D-Market Elektronik Hizmetler ve Ticaret A.S. (NASDAQ:HEPS) shares have retraced a considerable 25% in the last month, reversing a fair amount of their solid recent performance. Looking at the bigger picture, even after this poor month the stock is up 79% in the last year.

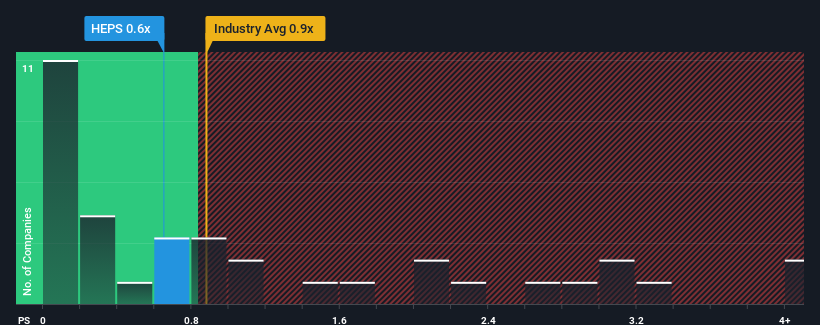

In spite of the heavy fall in price, there still wouldn't be many who think D-Market Elektronik Hizmetler ve Ticaret's price-to-sales (or "P/S") ratio of 0.6x is worth a mention when the median P/S in the United States' Multiline Retail industry is similar at about 0.9x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

What Does D-Market Elektronik Hizmetler ve Ticaret's P/S Mean For Shareholders?

D-Market Elektronik Hizmetler ve Ticaret could be doing better as it's been growing revenue less than most other companies lately. It might be that many expect the uninspiring revenue performance to strengthen positively, which has kept the P/S ratio from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Want the full picture on analyst estimates for the company? Then our free report on D-Market Elektronik Hizmetler ve Ticaret will help you uncover what's on the horizon.How Is D-Market Elektronik Hizmetler ve Ticaret's Revenue Growth Trending?

D-Market Elektronik Hizmetler ve Ticaret's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

D-Market Elektronik Hizmetler ve Ticaret's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Taking a look back first, we see that there was hardly any revenue growth to speak of for the company over the past year. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, even though the last 12 months were nothing to write home about. So while the company has done a great job in the past, it's somewhat concerning to see revenue growth decline so harshly.

Looking ahead now, revenue is anticipated to climb by 41% during the coming year according to the three analysts following the company. With the industry only predicted to deliver 13%, the company is positioned for a stronger revenue result.

With this in consideration, we find it intriguing that D-Market Elektronik Hizmetler ve Ticaret's P/S is closely matching its industry peers. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Final Word

Following D-Market Elektronik Hizmetler ve Ticaret's share price tumble, its P/S is just clinging on to the industry median P/S. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that D-Market Elektronik Hizmetler ve Ticaret currently trades on a lower than expected P/S since its forecasted revenue growth is higher than the wider industry. When we see a strong revenue outlook, with growth outpacing the industry, we can only assume potential uncertainty around these figures are what might be placing slight pressure on the P/S ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future revenue could see some volatility.

Plus, you should also learn about these 2 warning signs we've spotted with D-Market Elektronik Hizmetler ve Ticaret.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.