除此之外,研究出台盘活存量土地的增量政策、延长“金融16条”、经营性物业贷款的文件期限,进一步加大企业端资金支持力度,对于当前稳定企业预期、提振市场信心也将发挥重要作用。

除此之外,研究出台盘活存量土地的增量政策、延长“金融16条”、经营性物业贷款的文件期限,进一步加大企业端资金支持力度,对于当前稳定企业预期、提振市场信心也将发挥重要作用。Overall, this time the central bank released several heavy positive signals, which will have a positive impact on the macro economy and real estate market. With multiple measures being implemented simultaneously, it is expected to stabilize housing prices and accelerate the bottoming out of the real estate market.

China Real Estate Research Institute released a report stating that on September 24th, the State Council Information Office held a press conference. Overall, this time the central bank released multiple major positive news, which will have a positive impact on the macroeconomy and real estate market. By releasing liquidity through reserve requirement cuts and interest rate cuts to boost the economy, the expected economic improvement is likely to restore residents' income expectations. Lowering existing home mortgage rates will further stabilize buyers' home purchase expectations, improve market sentiment, and lowering the 7-day reverse repurchase rate will further guide the downward trend of the 5-year and above Loan Prime Rate (LPR) in October, continuing to reduce home purchase costs; lowering the minimum down payment ratio for the second home will significantly reduce the threshold for residents to buy homes, implementing a range of measures simultaneously, aiming to stabilize housing prices and accelerate the bottoming out of the real estate market.

Furthermore, the report mentioned that the central bank also expanded the proportion of central bank funds supporting reloans for affordable housing, which will help increase the scale of commercial bank loans. It will have a certain positive impact on local housing inventory accumulation. However, it is worth noting that the current progress of local housing inventory accumulation is slow, and key influencing factors such as great difficulty in matching inventory prices, high costs for local SOEs in inventory accumulation, and supply-demand mismatch exist. The current central bank interest rate cut can to a certain extent reduce the inventory accumulation costs of SOEs, while factors such as inventory prices, supply-demand mismatch may still require more short-term policy support to help local governments accelerate the inventory accumulation process.

In addition, measures to revitalize existing stock land, extend the '16 financial policies', and the document period for operational property loans, will further increase the support for funds to enterprises, playing an important role in stabilizing current business expectations, boosting market confidence.

In addition, measures to revitalize existing stock land, extend the '16 financial policies', and the document period for operational property loans, will further increase the support for funds to enterprises, playing an important role in stabilizing current business expectations, boosting market confidence.

On September 24, the State Council Information Office held a press conference to introduce the situation regarding financial support for high-quality economic development. People's Bank of China Governor Pan Gongsheng, China Banking and Insurance Regulatory Commission Chairman Li Yunze, and China Securities Regulatory Commission Chairman Wu Qing attended the event and answered questions. Among them, Governor Pan Gongsheng of the People's Bank of China announced multiple significant measures such as reserve requirement ratios cut, interest rate reduction, and adjustment of existing house mortgage rates. Meanwhile, Chairman Li Yunze of the China Banking and Insurance Regulatory Commission also presented progress on the 'white list' work.

Pan Gongsheng announced:

First, to lower the deposit reserve ratio and policy rates. Recently, the deposit reserve ratio will be lowered by 0.5 percentage points, providing approximately 1 trillion yuan of long-term liquidity to the financial market. Within this year, depending on the market liquidity conditions, there may be further reductions of 0.25-0.5 percentage points at the right time. Lower the central bank's policy rates, with the 7-day reverse repurchase operation rate reduced by 0.2 percentage points from the current 1.7% to 1.5%. At the same time, guide the decline in loan market quoted interest rates and deposit rates simultaneously, maintaining the stability of commercial banks' net interest margin.

二是降低存量房贷利率和统一房贷最低首付比例。引导商业银行将存量房贷利率降至新发放贷款利率的附近,预计平均降幅大约在0.5个百分点左右。统一首套房和二套房的房贷最低首付比例,将全国层面的二套房贷款最低首付比例由当前的25%下调到15%。将5月份人民银行创设的300 billion元保障性住房再贷款,中央银行资金的支持比例由原来的60%提高到100%,增强对银行和收购主体的市场化激励。将年底前到期的经营性物业贷款和“金融16条”这两项政策文件延期到2026年底。

李云泽表示:

在各方共同努力下,城市房地产融资协调机制取得了良好效果。截至目前,商业银行已审批白名单项目超过5700个,审批通过融资金额达到1.43 trillion元,支持400余万套住房如期交付。在协调机制的带动下,金融机构对房地产行业的支持力度也在不断扩大。截止到8月末,今年房地产开发贷款较年初实现了正增长,扭转了几年来持续下滑的态势,房地产的并购贷款和住房租赁贷款分别增长14%和18%,为促进房地产市场平稳健康发展提供了有力的金融支持。同时为积极支持刚性和改善性的住房需求,我们会同人民银行指导各地、各家金融机构因城施策来调整相关的房地产金融的政策。下一步,也会配合人民银行积极推进,稳妥降低存量房贷的利率,以进一步减少居民房贷支出,提高人民群众的获得感。

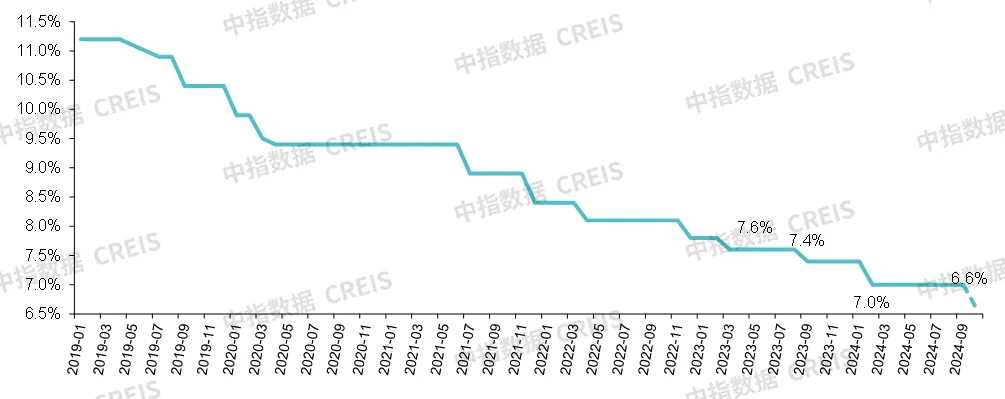

1.降准降息提振市场信心,促进经济平稳运行

2月央行下调存款准备金率0.5个百分点,向市场提供长期流动性约1 trillion元,金融机构加权平均存款准备金率为7%。此次存款准备金拟再次下调0.5个百分点,向金融市场提供长期流动性约1 trillion元,降准政策实施后,银行也平均存款准备金率约为6.6%,仍具备一定空间。

图:2019年以来金融机构平均存款准备金率

Pan Gongsheng also stated, "By the end of the year, we still have three more months, and depending on the situation, we may further reduce by 0.25-0.5 percentage points." This means that after this reserve requirement cut, there is still a certain expectation of further reserve cuts in the fourth quarter.

At the same time, the meeting also announced an interest rate cut. In July, the central bank reduced the 7-day reverse repo operation rate from 1.8% to 1.7%, another 20 BP cut to 1.5%. Under the market-oriented interest rate control mechanism, the adjustment of policy rates will drive the adjustment of various market benchmark rates. It is expected that in October, the LPR and deposit rates will also be lowered by 0.2-0.25 percentage points.

Under the combination of reserve requirement cut and interest rate cut policies, more liquidity will be released and financing costs lowered, which is expected to boost market confidence and facilitate the stable operation of the macroeconomy.

2. Guide the downward adjustment of new lending and existing home loan rates, reduce home buying costs, and restore market expectations.

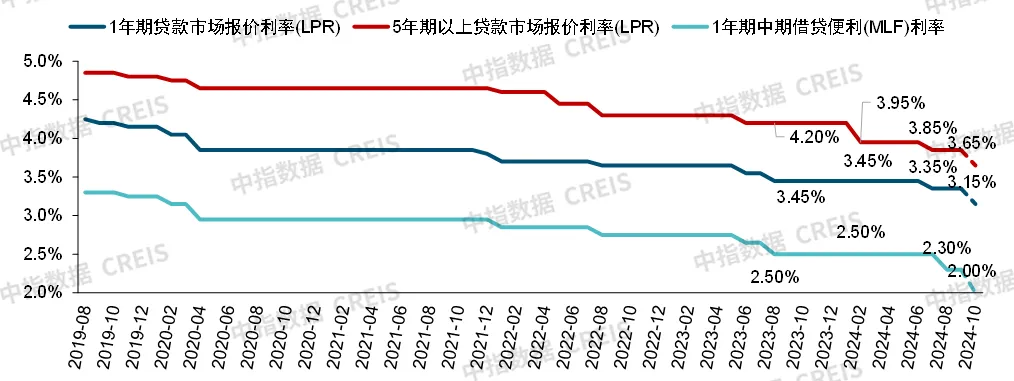

Chart: Trends in 1-year and 5-year LPRs

Since 2024, the central bank has twice lowered the 5-year LPR by a total of 35 BPs to 3.85%, while also removing the lower limit of first and second home loan rates at the national level. Currently, except for Beijing, Shanghai, and Shenzhen where the lower limits on home loan rates have not been removed, all other cities nationwide have removed the lower limits. First-home mortgage rates for new loans have dropped to around 3.2% in multiple cities, and in some cities rates have fallen below 3%.

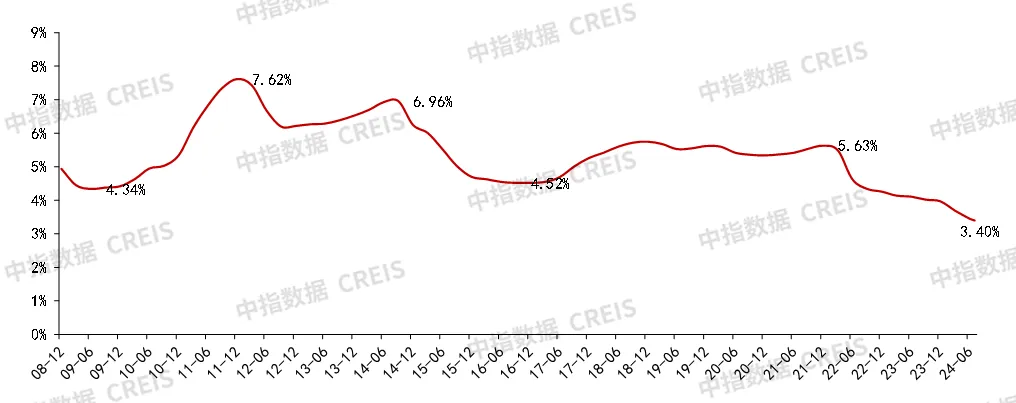

From the perspective of the impact of house prices, the average rental-to-purchase ratio in the current focus of 50 cities is 2.1%. In terms of capital costs, the yield of the 10-year national bonds is about 2%, and in July, the interest rate for new personal housing loans was 3.4%. The interest rate for first home loans with a term of over 5 years is 2.85%. Considering a comprehensive down payment ratio of around 30% (although the minimum down payment ratio has been reduced to 15%, the residents' willingness to leverage may not be strong), the current comprehensive capital cost for residents to purchase a house is approximately between 2.6% to 3%. Lowering interest rates helps reduce the cost of residents purchasing houses, bringing it closer to the rental-to-purchase ratio, thus stabilizing house prices.

Image: Average loan interest rate for personal housing loans from financial institutions

Previously restricted by narrow bank interest margins, the reduction of existing home loan rates was constrained. This reduction was opened up by the recent central bank reserve requirement cut. Pan Gongsheng stated that 'The central bank's reserve requirement cut provides banks with low-cost, long-term funds for operations directly. Medium-term lending facilities and open market operations are the central bank's main ways to provide commercial banks with medium and short-term funds. The decline in interest rates will also reduce banks' funding costs.'

In this press conference, Pan Gongsheng pointed out that 'The People's Bank of China plans to guide banks to make batch adjustments to the interest rates of existing home loans, lowering the existing home loan rates to near the new loan rates. We expect the average decrease to be around 0.5 percentage points. We use the term average because loans are issued at different times, in different regions, and by different banks, resulting in different levels of existing home loan rates being issued. We predict the decrease will be the expected average. Lowering the interest rates of existing home loans by banks will help further reduce borrowers' interest payments on home loans. We estimate that this policy will benefit 50 million households and 150 million individuals, reducing the total interest payments of households by approximately 150 billion yuan per year. This will help promote expanded consumption and investment, reduce early repayment behaviors, and also help to limit the space for illegal displacement of existing home loans, protecting the legitimate rights and interests of financial consumers and maintaining the stable and healthy development of the real estate market.'

Both the first and second home loan rates for existing homes are expected to be adjusted accordingly. On one hand, this lowers the cost of residents purchasing houses, promoting consumer spending and providing important support for the stable operation of the economy. On the other hand, it also helps restore market expectations, alleviate the wait-and-see sentiment due to anticipated decreases in mortgage rates, and along with this interest rate cut, all help further reduce the costs of homebuyers, boosting the demand for home purchases.

3. Lower the threshold for the purchase of second homes and guide the release of demand for improved housing.

The central bank once again adjusted the down payment ratio for second homes to further support the release of residents' demand for improving housing. Pan Gongsheng pointed out that "to better support the rigid and diversified demand for improving housing for urban and rural residents, the commercial individual housing loans at the national level will no longer distinguish between first homes and second homes, with a unified minimum down payment ratio of 15%. ... Each place can implement policies according to local conditions, autonomously decide whether to adopt differentiated arrangements, and determine the minimum lower limit of the down payment ratio within its jurisdiction."

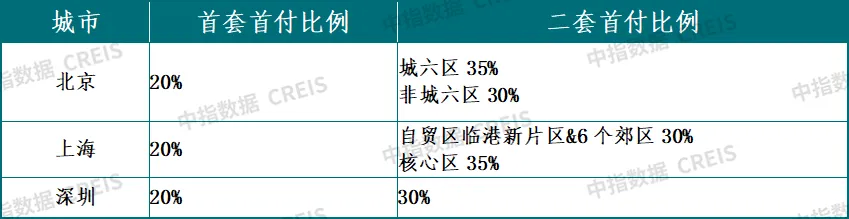

On May 17, the central bank and the China Banking and Insurance Regulatory Commission jointly issued a document, reducing the minimum down payment ratios for first and second home commercial loans to 15% and 25% respectively. Subsequently, various regions quickly followed suit. As of now, only Beijing, Shanghai, and Shenzhen have not yet lowered the down payment ratios for first and second home commercial loans to the national minimum.

Table: Current down payment ratios for commercial loans in Beijing, Shanghai, and Shenzhen

For most second and third-tier cities, the down payment ratio for second homes has already been reduced to a relatively low level. Lowering the down payment ratio again may have limited stimulative effects. However, for core cities with higher housing prices such as Beijing, Shanghai, and Shenzhen, most buyers of second homes usually complete the replacement by selling one to buy another, needing funds from completing transactions of existing properties. The higher down payment ratio for second homes previously imposed certain restrictions on purchasing new homes. The reduction of the down payment ratio for second homes will help alleviate the problem of having to buy before selling when switching homes, accelerating the circulation of the chain of first and second-hand housing replacements.

After the implementation of this policy, it is expected that various regions will speed up the implementation and lower the minimum down payment ratio for second homes to 15%. Beijing, Shanghai, and Shenzhen are also expected to follow suit and adjust their down payment ratios, further lowering the barrier to home purchases and potentially stimulating the release of demand for housing improvements into the market.

4. Provide more financial support for local state-owned enterprises to reduce inventory, but the key factors affecting the pace of inventory reduction have not changed in the short term.

On May 17, the People's Bank of China announced the establishment of a 300 billion yuan affordable housing refinancing scheme, guiding financial institutions to support local state-owned enterprises in acquiring completed but unsold commodity houses at reasonable prices for distribution or rental affordable housing in accordance with market-oriented and rule of law principles. However, the overall progress is still relatively slow. According to data disclosed by the central bank, as of the end of June 2024, the balance of the 300 billion yuan affordable housing refinancing was 12.1 billion yuan.

At this meeting, Pan Gongsheng pointed out that in order to further enhance the market-oriented incentives for banks and acquirers, we will increase the proportion of the People's Bank of China's contribution in the affordable housing refinancing policy from the original 60% to 100%. Originally, commercial banks provided 10 billion yuan, with the People's Bank of China providing 6 billion yuan. Now, commercial banks provide 10 billion yuan, while the People's Bank of China provides low-cost funds of 10 billion yuan, accelerating the destocking process of commodity houses. Increasing the central bank's contribution ratio in the refinancing policy is conducive to expanding commercial bank lending scale, and in conjunction with the central bank's interest rate reduction policy, is expected to accelerate the process of local inventory acquisition.

However, it is worth noting that state-owned enterprises in various regions still face significant difficulties in price matching and supply-demand mismatch, and these restrictive factors are still present in the short term. To accelerate the pace of state-owned enterprise acquisitions, further policy optimization may be necessary, such as expanding the scope of uses for acquired existing assets and expanding the types of acquisition targets.

5. Incremental policies to activate existing land assets are underway, with the injection of more funds expected to accelerate the pace of revitalizing local land resources and alleviate the funding pressure on real estate enterprises.

The central bank also proposed to 'support the acquisition of real estate companies' existing land. By using part of the local government special bonds for land reserves, studying policies that allow policy banks and commercial banks to provide loans to support conditionally market-oriented acquisition of real estate companies' land, revitalizing existing land resources, and alleviating funding pressures on real estate companies. If necessary, the People's Bank of China can also provide refinancing support. We, together with the Financial Regulatory Bureau, are still studying this policy. The policy is intended to support the acquisition of land by real estate companies using conditional market-oriented methods. The provision of refinancing support when necessary means that more accompanying funds will enter the market. For high-quality real estate enterprises, they can actively seek loan support, acquire high-quality land from financially distressed real estate companies, expand land reserves, and revitalize existing land. On the other hand, the sale of existing land by financially distressed real estate companies is also beneficial for alleviating funding pressures and further stabilizing market expectations.

In order to activate existing land resources, the Ministry of Natural Resources has already issued documents clearly specifying that for reclaimed land used for affordable housing purchases, support can be provided through local government special bonds and other funds. The People's Bank of China has further clarified and studied the fund support policy for conditionally market-oriented acquisition of real estate companies' land, and if necessary, will provide refinancing support. This means that more accompanying funds will enter the market. For high-quality real estate enterprises, they can actively seek loan support to acquire high-quality land from financially distressed real estate companies, expand land reserves, and activate existing land. On the other hand, the sale of existing land by financially distressed real estate companies is also beneficial for alleviating funding pressures and further stabilizing market expectations.

6. Operational property loans and the '16 Financial Measures' extended to the end of 2026 will ease the funding pressure on real estate enterprises.

Operating property loans delayed will enhance the debt repayment ability of some real estate developers. In January, the People's Bank of China and the China Banking and Insurance Regulatory Commission jointly issued the "Notice on the Management of Operating Property Loans", which allows operating property loans issued to real estate development enterprises with standardized operations and good development prospects to be used to repay the existing loans of real estate developers and the public market bonds they issued before the end of this year.

At this press conference, the policy has been extended until the end of 2026. For real estate developers with a large number of commercial real estate projects and stable operations, such as$CHINA RES LAND (01109.HK)$,$LONGFOR GROUP (00960.HK)$,$China Merchants Shekou Industrial Zone Holdings (001979.SZ)$,$CHINA JINMAO (00817.HK)$,$SEAZEN (01030.HK)$Wait, there is a great bullish signal. These real estate developers can use operating property loans for debt repayment, further enhancing corporate debt repayment capabilities.

In April, the Shanghai branch of the central bank convened 8 major commercial banks in Shanghai, as well as Longfor Group, Zhangjiang Group, Nanfeng Group, Dahua Group and 12 real estate developers to participate in a centralized signing ceremony for operating property loans, with a signing loan amount of 14.6 billion yuan.

The further extension of the "16 financial regulations" will ease the debt repayment pressure on real estate enterprises. In July 2023, the People's Bank of China and the China Banking and Insurance Regulatory Commission issued a notice clarifying that the application period for the real estate "16 financial regulations" released by the People's Bank of China and the former China Banking and Insurance Regulatory Commission in November 2022 will be uniformly extended to December 31, 2024. This announcement indicated that the application period of the real estate "16 financial regulations" has been extended to the end of 2026, demonstrating that financial institutions will be able to further extend existing financing such as development loans and trust loans for real estate enterprises. From January to August 2024, the total sales of the top 100 real estate companies decreased by 38.5% year-on-year, the actual funds of real estate development enterprises decreased by 20.2% year-on-year, and the total amount of real estate industry bond financing decreased by 29.7% year-on-year. Despite the significant decline in real estate sales and financing for real estate companies, the ability to extend existing development and trust loans will effectively alleviate the debt repayment pressure on real estate enterprises.

7. The continuous advancement of the "white list" project is yielding results.

Li Yunze pointed out, "Up to now, commercial banks have approved over 5700 "white list" projects, with approved financing amounting to 1.43 trillion yuan, supporting the timely delivery of over 4 million housing units. Driven by the coordination mechanism, the support of financial institutions for the real estate industry is continuously expanding. As of the end of August, our real estate development loans this year have achieved positive growth compared to the beginning of the year, reversing the downward trend of real estate development loans. Merger and acquisition loans in the real estate and housing leasing loans have also grown by 14% and 18%, providing strong financial support for promoting the stable and healthy development of the real estate market.

The "white list" mechanism for future project financing will continue to be promoted, playing an important role in "guaranteeing delivery" and alleviating corporate financial pressure, further easing residents' concerns about the delivery of pre-sold houses and helping restore homebuyers' confidence.

Editor/Rocky