Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Sempra (NYSE:SRE). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

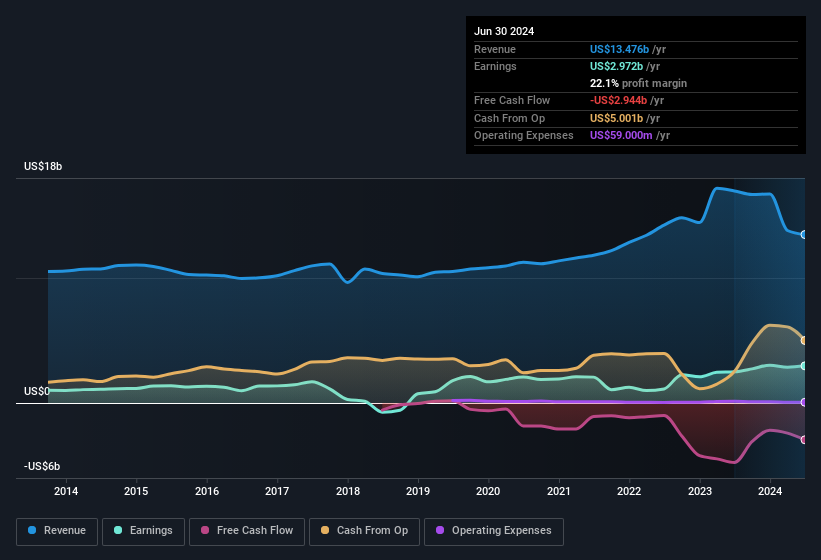

How Fast Is Sempra Growing?

The market is a voting machine in the short term, but a weighing machine in the long term, so you'd expect share price to follow earnings per share (EPS) outcomes eventually. That means EPS growth is considered a real positive by most successful long-term investors. Over the last three years, Sempra has grown EPS by 10% per year. That's a good rate of growth, if it can be sustained.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Despite consistency in EBIT margins year on year, Sempra has actually recorded a dip in revenue. While this may raise concerns, investors should investigate the reasoning behind this.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Despite consistency in EBIT margins year on year, Sempra has actually recorded a dip in revenue. While this may raise concerns, investors should investigate the reasoning behind this.

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

While we live in the present moment, there's little doubt that the future matters most in the investment decision process. So why not check this interactive chart depicting future EPS estimates, for Sempra?

Are Sempra Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

Sempra top brass are certainly in sync, not having sold any shares, over the last year. But the real excitement comes from the US$150k that Independent Director Richard Mark spent buying shares (at an average price of about US$77.97). Strong buying like that could be a sign of opportunity.

On top of the insider buying, it's good to see that Sempra insiders have a valuable investment in the business. As a matter of fact, their holding is valued at US$20m. That's a lot of money, and no small incentive to work hard. Despite being just 0.04% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

Does Sempra Deserve A Spot On Your Watchlist?

As previously touched on, Sempra is a growing business, which is encouraging. In addition, insiders have been busy adding to their sizeable holdings in the company. These factors alone make the company an interesting prospect for your watchlist, as well as continuing research. You still need to take note of risks, for example - Sempra has 2 warning signs (and 1 which is a bit unpleasant) we think you should know about.

Keen growth investors love to see insider activity. Thankfully, Sempra isn't the only one. You can see a a curated list of companies which have exhibited consistent growth accompanied by high insider ownership.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.