Micron Technology's revenue is expected to reach a record high this quarter, with revenue guidance increasing by up to 88%. The high end of EPS guidance is nearly 20% higher than analysts' expectations, and the company expects revenue for the fiscal year to set a 'substantial record'. Micron forecasts that by 2025, the HBM market size will increase from $4 billion in 2023 to over $25 billion, and the company will ramp up production of HBM3E 12H products early in 2025.

Leader in the U.S. storage chip industry $Micron Technology (MU.US)$ Accelerated growth in the past fiscal quarter, coupled with strong performance in the current quarter exceeding Wall Street expectations, reflects the robust demand for high-bandwidth memory (HBM) amidst the artificial intelligence (AI) boom.

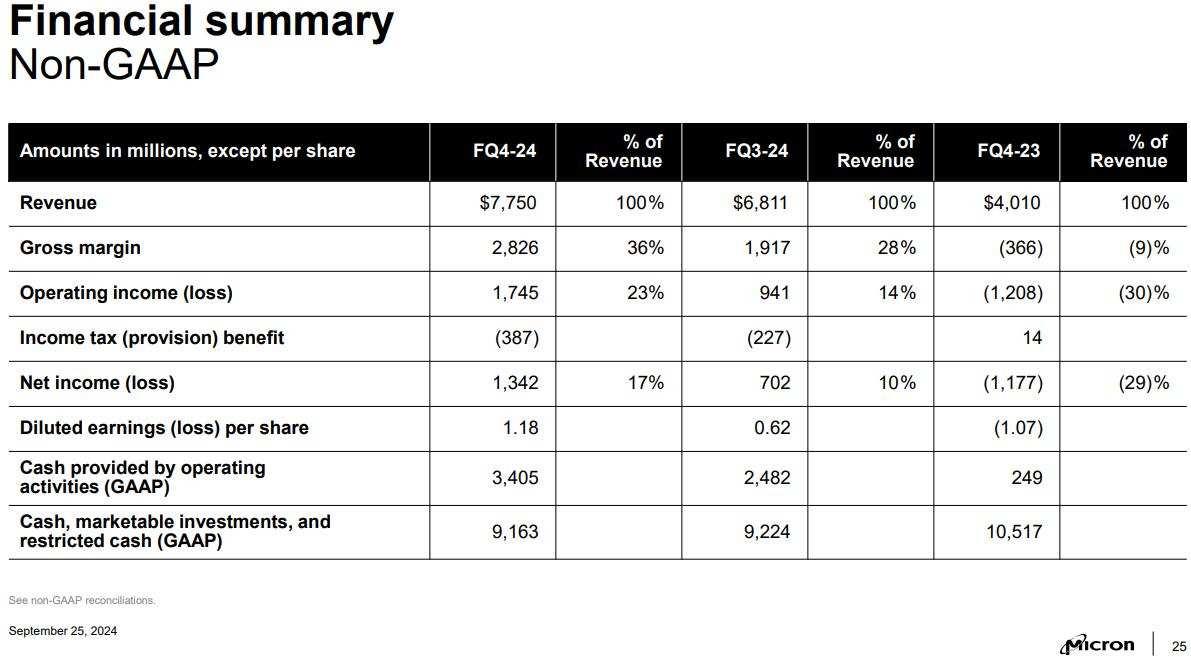

After the post-market trading on Wednesday, September 25th, Micron Technology released financial data for the fourth quarter of the 2024 fiscal year (referred to as Q4) ending on August 29, 2024, and provided performance guidance for the first quarter of the 2025 fiscal year (referred to as Q1).

1) Key Financial Figures:

1) Key Financial Figures:

Revenue: Q4 revenue was $7.75 billion, a 93.3% year-on-year increase, surpassing analysts' expectations of $7.66 billion. The company's guidance was $7.4 billion to $7.8 billion, with an 81.6% year-on-year increase from the previous quarter.

EPS: Non-GAAP diluted EPS for Q4 was $1.18, compared to a loss of $1.07 per share in the same period a year ago and analysts' expectations of $1.12. The company's guidance was $1.00 to $1.16, with a profit turnaround from the previous quarter's loss to $0.62 per share.

Operating profit: After adjustment in the fourth quarter, the operating profit was $1.745 billion, compared to a loss of $1.208 billion in the same period a year ago. Analysts expected $1.58 billion, turning from a loss to a profit year-on-year to $0.941 billion in the previous fiscal quarter.

Gross margin: After adjustment in the fourth quarter, the gross margin was 36.5%, compared to -9.1% in the same period a year ago. Analysts expected 34.7%, with the company guiding from 33.5% to 35.5%, compared to 28.1% in the previous fiscal quarter.

Expected Q3 revenue growth of 3.25%-4.25% and adjusted earnings per share of 0.51-0.52 US dollars, below the market estimate of 0.55 US dollars.

Revenue: The first-quarter revenue is expected to be $8.7 billion, with a range of ±$0.2 billion, equivalent to a guidance range of $8.5 billion to $8.9 billion. Analysts expected $8.32 billion.

EPS: The diluted EPS for the first quarter after adjustment is $1.74, with a range of ±$0.08, equivalent to a guidance range of $1.66 to $1.82. Analysts expected $1.52.

Gross margin: After adjustment in the fourth quarter, the gross margin was 39.5%, with a range of ±1 percentage point, equivalent to a guidance range of 38.5% to 40.5%. Analysts expected 37.6%.

Micron Technology's performance in the last quarter was significantly better than expected, but the guidance for this quarter fell short of Wall Street's 'ultra-high expectations', and the production capacity of HBM chips is limited, causing the company's stock price to continue to decline. Some commentators have said that the market has not been very optimistic about Micron recently. Citigroup even stated before Micron's financial report that many investors expected Micron's performance to fall short of the guidance. However, Micron's performance this time clearly injected a strong stimulant into stock market investors.

The revenue for this quarter is expected to reach a historic high. The revenue for the fiscal year is expected to set a "significant record".

Financial reports show that in the fourth quarter, both revenue and profit of Micron accelerated compared to the previous fiscal quarter, surpassing Wall Street's expectations. Analysts expect Micron's fourth-quarter revenue to increase by 91%, exceeding expectations by 93%.

Furthermore, Micron's performance guidance is very strong. Based on the guidance range, Micron expects a nearly 80% to about 88% increase in revenue for the first quarter, while analysts expect a nearly 76% increase. Micron's EPS guidance for the first quarter overall exceeds analysts' expectations, with the upper end of EPS guidance exceeding expectations by almost 20% and the lower end by 9.2%.

In the announcement of the financial report, Micron CEO Sanjay Mehrotra attributed the fourth-quarter revenue growth to AI demand and optimistically expects first-quarter revenue to reach a single-quarter historic high. He stated:

"Strong AI demand has driven growth in data center DRAM products and our industry-leading HBM. Data center SSD sales have led to record-breaking NAND revenue, exceeding $1 billion for the first time this quarter."

"We are entering the 2025 fiscal year in Micron's strongest competitive position ever. We expect the first quarter revenue to reach a historic high, and the revenue for the 2025 fiscal year to set a significant record, with a significant increase in profitability."

The HBM market size is expected to exceed $25 billion in 2025. Production of HBM3E 12H has been increased since the beginning of the year.

Before Micron released its financial report, analysts predicted strong growth in revenue for one of Micron's most profitable products, the HBM used for AI data processing. In the financial report, Micron stated that the data center business where HBM is located achieved record annual revenue in the 2024 fiscal year, with a significant increase expected for the 2025 fiscal year based on this performance.

Micron expects the overall market size of HBM (TAM) to increase from about $4 billion in calendar year 2023 to over $25 billion in 2025.

In February of this year, Micron started mass production of HBM3E designed specifically for AI and supercomputers. In this financial report, Micron mentioned the progress of this product, stating that compared to competitors' HBM3E 8H 24GB capacity solution, Micron's HBM3E 12H 36GB capacity product reduces power consumption by 20% and offers 50% higher DRAM capacity.

Micron expects to increase production of HBM3E 12H products early in calendar year 2025, with a full year increase in product shipments.

Micron mentioned that the demand for data center solid-state drives (SSDs) continues to experience strong growth driven by AI, as well as the recovery in the traditional PC and storage markets. The revenue from data center SSDs in the fourth quarter exceeded $1 billion, setting a new single-quarter record, with data center SSD revenue for FY 2024 more than doubling compared to a year ago.

Editor/Lambor