上周,美联储的一系列高调举动让多头振奋,美国股市创下历史新高,

上周,美联储的一系列高调举动让多头振奋,美国股市创下历史新高,US stocks and bonds are valued higher than the levels at the start of the past 14 easing cycles by the Federal Reserve, making them more susceptible to negative news.

For Wall Street traders with seemingly increasing speculative preferences, last week's 50 basis point rate cut by the Fed was a moment of vindication for them.

Now, with the Fed's new round of easing supporting the economic outlook, another variable - valuation - is becoming a bigger challenge in determining how far this optimism can go.

Last week, a series of high-profile moves by the Fed invigorated the bulls, and the US stock market hit a historic high,$NASDAQ 100 Index (.NDX.US)$recording the largest two-week gain since November last year.

Last week, a series of high-profile moves by the Fed invigorated the bulls, and the US stock market hit a historic high,$NASDAQ 100 Index (.NDX.US)$recording the largest two-week gain since November last year.

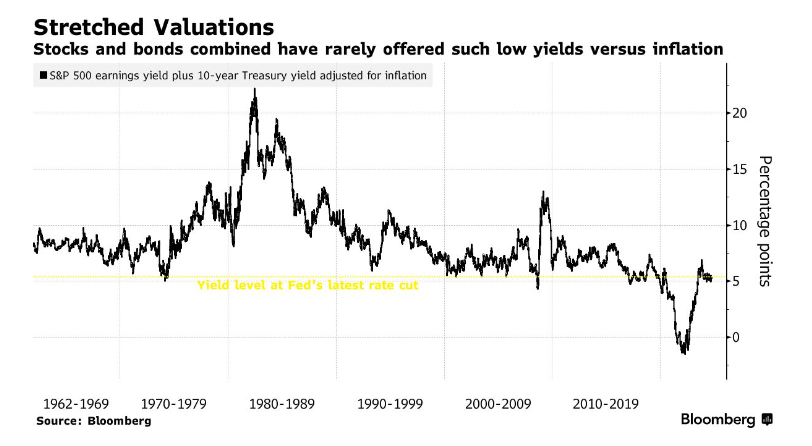

Although valuation itself has long been an obstacle to market rally, in the current situation, there is not much room for error if something were to disrupt investors' big bets. A risk based on inflation adjustment.$S&P 500 Index (.SPX.US)$The model of roi and the 10-year US Treasury yield shows that the current cross-asset prices are higher than the levels at the start of all 14 previous Fed easing cycles, which are typically associated with economic recessions.

According to Lauren Goodwin, economist and chief market strategist at New York Life Investments, high valuation is just one of the factors that make the market environment particularly complex. This environment has various potential outcomes, including continued stock market gains. She says that while high valuation is not a good tool for timing the market, it does increase the market's vulnerability if other aspects falter.

She said, "If any of the seven giants' financial reports show disappointing situations at a substantial level, it will pose a risk to valuation. Bad inflation data—such as rising inflation—is also dangerous because it will pose a risk to this rate-cutting cycle. Of course, anything related to economic growth will threaten valuations."

The total return of the S&P 500 index in 2024 has already exceeded 20%, indicating that many of the benefits from economic and policy bullish factors have already been absorbed by risky assets. Looking at the performance of major ETFs, the U.S. stock market and government bonds have been rising for the fifth consecutive month. This is the longest simultaneous increase since 2006.

The strong rise in the U.S. stock market this year has led to many valuation indicators being significantly overvalued. This includes the so-called Buffett Indicator, which divides the total market value of U.S. stocks by the total value of the U.S. gross domestic product (GDP) in U.S. dollars. Yardeni pointed out that as Buffett recently reduced holdings of some high-profile stocks, this indicator is approaching a historical high.

The founder of Yardeni Research said, "Corporate profits are likely to continue to demonstrate that rational prosperity is reasonable. The issue lies with valuation. In a frothy scenario, the S&P 500 index may soar to over 6000 by the end of this year. Although this will be very bullish in the short term, it will increase the possibility of a pullback early next year."

One reason why high valuations have not hindered the rebound of U.S. stocks is that although current valuations always seem expensive at any time, in the case of synchronous profit growth, high valuations are more likely to be proven rational. Garrett Melson, Portfolio Strategist at Natixis Investment Managers Solutions, said this concept often appears mainly as a reason to review market trends.

He explained, "Currently, valuations really serve no purpose because ultimately, they just offer a perspective. That's how the market operates."

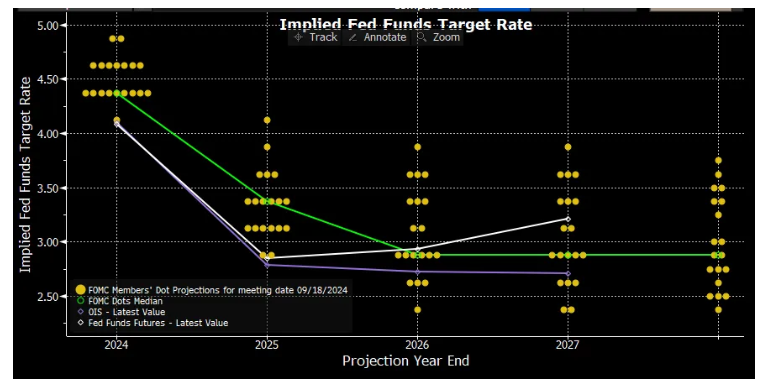

However, there is a high possibility of disappointment in the U.S. bond market as bond traders continue to digest expectations for a more aggressive rate cut by the Federal Reserve next year compared to policymakers' expectations. They expect rates to drop to around 2.8% by 2025. In contrast, based on policymakers' median forecast, the expected rate level by then is 3.4%.

Just a few days after the Federal Reserve launched the highly anticipated easing cycle, the yield on 10-year US Treasury bonds rose to a two-week high.

One issue that interest rate speculators face is that while the labor market is showing intermittent weakness, most data remains robust. Jim Reid, a strategist at Deutsche Bank, used an artificial intelligence model to classify and rank 16 US economic and market variables (from consumer prices to retail sales) and found that currently only two variables indicate an urgent need for economic stimulus measures.

When the Federal Reserve launched easing cycles with similar interest rate cuts in 2001 and 2007, the number of flashing "interest rate urgency" indicators was 6 and 5, respectively.

Reid wrote, "Analysis shows that compared to 2024, it would be easier to prove that the 50 basis point interest rate cut in 2001 and 2007 was reasonable. Although this does not necessarily mean that last week's interest rate decision was wrong, it does mean that the Federal Reserve is more proactive this time and indicates that their decision-making has a greater degree of subjectivity."

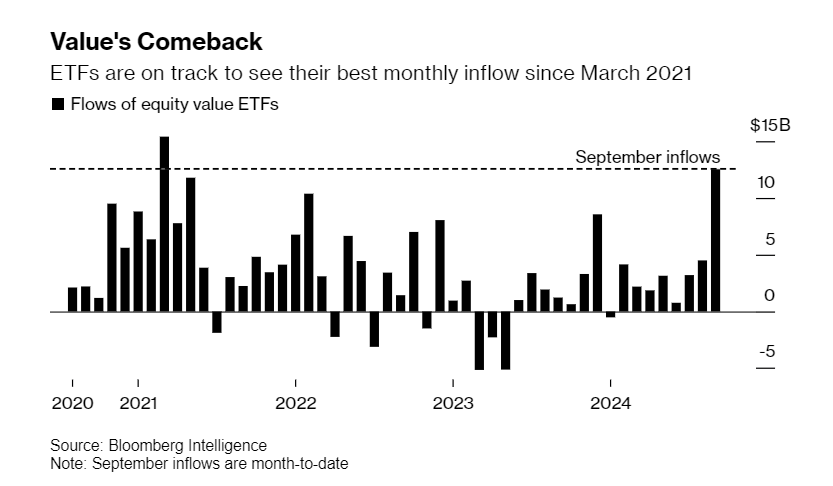

At least for now, the market trend and capital flow have shown a clear belief in a positive economic outlook. Small-cap stocks, which are most sensitive to economic fluctuations, rose for seven consecutive trading days until last Thursday, marking the longest continuous increase since March 2021. Value-focused ETFs attracted $13 billion in funds this month, the largest inflow in over three years. These value-oriented funds are mainly focused on cyclical stocks like banks.

In terms of fixed income, people's concerns about inflation, which has caused bonds to be hit hard in recent years, have largely subsided. Earlier this month, the so-called 10-year break-even rate (an indicator of consumer price index growth expectations) fell to 2.03%, the lowest level since 2021.

However, anyone hoping for the S&P 500 index to continue its gains since the beginning of the year should consider that Wall Street strategists, who are not known for their caution, have already seen the exhaustion of the upside potential. The latest Bloomberg survey shows their consensus forecast of 5483 points, which means that the S&P 500 index is expected to drop by 4% for the remainder of this year.

Emily Roland, Co-Chief Investment Strategist at John Hancock Investment Management, has felt this fear among clients.

She said, "When I go out and talk to investors every week, they tell me that they are afraid. I haven't seen a lot of bullish sentiment, but of course, this is not reflected in the cross-asset behavior we see in the stock market approaching historical highs."

Editor/Rocky