相较于过往政策而言,本轮的强心剂显然强而有力。那么从政策层面上来看,本轮政策组合拳究竟发挥了怎样的作用,后市又该如何分析,本文将对此进行浅析。

相较于过往政策而言,本轮的强心剂显然强而有力。那么从政策层面上来看,本轮政策组合拳究竟发挥了怎样的作用,后市又该如何分析,本文将对此进行浅析。After the Federal Reserve entered a rate-cutting cycle, the market had expectations for the opening of China's interest rate space and policy space. However, many participants may not have anticipated that the government's sudden policy combination would have such a significant boosting effect on the stock markets in Hong Kong and mainland China.

On September 24, the State Council held a press conference and introduced a series of financial support policies to promote high-quality economic development, including the reduction of existing home loan interest rates, a comprehensive 50 basis points reserve ratio cut, two innovative capital market support tools, a total of 800 billion yuan in market liquidity supplementation, and expectations for the planning of the sovereign wealth fund. At the same time, news about the entry of medium to long-term funds into the market and the management of central enterprise market capitalization has been mentioned again, showing that this round of comprehensive policies is very sincere in terms of intensity and scale.

From the perspective of market sentiment, this round of policy combination has powerfully boosted market confidence. On September 24, both Hong Kong and mainland China stock markets set new highs for the year, with visible increases in trading volume. As of the publication date, the Hang Seng Index and the Shanghai Composite Index maintained an upward trend.

Compared to past policies, this round of powerful stimulus is evidently robust. So, from a policy perspective, what role has this round of policy combination played, and how should we analyze the future market trends? This article will provide a brief analysis.

Compared to past policies, this round of powerful stimulus is evidently robust. So, from a policy perspective, what role has this round of policy combination played, and how should we analyze the future market trends? This article will provide a brief analysis.

What role can be played by traditional interest rate tools being implemented?

To speak frankly about the core nature of this policy combination, the term "flooding" is perhaps the most common description in the industry, in other words, it provides incremental liquidity to the market. However, in implementing this effect, the policy side is not purely traditional, but combines some innovative tools to achieve the flooding effect, with varying closeness in terms of timing.

Starting with more traditional policies, namely, reserve ratio cuts, reduction of existing home loan interest rates, and lowering the down payment ratio for second homes, these are policy tools that have been used repeatedly in past policies, and the market, including the author, has mostly predicted them.

Specifically, the central bank announced a recent 50 basis points reduction in the reserve requirement ratio. The reserve requirement ratio for major banks will decrease from 8.5% to 8.0%, for medium-sized banks from 6.5% to 6%, and rural financial institutions will remain at 5%. At the same time, the central bank will guide commercial banks to lower existing home loan rates to be near the rates for new home loans, with an average expected decrease of 50 basis points, and will lower the minimum down payment rate for second homes nationwide from 25% to 15%, unifying the minimum down payment rates for first and second home mortgages at the national level.

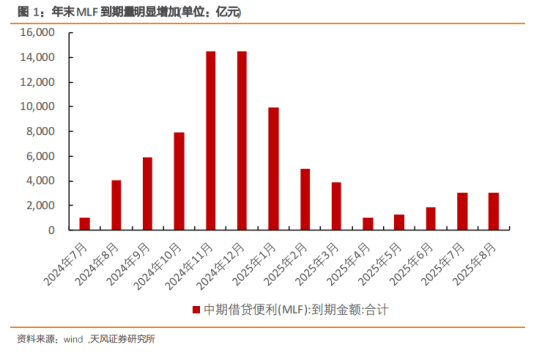

Regarding the central bank's reserve ratio cut measures, it is actually somewhat beyond expectations, but still rational. Due to the relatively poor economic data performance, since mid-August, the government's debt issuance speed has increased. Combined with the previous policy direction of "emptying the space" and "stopping manual replenishment", it has brought certain pressure to the long-term funds in the interbank market. Looking at the scale of MLF maturities by the end of the year, the pressure on maturities after October is evident. The liquidity supplement brought by the reserve requirement cut provides the market with approximately 1 trillion yuan of long-term liquidity, which also significantly supplements the liquidity that banks can provide.

As for the reduction of existing housing loan interest rates and the reduction of the down payment ratio for the second home, the author has already analyzed and mentioned these policies recently, so I won't go into too much detail here. Let's discuss the effectiveness of the implementation of the 50 basis points reduction. According to the central bank's calculations, the reduction of existing housing loan interest rates can reduce the total annual interest expenditure of families by approximately 150 billion yuan. According to SHWY's calculations, based on the total scale of 49.3 trillion yuan of resident consumption in 2023, the reduction in mortgage rates is expected to stimulate consumption by around 0.2%. From the above calculations, this policy is more aimed at easing the urge for residents to repay loans early.

Looking back at the three total policy adjustments since 2024, the first quarter saw a reserve requirement cut and an asymmetric interest rate cut for the LPR. In July, the interest rate tool was focused on OMO rate as the core for the interest rate cut, while this time it is a combination of tools at the total and real estate levels for the interest rate cut. The overall tone has shifted from loose to looser and the policy strength is continuously increasing.

How will the unexpectedly new policies support the equity market?

Overall, looking at the central bank's policies related to real estate support and reserve ratio cuts, most can only be said to be in line with expectations. However, the highlight of the policy combination on September 24th is that the two innovative monetary policy tools significantly exceeded market expectations. This is also the first time that the People's Bank of China has supported the capital markets with innovative structural monetary policy tools, hence the significant market response.

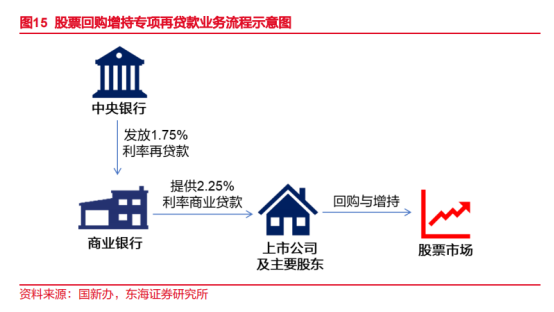

Among them, the special redisclosure of share buyback and incremental loans is a relatively easy-to-understand monetary tool. Encouraging banks to provide loans to listed companies and major shareholders, supporting share buybacks and holding increases, can be considered as a type of incremental structural policy tool. Considering the previous market correction, many companies' stock prices are currently undervalued, and listed companies themselves have a strong willingness to repurchase shares.

The introduction of special rediscount loans has helped listed companies solve their funding problems, or may boost the repurchase willingness of some enterprises. From a cost perspective, the rediscount loan rate is 1.75%, the loan rate issued by banks is 2.25%, the initial quota is 300 billion yuan, and there may be further quota releases depending on the situation.

From past policies, during the pandemic, special rediscount loans were used to strengthen financial support for key enterprises in important medical and daily necessities sectors, being one of the main channels through which the central bank creates liquidity for specific sectors. This time being used for the commonly used countercyclical adjustment method of repurchases in the capital markets, it will drive the expansion of the basic currency, improve the supply-demand balance of the stock market. For companies with repurchase willingness, the repurchase costs previously borne out of their own pockets can now be used for listed company dividends or physical business investments. In conjunction with the incremental policy measures proposed by the regulators, it is undoubtedly a strong support for listed companies.

Relatively speaking, the interchange convenience of securities, funds, and insurance companies is a relatively new concept domestically. According to the central bank, the interchange convenience is achieved by "swapping securities and assets of securities, funds, and insurance companies through collateralization for high liquidity national debt and central bank notes assets, and these assets may subsequently be converted into liquidity inflows into the stock market through other means.

Compared to the previous special loans, the interchange convenience does not increase the basic currency, and does not directly provide funds to non-bank institutions. According to the Governor of the central bank, the initial scale of interchange convenience operations is 500 billion yuan, which can be "expanded as needed in the future."

In terms of specific implementation conditions and details, both of the above currency support tools have many parts that need to be supplemented. For example, whether the liquidity obtained from rediscount loans/interchange convenience is applicable to companies listed in the Hong Kong stock market. For A+H type enterprises, how should their share buybacks be calculated? In facing the higher-risk equity market, how should the central bank grasp the risk factors of rediscount loans? These details may have a significant impact on the effectiveness of this policy and require continuous attention in the future.

But undoubtedly, the two new monetary policy tools will bring 800 billion yuan, or even more, liquidity increment to the equity market. For the declining turnover of A-shares and Hong Kong stocks, it will undoubtedly be a powerful heartening agent.

Compared to overseas markets, the central bank's direct liquidity injection measures are not uncommon. Measures such as the quantitative easing in the United States, or the ETFs used by the Bank of Japan to purchase stocks, are common means to stabilize/boost the stock market and enhance investor confidence. The stability of the capital markets is crucial for high-quality economic development, and this unexpected policy implementation is a strong move made by the central bank to promote the vigorous development of the capital market and help enhance the quality and efficiency of the real economy.

It is worth mentioning that besides the new policy tools mentioned above, the governor of the central bank also disclosed the intention to establish a reserve fund. Reserve funds have precedents in stock markets in Hong Kong, Japan, South Korea, the USA, etc., and are a type capable of effectively alleviating the spread of market pessimism, injecting liquidity into the market, and helping the market stabilize and rebound as a 'national team'. In the past A-share market, this responsibility was played by sovereign wealth funds/state-owned investment companies, and with the formal establishment of the reserve fund, the official debut of the national team may be not far away. In terms of further policy follow-up efforts, the establishment brings hopeful expectations.

After the opening of policy space, which assets should be paid attention to?

In terms of timing, the landing time of this policy package was on the eve of National Day, which can be considered to be related to the habit of 'sending gifts before holidays', but more likely due to the move by the Federal Reserve to open up space in the domestic interest rate market.

On September 18, the Federal Reserve announced a 50 basis point reduction in the target range for the benchmark interest rate, opening the much-awaited rate cut cycle since 2022, and the initial rate cut exceeded market expectations to some extent. According to Powell's emphasis at the monetary policy meeting, there are currently no significant signs of recession in the USA, and this rate cut leans more towards a defensive cut, aiming to improve liquidity, support economic growth, and prevent further deterioration in employment situations.

Regarding the impact of the Federal Reserve's rate cut, there have been many analyses in the market. Here, the author will not dwell too much but mainly focus on two points. One is the impact of the rate cut on the Chinese market. As analyzed earlier, due to various market factors, even though the Federal Reserve has started the rate-cutting cycle, the support from overseas capital inflows to the domestic market is not as encouraging as expected. However, with the rate cut in place, the exchange rate of the US dollar against the RMB has been significantly affected. With the combined efforts of the Chinese and US monetary policy cycles, the offshore RMB broke through the key level of 7 yuan on September 25, and its impact may be worth investors' attention.

Against the backdrop of the decline in the exchange rate of the US dollar against the RMB, foreign trade enterprises may avoid significant disturbances in foreign exchange gains and losses and may start repatriating overseas export revenue from the past few years through US dollar deposits and US dollar-denominated assets to attract domestic assets. However, for the Chinese market in the midst of a wave of enterprises going global, the appreciation of foreign exchange is not beneficial for exporting and going global. In the context of a continuously strengthening RMB, export-oriented enterprises relying mainly on overseas income may need to pay attention to certain risks.

On the other hand, the strengthening of the RMB may have favorable effects on the stock market, especially the Hong Kong stock market compared to the A-share market. Chinese companies listed in Hong Kong benefit from RMB calculations and valuations in Hong Kong stocks. With the appreciation of RMB, the improvement in profit levels will become their advantage. For the southbound funds of the Hong Kong Stock Connect, the benefits of Hong Kong stock quotes and RMB settlement will gradually be reflected as the currency appreciates. Additionally, due to the linked exchange rate system in Hong Kong, the strengthening of the RMB also has a loosening effect on Hong Kong's financial conditions, which may bring unexpected positive effects for enterprises focusing on local assets in the Hong Kong stock market.

Secondly, it is the frequent exceeding of the gold spot price trend beyond the author's expectations. As of the time of writing, the international gold spot price once reached around $2680 per ounce, with a sharp focus on the $2700 mark. It can be said that for the author who had previously warned several times about the limited upside potential of gold and the high-level pressure, this is a very embarrassing matter.

Whether it is the unexpected interest rate cuts or the increasingly intense geopolitical conflicts in the Middle East, the current trend in the gold market still shows no signs of decline. However, with prices at high levels and significant short-term gains, the risks, in the author's view, still remain significant. It can only be said that approaching the holiday season, one should pay attention to profit-taking and short-term reversal signals, as well as distinguish between the differences of gold spot and gold stocks. The relationship between returns and risks during this period can only be balanced by investors participating in the market themselves.

In conclusion,

In the author's opinion, the policies implemented this time, as different from the past 'emotion-driven' policies, are more practical and have actual liquidity-stimulating measures. Therefore, personally, the author is quite bullish on the trend of the equity market in the fourth quarter.

As of the date of writing, the Hang Seng Index and the Shanghai Composite Index still maintain an upward trend, but whether this trend can continue after the holiday period remains unknown. After the frenzy of receiving the policy 'gifts', the market, when it calms down, will still ponder and worry about the future situation of the market. The effects of implemented policies need time and data for validation, while a comprehensive rebound in the equity market still requires an improvement in the domestic economic fundamentals to drive it forward.