Concentrix Corporation (NASDAQ:CNXC) shares have had a horrible month, losing 29% after a relatively good period beforehand. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 35% share price drop.

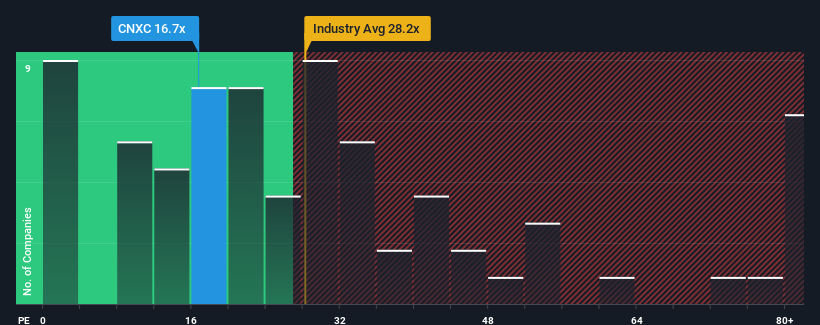

Although its price has dipped substantially, it's still not a stretch to say that Concentrix's price-to-earnings (or "P/E") ratio of 16.7x right now seems quite "middle-of-the-road" compared to the market in the United States, where the median P/E ratio is around 18x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Recent times haven't been advantageous for Concentrix as its earnings have been falling quicker than most other companies. It might be that many expect the dismal earnings performance to revert back to market averages soon, which has kept the P/E from falling. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. Or at the very least, you'd be hoping it doesn't keep underperforming if your plan is to pick up some stock while it's not in favour.

How Is Concentrix's Growth Trending?

There's an inherent assumption that a company should be matching the market for P/E ratios like Concentrix's to be considered reasonable.

There's an inherent assumption that a company should be matching the market for P/E ratios like Concentrix's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 54%. The last three years don't look nice either as the company has shrunk EPS by 54% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next year should generate growth of 52% as estimated by the five analysts watching the company. That's shaping up to be materially higher than the 15% growth forecast for the broader market.

With this information, we find it interesting that Concentrix is trading at a fairly similar P/E to the market. It may be that most investors aren't convinced the company can achieve future growth expectations.

What We Can Learn From Concentrix's P/E?

With its share price falling into a hole, the P/E for Concentrix looks quite average now. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Concentrix's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 4 warning signs with Concentrix (at least 1 which is a bit concerning), and understanding them should be part of your investment process.

If you're unsure about the strength of Concentrix's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.