①How is the sustainability of the stock market following the real estate and infrastructure trends in the Hong Kong cement sector? ②What are the highlights of the successive price increases in the cement markets in multiple regions?

Financial Union News on September 25th (Editor: Feng Yi) Due to the positive macro policies and the return of the real estate and infrastructure trends, the stock prices of Hong Kong cement companies rose today.

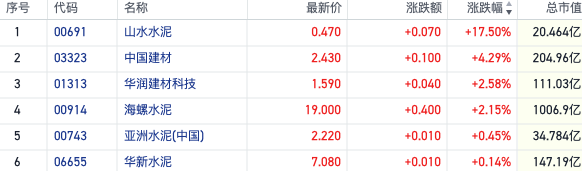

As of the time of publication, Shanshui Cement (00691.HK) rose by more than 17%, China National Building Materials (03323.HK) rose by over 4%, Huaxin Building Materials Technology (01313.HK), Conch Cement (00914.HK) both rose by over 2%, Huaxin Cement (06655.HK) followed the upward trend.

On the news front, after various local cement associations strengthened industry self-discipline in response to production control since August, cement prices have shown a rebound trend recently.

On the news front, after various local cement associations strengthened industry self-discipline in response to production control since August, cement prices have shown a rebound trend recently.

According to Century Building Information, in early September, cement prices in many areas of Zhejiang rose by 10-20 yuan/ton, and some brands in markets such as southern Jiangsu successively raised prices by 20-30 yuan/ton. Most brands maintained price increases ranging from 10-30 yuan/ton; in many areas of Sichuan, from the 6th onwards, the ex-factory prices of various types of bagged cement and bulk cement were raised by 40 yuan/ton over the original prices.

In addition, the mainstream brand manufacturers in the main urban area of Chongqing notified of a 50 yuan/ton increase in cement prices; additionally, cement manufacturers in the western region of Chongqing notified of a 30 yuan/ton increase in cement prices.

Analysts in the industry state that the current market demand has improved somewhat, coupled with significant losses in cement companies themselves, leading to a strong willingness to raise prices.

On the other hand, due to the press conference held by the State Council Information Office announcing multiple macroeconomic bullish policies, including reserve requirement ratio cuts, interest rate cuts, adjustment of existing housing loan interest rates, and reduction of down payment ratios for second homes, the market's expectations for the real estate and infrastructure sectors have risen. Cement, as an upstream industry for these two major sectors, has also been boosted.

CITIC Securities pointed out that policy bullishness is expected to transmit throughout the entire industry chain. The cement industry is already at the bottom of a profit cycle, and if subsequent real estate sales can stabilize with policy support, the drag on cement demand from the real estate sector will not worsen. In addition, in recent years, the cement supply structure has gradually improved, and the profit restoration expectations for leading enterprises are gradually improving.

It should be noted that despite the short-term stabilization and rise in cement prices, they are still in a downward cycle.

According to the latest data from the National Bureau of Statistics, as of mid-September, the domestic bulk cement price of P.O42.5 was 322.5 yuan/ton, still far below the national average price of 394 yuan/ton in 2023.

Analysts Sun Weifeng and Chen Qifan from Everbright Securities also mentioned in their report on September 23 that with the continuous weakening of demand, the difficulty in implementing staggered production increases and the weakening impact on price increases.

Analysts Wu Huidong and Zhu Simin from Guolian Securities also stated in a recent research report that China's cement demand has entered a plateau period with a certain marginal decline, and the key to resolving the overcapacity situation in the cement industry should focus on the supply side.

It is worth noting that on September 9, the Ministry of Ecology and Environment publicly solicited opinions on the "National Carbon Emission Trading Market Covering Cement, Steel, and Electrolytic Aluminum Industry Work Plan (Draft for Soliciting Opinions)." According to the draft for soliciting opinions, the cement industry will be officially included in the national carbon market within this year.

Guolian Securities believes that the current profitability of the cement industry may be at historically low levels, and the valuations of major cement companies are also at historically low levels. In recent years, policies have had some effect on constraining capacity and guiding an increase in existing capacity. It is recommended to pay attention to the changes and positive influences after continuous clearance of supply.