通胀较上年同期放缓反映出能源和食品价格下跌,以及核心成本的放缓。经济学家预计,不包括食品和燃料的PCE物价指数可能连续第三个月环比上涨0.2%。

通胀较上年同期放缓反映出能源和食品价格下跌,以及核心成本的放缓。经济学家预计,不包括食品和燃料的PCE物价指数可能连续第三个月环比上涨0.2%。This week, the global financial markets will see a number of important data and heavyweight events.

The most favored price indicators by the Federal Reserve slowing down and strong consumer demand will support the Fed's decision to significantly cut interest rates and Chairman Powell's view that the economy is still strong.

Economists predict that the US August PCE price index, which is scheduled to be released on Friday, will increase by only 0.1% for the second consecutive month. This inflation indicator may rise 2.3% compared to the same period last year, the smallest annual increase since early 2021, slightly higher than the Fed's 2% target.

The slowdown in inflation compared to the same period last year reflects the decline in energy and food prices, as well as the moderation of core costs. Economists predict that the PCE price index, excluding food and fuel, may rise by 0.2% for the third consecutive month.

The slowdown in inflation compared to the same period last year reflects the decline in energy and food prices, as well as the moderation of core costs. Economists predict that the PCE price index, excluding food and fuel, may rise by 0.2% for the third consecutive month.

The decline in inflationary pressures earlier this year provided enough confidence for Federal Reserve policymakers to lower interest rates by 50 basis points on September 18. This is the first rate cut in over four years and represents a shift in Fed policy to avoid deterioration in the labor market.

Investors will be paying attention to speeches by several Federal Reserve officials in the coming week. On Thursday, Federal Reserve Chairman Powell recorded a video as the opening remarks for an event. In addition, Fed Vice Chair Michelle Bowman, Adriana Kugler, Lisa Cook, as well as regional Fed presidents Raphael Bostic and Austan Goolsbee, will be attending various events.

Inflation data for August will be released along with personal income and spending data, and economists predict that US household spending will once again see significant growth. Continued growth in consumer spending helps to improve the likelihood of continued economic expansion.

Other important US economic data to watch for include August new home sales, second quarter gross domestic product (GDP), weekly initial jobless claims, and August durable goods orders.

The GDP data for July and the preliminary data for August in Canada are expected to show weak growth in the third quarter, possibly below the Bank of Canada's annualized growth expectation of 2.8%. Meanwhile, Bank of Canada Governor Tiff Macklem will deliver a speech at a banking conference in Toronto.

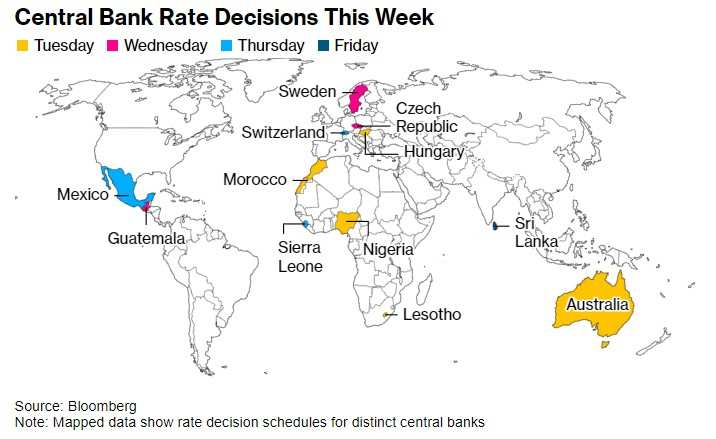

In addition, the Organization for Economic Cooperation and Development (OECD) will release new economic forecasts on Wednesday, and the Swiss and Swedish central banks may lower interest rates, while the Reserve Bank of Australia is expected to keep rates unchanged.

Several central banks will announce their interest rate decisions this week.

Here are the major events that the financial markets will be anticipating this week:

Asia

The market expects the Reserve Bank of Australia to keep the cash rate unchanged at 4.35% on Tuesday, with a focus on whether RBA Governor Michele Bullock will maintain her hawkish stance. Strong employment data earlier prompted traders to reduce bets on a rate cut in December.

Bloomberg Economics still believes that the Reserve Bank of Australia may ease monetary policy in the fourth quarter. Australian authorities will have to wait until Wednesday to see if inflation in August has cooled for a third consecutive month.

Australian Treasurer Jim Chalmers said on Sunday that he expects the upcoming data to show encouraging progress in Australia's fight against inflation, but he admits that the Reserve Bank of Australia may not be ready to cut rates this week.

Other countries that have announced the latest inflation data include Malaysia and Singapore, and it is expected that the inflation rate in both countries will slow down in August.

Japan will announce new inflation data on Friday, and the market expects Tokyo CPI in September to exceed the Bank of Japan's target of 2%.

Australia and India will release the Purchasing Managers' Index (PMI) for September on Monday, and Japan will announce it the next day.

Europe, Middle East, Africa.

Four central banks in Europe will announce interest rate decisions, and investors may question whether policymakers are interested in following the footsteps of the Federal Reserve in cutting interest rates by 50 basis points.

The Swiss National Bank will announce its interest rate decision on Thursday. Although most economists expect the bank to cut rates by 25 basis points, observers believe that with the continuous strength of the Swiss franc, the possibility of the Swiss National Bank cutting rates by 50 basis points has increased due to the significant rate cut by the United States. This is the last meeting of Thomas Jordan, the head of the Swiss National Bank, and his term will end at the end of this month.

The Swedish central bank will announce its interest rate decision on Wednesday. The market expects the bank to cut interest rates by 25 basis points for the third time this year, lowering the rate to 3.25%, and outline the further path of interest rate cuts.

The current guidance is to raise interest rates two to three more times in 2024, including on Wednesday. Swedish central bank policy makers discussed a 50-basis-point rate cut at last month's meeting, but most economists believe the bank is more likely to wait until November to take larger rate-cutting measures.

At the same time, in Eastern Europe, it is expected that the Hungarian central bank will cut interest rates by 25 basis points on Tuesday, and the Czech central bank by Thursday.

The eurozone and the United Kingdom will release the preliminary September PMI figures on Monday, reflecting the state of private sector activity at the end of the third quarter.

Due to the focus on the weak German economy by investors, the Ifo Business Confidence Index to be released on Tuesday will be a focal point. On the same day, the President of the German Central Bank, Joachim Nagel, will speak on the economy. German economic institutions will release new forecasts on Thursday.

Investors will closely monitor the data from France as well as the newly appointed Finance Minister of the country, Antoine Armand. The PMI index of the eurozone's second-largest economy received a boost from the Olympics in August, but this effect is expected to fade this month. Consumer confidence index will also be published.

Investors are also watching for the inflation data for France and Spain in September, to hint at the overall inflation results for the eurozone to be published next week. Economists predict that the inflation rates of both countries will fall below 2%.

Apart from Nagel, there are 6 other eurozone policymakers planning to speak, including the President of the European Central Bank, Christine Lagarde, Chief Economist Philip Lane, and the new Governor of the Bank of Spain, Jose Luis Escriva.

In Africa, the Nigerian central bank may pause its tightening policy on Tuesday, the Moroccan central bank may keep interest rates at 2.75%, and Lesotho in southern Africa may maintain borrowing costs at 7.75% due to persistent high inflation.

Latin America

The minutes of the Brazilian Central Bank's September interest rate meeting and the quarterly inflation report will be the focus.

After raising interest rates by 25 basis points to 10.75% on September 18, the minutes of the Brazilian Central Bank's meeting may provide a more detailed policy roadmap. The market expects the Brazilian Central Bank to raise its forecasts for inflation, key interest rates, and GDP growth.

The employment data to be released this week may show that the Brazilian labor market is still at historically tight levels, while the mid-month inflation rate may have stalled near the top of the Brazilian Central Bank's target range.

Argentina is expected to release proxy GDP data for July, which could support the following views: Argentina's economy has passed the lowest point of 2024 and is beginning to recover in the second half of the year.

In Mexico, a slowdown in domestic demand could lead to another weak retail sales data, and mid-month inflation data is unlikely to provide sufficient reasons for policymakers to cut interest rates or keep them unchanged at the upcoming meeting of the Bank of Mexico.

The market expects Mexico to cut interest rates by 25 basis points to 10.5%, but some analysts believe there could be a 50 basis point cut to stay in line with the Federal Reserve.

Editor/Lambor