一个根据通胀调整标普500指数收益率和10年期美债收益率的模型显示,

一个根据通胀调整标普500指数收益率和10年期美债收益率的模型显示,Source: Wall Street See

Taking the 2008 financial crisis as a lesson, if the USA has already or is about to start declining, even a significant interest rate cut cannot prevent the arrival of a bear market. According to goldman sachs's latest research reports, if the economy has already entered a recession before the first interest rate cut, then the s&p 500 index is expected to drop an average of 14% in the next year.

The Federal Reserve's first interest rate cut has sparked expectations of avoiding an economic downturn in the United States, causing the already high valuation of the U.S. stock and bond markets to rise further.

A model based on adjusting the S&P 500 index return rate and the 10-year U.S. Treasury bond yield to inflation shows that the current valuation level of U.S. stocks and bonds is higher than the level at the start of the previous 14 easing cycles (usually associated with recessions) by the Federal Reserve.

A model based on adjusting the S&P 500 index return rate and the 10-year U.S. Treasury bond yield to inflation shows that the current valuation level of U.S. stocks and bonds is higher than the level at the start of the previous 14 easing cycles (usually associated with recessions) by the Federal Reserve.

With the U.S. stock market reaching new historic highs, the total return rate of the S&P 500 index has exceeded 20% year-to-date, indicating that many of this week's economic and policy news have already been priced into risk assets.

Looking at the performance of major ETFs, U.S. stocks and bonds are expected to achieve five consecutive months of growth, the longest synchronized growth cycle since 2006. In addition, investors are pouring money into riskier corporate bonds, betting that lower borrowing costs will allow heavily indebted companies to refinance and extend their maturity dates, thereby reducing default rates and supporting market valuations.

However, a significant interest rate cut may not be able to prevent investors from entering a bear market. Spencer Jakab, a well-known journalist for The Wall Street Journal, wrote in a report on Saturday that if the economy has already begun to decline, then "Federal Reserve Chairman Powell really cannot prevent their investment portfolios from shrinking as people imagine."

The initial reaction of the stock market to the interest rate cut on Wednesday was enthusiastic. However, this has often proven to be an illusion - we still do not know the ending of this drama.

Jakab cited a Goldman Sachs report that if the economy is already in a recession before the first rate cut, the s&p 500 index will average a 14% decline in the next year.

The financial crisis of 2008 is still vivid.

Taking the interest rate cycle in 2007 as an example, after the first rate cut by the Federal Reserve, the US stock market skyrocketed, with the Dow Jones Index recording its largest increase in over four years, rising by 336 points, equivalent to about 1000 points today. Lehman Brothers had the best stock performance, soaring 10%. It is a coincidence that the first rate cut in 2007 and this rate cut both occurred on September 18th, with the same initial federal funds rate and the same rate cut of 50 basis points.

But as we now know, after the US stock market reached its peak of the bull market just three weeks later, a panic-induced crash began in January 2008, and less than a year later, Lehman Brothers went bankrupt, becoming the largest bankruptcy case in US history. By that time, the Federal Reserve had already cut rates six times, lowering the interest rate to 2%, the lowest level in nearly four years. In the two months following the outbreak of the Lehman crisis, the Federal Reserve cut rates significantly three times, with the interest rate initially approaching zero (technically 0% to 0.25%).

Two months after the start of the rate cut cycle, market sentiment had already become gloomy. However, a survey of 54 economists conducted by The Wall Street Journal at the time showed that there was only a one-third chance of the US economy entering a recession within the next 12 months.

Jakab wrote that the Federal Reserve has no magic wand to save an economy and stock market that are already in or about to enter a difficult situation.

Interest rate cuts are certainly important for bond investors. However, they may only temporarily weaken the already emerging market downturn and take a long time to permeate to companies and consumers.

In contrast, "the trajectory of economic growth is more capable of driving stock market gains than the speed of rate cuts", as Goldman Sachs strategist David Kostin recently pointed out. If the economy is already in a recession before the first rate cut, the s&p 500 index will average a 14% decline in the next year. If the economy is not in a recession, the situation is just the opposite.

However, Jakab believes that there is currently no concrete evidence to suggest that the US economy will soon enter a recession, and it is uncommon for the stock market to experience significant declines in the absence of an obvious economic downturn.

This helps explain why the stock market can maintain its level close to historical highs, and why the usual cautious sentiment in the market is not apparent. In addition, there is a misconception that the Fed's rate cuts are a reason to stay calm and continue investing, which supports market sentiment to some extent.

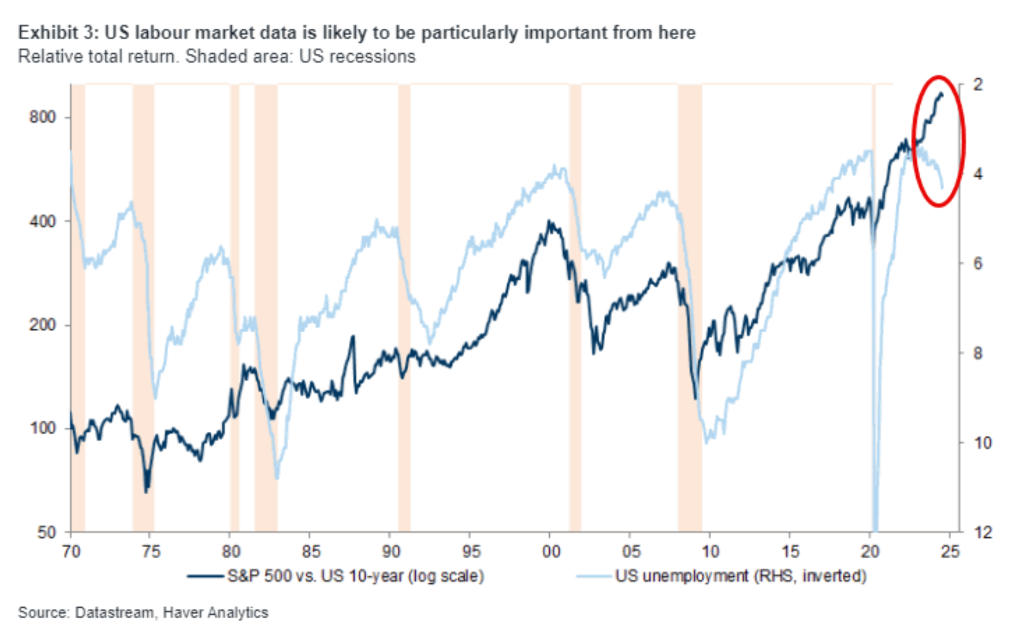

Pay attention to whether the labor market continues to deteriorate.

Jakab is not the only one concerned that the Fed's significant rate cuts may be too late. BlackRock researchers Amanda Lynam and Dominique Bly wrote in a recent report that participants in the market are also concerned about signs of deteriorating fundamentals, particularly for floating rate bonds, as US monetary policy may continue to tighten.

In addition, the two researchers pointed out that although CCC-rated corporate bonds have performed well, they still face overall pressure. These companies have lower overall income levels compared to interest expenses. The borrowing costs of CCC bonds still remain around 10%, which forces some smaller companies to refinance after the era of loose monetary policy, putting them in a predicament and exposing them to default risk even if interest rates decline.

JPMorgan analysts Eric Beinstein and Nathaniel Rosenbaum wrote in a research report last week that any signs of weakness in the labor market would have an adverse impact on spreads, as it would intensify concerns of an economic recession and lower yields.

JPMorgan analysts Eric Beinstein and Nathaniel Rosenbaum wrote in a research report last week that any signs of weakness in the labor market would have an adverse impact on spreads, as it would intensify concerns of an economic recession and lower yields.

Editor / jayden