After a significant interest rate cut, the Federal Reserve quickly began managing new expectations!

The U.S. stock market closed basically flat on Friday, with major stock indexes performing weakly. Michelle Bowman, a board member of the Federal Reserve, insists that a smaller interest rate cut this week would be preferable. Bowman is the only member of the Federal Reserve who disagreed with the latest interest rate policy decision, stating that she prefers a smaller rate cut (25 basis points) rather than 50 basis points.

In fact, according to the latest data from the Federal Reserve's balance sheet, although there has been a significant interest rate cut this week, the Federal Reserve has not changed its trend of shrinking the balance sheet. In other words, quantitative easing and interest rate cuts have not occurred simultaneously, which may also mean that the Federal Reserve still has concerns about inflation.

It is worth noting that shortly after the Federal Reserve cut interest rates by 50 basis points, pushing the U.S. stock market to new historic highs, European Central Bank President Lagarde warned on Friday local time that the global economy is facing pressures of "economic nationalism," a collapse of global trade, and the Great Depression of the 1920s.

It is worth noting that shortly after the Federal Reserve cut interest rates by 50 basis points, pushing the U.S. stock market to new historic highs, European Central Bank President Lagarde warned on Friday local time that the global economy is facing pressures of "economic nationalism," a collapse of global trade, and the Great Depression of the 1920s.

Different voices

Michelle Bowman, the only opponent of the Federal Reserve's significant interest rate cut and a board member of the Federal Reserve, stated on Friday local time that during this process, taking smaller rate cuts would be a better choice, as the inflation rate has not yet dropped to the central bank's target of 2%. The Federal Reserve's larger-scale policy actions may be interpreted as announcing victory too early in the task of price stability.

She stated that she prefers a smaller rate cut (25 basis points) rather than 50 basis points.

She agrees that it is necessary to lower interest rates this week, but she believes that taking measured steps towards a more neutral policy stance will ensure that the inflation rate continues to decline towards the target of 2%. This approach can also avoid unnecessary demand stimulation. Powell acknowledges Bowman's dissenting view, but he also states that the interest rate cut has received "broad support" and that he shares many commonalities with his fellow policy makers.

In a statement advocating a small reduction in production, Bauman stated that the US economy remains strong, with "robust potential growth" and the job market approaching full employment. Despite a perceived slowdown in hiring, layoffs remain low. Considering the trend of productivity growth, she believes that the normalization of the job market is necessary to help wage growth align with a 2% inflation rate.

Currently, the market has begun to anticipate another 50 basis point rate cut by the Fed in November. Fed Governor Waller stated on Friday that a 50 basis point rate cut by the Fed is the right move to maintain a strong economy. The inflation data released during the blackout period has led me to lean toward a significant rate cut. The magnitude of future rate cuts will depend on the upcoming data. If the job market deteriorates, there may be consideration of another 50 basis point rate cut. His comments reinforced market expectations of a 50 basis point rate cut.

However, there is almost a split among members of the Federal Open Market Committee regarding the expected number of additional rate cuts this year. Seven members support an additional 25 basis points rate cut by the end of the year, while nine members support an additional 50 basis points rate cut. According to the Chicago Mercantile Exchange's FedWatch tool, the market has fully anticipated that the Fed will cut rates by at least 25 basis points in November, with a 48.9% chance of a 50 basis point rate cut.

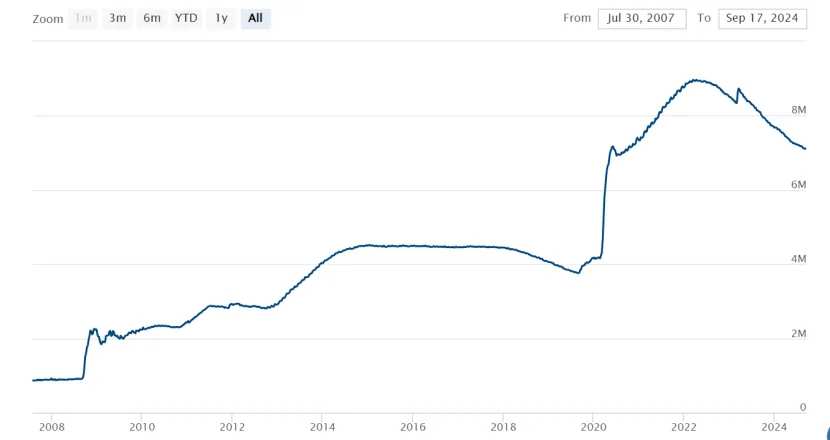

Trends in the balance sheet

For capital markets, in addition to interest rates, the balance sheet is worth paying attention to. Although the Fed has already cut rates significantly, there has not been a trend of quantitive easing in its balance sheet. Simultaneously lowering funding rates while using balance sheet reduction to control inflation that is not completely subdued may be the current strategy of the Fed.

However, only when the Fed implements quantitative easing can the loose liquidity situation of the global offshore US dollar truly materialize. Therefore, even though the Fed cuts rates significantly, the US dollar index has not fallen below 100, and it still shows signs of stability in the short term.

According to a research report released by Bank of America, it is expected that the Fed will end balance sheet reduction by the end of March 2025, while the previously predicted end time was December 2024, due to the limited discussion among decision-makers. The September FOMC meeting indicated that the Fed considers changes in policy rates and the balance sheet to be independent of each other. Nevertheless, strategists still believe that the Fed should approach quantitive tightening with caution during the approaching debt ceiling period, as it could lead to funding "blind spots" that policymakers may wish to avoid. They believe that the lack of attention to quantitive tightening suggests a postponement of the end of balance sheet reduction, with increased volatility in funding. During the approaching debt ceiling period, the decline in the Treasury General Account (TGA) offset the impact of quantitive tightening on liquidity, halting or temporarily reversing upward pressure on the funding market. However, the consumption and corresponding replenishment scale of the TGA will be about twice as large as in 2019. After the pause of the debt ceiling in 2019, the repurchase market experienced significant volatility in September of that year.

Barclays believes that although the Fed has indicated that it can reduce the balance sheet while lowering interest rates, it is advisable to end balance sheet reduction ahead of time due to risk management considerations. Barclays expects the Fed to end quantitative tightening in December and announce it at the November meeting.

Some warnings.

The actions of central banks around the world are driven by changes in the economic trend. And from the current situation, it doesn't seem too good.

Christine Lagarde, President of the European Central Bank, pointed out in a speech at the International Monetary Fund in Washington on Friday local time: "We are facing the most serious pandemic since the 1920s, the most severe conflict in Europe since the 1940s, and the most serious energy shock since the 1970s.

She believes that there are some similarities between the 1920s and the 2020s, especially in terms of "setbacks in global trade integration" and "technological progress." The global economy is facing the pressure of "economic nationalism," global trade collapse, and the Great Depression of the 1920s. These disruptions, along with supply chain issues and other factors, have permanently changed global economic activity.

According to Xinhua News Agency, renowned economist David Rosenberg recently expressed strong concerns about an imminent economic recession. He believes that the performance of the stock market is clearly disconnected from the economic fundamentals. Although stock indices continue to reach new historical highs, this increase is mainly driven by weak profit growth. He said that consumer spending exceeds expectations, but this spending is not driven by income growth, but rather by worrying decline in personal savings rates. At present, the personal savings rate in the United States has dropped to a historically low level of 2.9%, which is extremely rare.

In recent months, investment banks such as Goldman Sachs have been warning clients to prepare for a critical shift in the economy. They believe that some changes in the macroeconomic pattern indicate a significant increase in the probability of an economic recession, which could have global implications.

Editor/Emily