Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, e.l.f. Beauty, Inc. (NYSE:ELF) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does e.l.f. Beauty Carry?

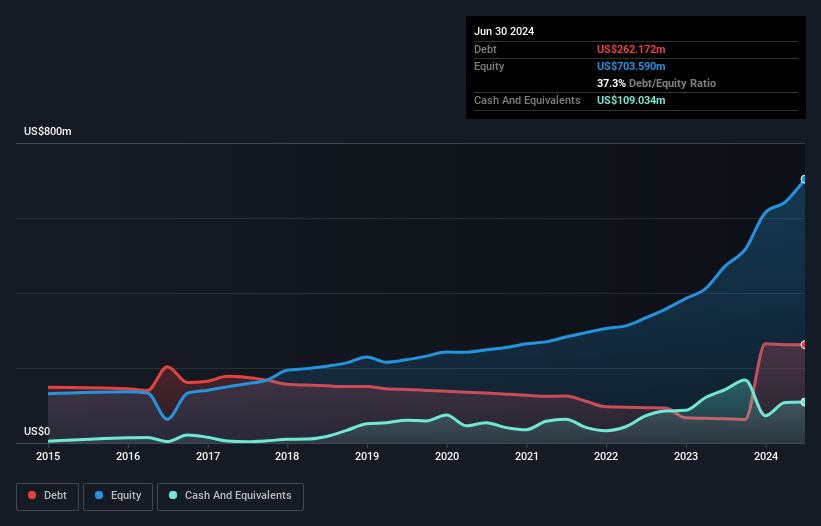

You can click the graphic below for the historical numbers, but it shows that as of June 2024 e.l.f. Beauty had US$262.2m of debt, an increase on US$64.6m, over one year. However, because it has a cash reserve of US$109.0m, its net debt is less, at about US$153.1m.

How Healthy Is e.l.f. Beauty's Balance Sheet?

According to the last reported balance sheet, e.l.f. Beauty had liabilities of US$299.8m due within 12 months, and liabilities of US$201.4m due beyond 12 months. Offsetting these obligations, it had cash of US$109.0m as well as receivables valued at US$155.7m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$236.5m.

According to the last reported balance sheet, e.l.f. Beauty had liabilities of US$299.8m due within 12 months, and liabilities of US$201.4m due beyond 12 months. Offsetting these obligations, it had cash of US$109.0m as well as receivables valued at US$155.7m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$236.5m.

Since publicly traded e.l.f. Beauty shares are worth a total of US$6.37b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

e.l.f. Beauty has a low net debt to EBITDA ratio of only 0.88. And its EBIT covers its interest expense a whopping 13.0 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. On top of that, e.l.f. Beauty grew its EBIT by 33% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine e.l.f. Beauty's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, e.l.f. Beauty recorded free cash flow worth 59% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

The good news is that e.l.f. Beauty's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its EBIT growth rate also supports that impression! Considering this range of factors, it seems to us that e.l.f. Beauty is quite prudent with its debt, and the risks seem well managed. So we're not worried about the use of a little leverage on the balance sheet. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. We've identified 1 warning sign with e.l.f. Beauty , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.