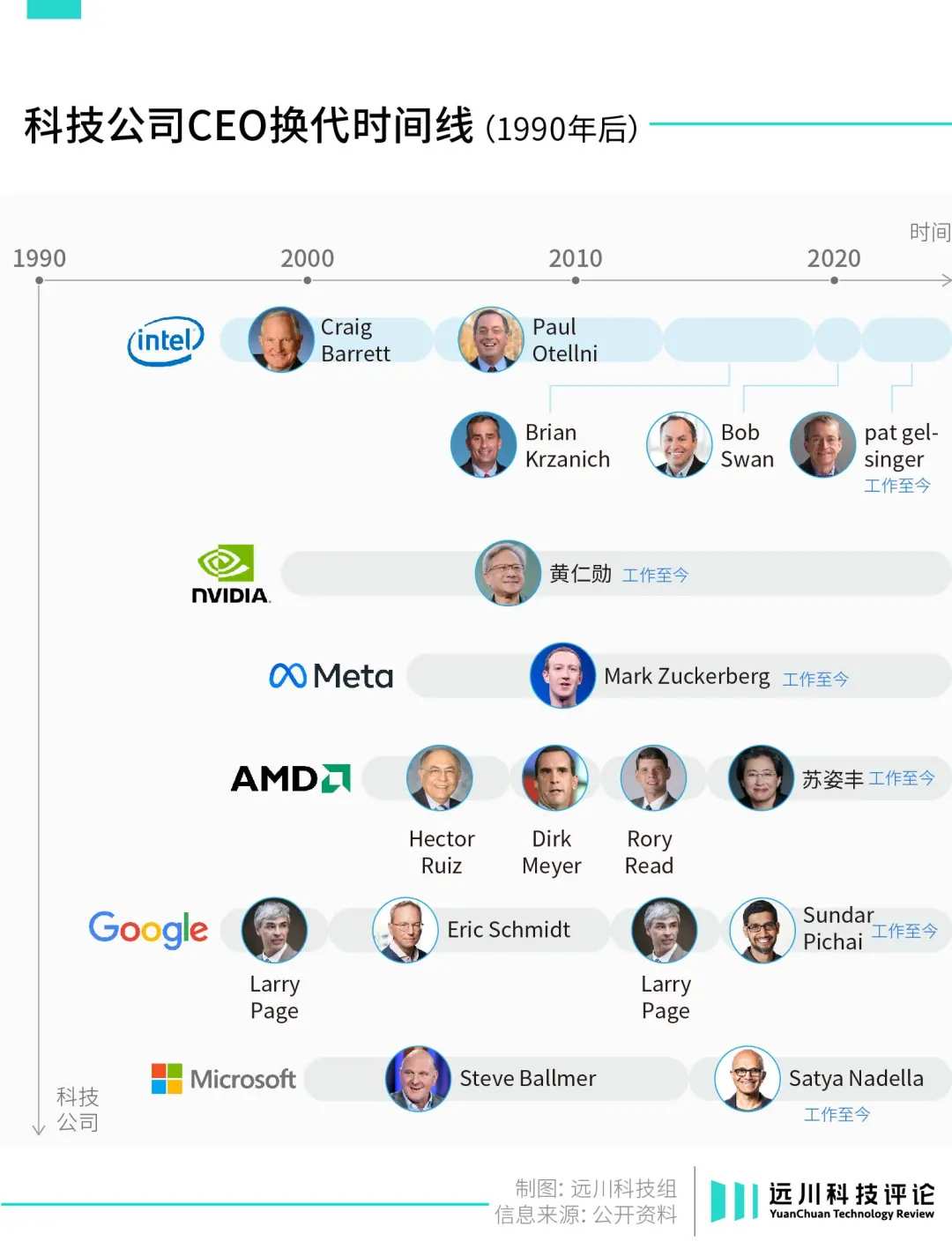

From 2000 to the present, Intel has changed CEOs five times in total, a frequency that may be normal for a football team but is a major taboo in the high-tech industry.

On the matter of missing technological waves, every Intel CEO can be criticized. First is Paul Otellini:

During Otellini's tenure, Intel successfully brought Apple into the x86 camp, but missed the best opportunity to enter the mobile terminal market by refusing to design chips for Apple.

回过味的欧德宁亡羊补牢,先是推出Atom系列处理器,借上网本杀进移动市场。虽然表现平淡,但这颗芯片的生命力不可谓不旺盛,一些$Tesla (TSLA.US)$老款车型的车机芯片就搭载了Atom处理器。

随后,欧德宁开始大力投资EUV光刻机,向ASML的EUV项目投资4.1 billion美元,比台积电(1.4 billion美元)和三星(0.974 billion美元)加起来还多[6]。

但这两项投资都伴随欧德宁在2013年的引咎辞职束之高阁。继任者科再奇不相信EUV光刻机的规模效应,坚持在10nm工艺节点采用技术更成熟、也更便宜的DUV光刻机,导致10nm良率迟迟上不去,被三星、台积电弯道超车。

早在2017年,英特尔就将第一台EUV光刻机收入囊中,但一直落灰到2021年才重见天日。其间,英特尔在14nm节点凑合了整整7代产品,牙膏厂的名号愈发响亮。

频繁的人事变动造成了各项业务战略的摇摆不定,继而影响了英特尔对新兴技术的长期投资。

Pat Gelsinger led the acquisition of Nervana during his tenure, marking Intel's fourth attempt in the field of artificial intelligence. However, in 2019, Pat Gelsinger resigned due to a scandal involving his lower body and Nervana predictably met its demise.

Robert Swan, with a financial background, took over and instead acquired the AI chip company Habana Labs, redirecting all resources that were originally intended for Nervana.

Leaders of high-tech companies need keen instincts, long-term vision, strong execution capabilities, but what truly carries everything is sufficient time in office. Only then can long-term technological investments remain stable and receive continuous resource support.

Intel's biggest competitor, AMD, also went through turbulence. In 2014, Lisa Su took over a mess and remained the CEO for a decade. Only after 2020 did her series of strategic plans gradually transform into actual market share and company performance.

Horizontal Comparison$Microsoft (MSFT.US)$and$Alphabet-C (GOOG.US)$ Like other technology companies, intel's leadership turnover is also too frequent. In contrast, Huang Renxun, who just celebrated his 60th birthday, shows no intention of retiring at all, stating that he wants to follow Zhang Zhongmou's example and work another 30 years. Mark Zuckerberg just turned 40 this year, right in his prime.

Another issue for intel is that after struggling in the x86 market, its next global strategy direction has remained unclear.

For high-tech companies, the successor's role is the 'executor of the next strategy'. Therefore, most companies will choose the person who will steer the future strategic business, rather than the one in charge of traditional past business.

Google's current CEO Sundar Pichai, before taking over, managed the Chrome and Android business, hardly touching the search business. Bezos's chosen successor is Andy Jassy, who pioneered the AWS cloud computing business and has hardly been involved in e-commerce. Similarly, Satya Nadella, before taking office, had never touched Windows and Office, but made a name for himself through cloud computing.

Intel keenly captured almost all revolutionary emerging technologies; unfortunately, compared to the all-in bet in 'Only the Paranoid Survive,' they only invested a little in each track.

Reference material

Intel used to dominate the U.S. chip industry. Now it's struggling to stay relevant, CNBC.

Intel’s Lunar Lake is actually made at taiwan semiconductor, PC World.

[3] Project Larrabee: How Intel's First Attempt at GPUs Failed,How-to Geek

[4] Observing the Fall of Intel's Nervana in the Semiconductor Industry

[5] Unwilling to Wait for 450mm and EUV Technology, Intel Invests $4.1 Billion in ASML, EET-China

[6] Patricio Kissinger: A Native Technology Enthusiast of Intel, TechSugar

[7] Only Paranoiacs Can Survive, Andy Grove

Editor/Somer